Both Nonresidential and Residential Spending Retreat from January Levels amid Extreme Winter Weather; Association Posts Inflation Alert to Aid Understanding of Squeeze on Nonresidential Construction Firms

Construction spending slumped in February as unseasonably severe weather hammered the industry and a decline in new projects squeezed nonresidential contractors experiencing rising costs and delivery times, according to an analysis of new federal construction spending data by the Associated General Contractors of America. The association posted a Construction Inflation Alert to inform project owners and government officials about the threat to project completion dates and contractors’ financial health.

“The downturn in February reflects both an unfavorable change from mild January weather and an ongoing decline in new nonresidential projects,” said Ken Simonson, the association’s chief economist. “Unfortunately, it will take more than mild weather to help nonresidential contractors overcome the multiple challenges of falling demand for many project types, steeply rising costs, and lengthening or uncertain delivery times for key materials.”

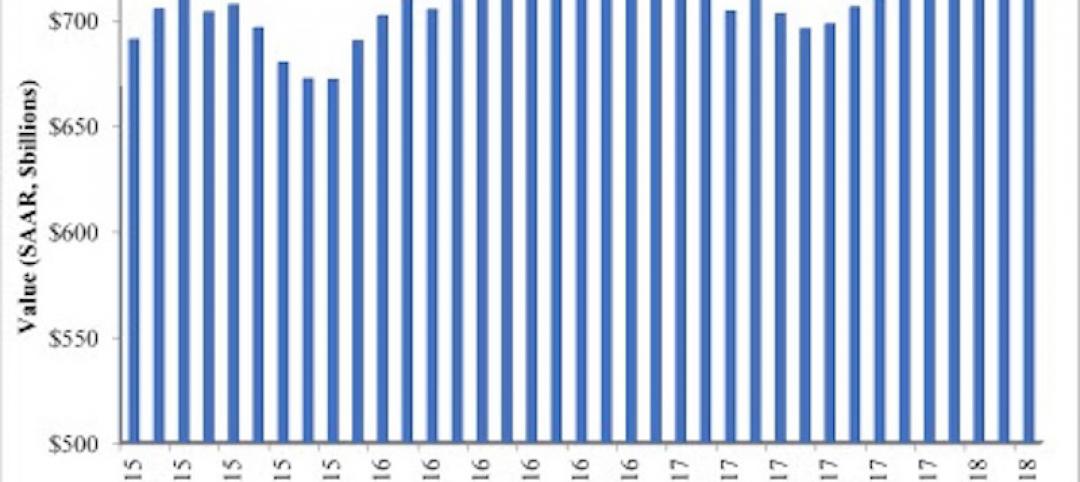

Construction spending in February totaled $1.52 trillion at a seasonally adjusted annual rate, a decrease of 0.8% from the pace in January. Although the overall total was 5.3% higher than in February 2020, the year-over-year gain was limited to residential construction, Simonson noted. That segment slipped 0.2% for the month but jumped 21% year-over-year. Meanwhile, combined private and public nonresidential spending declined 1.3% from January and 6.1% over 12 months.

Private nonresidential construction spending fell 1.0% from January to February and 9.7% since February 2020, with year-over-year decreases in all 11 subsegments. The largest private nonresidential category, power construction, retreated 9.7% year-over-year and 0.4% from January to February. Among the other large private nonresidential project types, commercial construction—comprising retail, warehouse and farm structures—slumped 7.1% year-over-year and 1.2% for the month. Manufacturing construction tumbled 10.4% from a year earlier despite a pickup of 0.3% in February. Office construction decreased 5.0% year-over-year and 0.5% in February.

Public construction spending dipped 0.9% year-over-year and 1.7% for the month. Among the largest segments, highway and street construction declined 1.0% from a year earlier and 0.6% for the month, while educational construction decreased 2.3 percent year-over-year and 3.2 percent in February. Spending on transportation facilities declined 2.3 percent over 12 months and 2.5 percent in February.

Association officials said that rising materials prices and unreliable delivery schedules are making it hard for firms to remain profitable as they have difficulty passing raising prices for construction work. They said that proposed new infrastructure projects will help boost demand for many types of construction projects. But they urged Washington officials to also take steps to address supply-chain challenges, including by ending tariffs on key materials like lumber and steel.

“Contractors are having a hard time finding work, and when they do, they are getting squeezed by rapidly rising materials prices,” said Stephen E. Sandherr, the association’s chief executive officer. “New infrastructure investments will certainly help with demand, but the industry also needs Washington to help address supply-chain problems and rising costs.”

Related Stories

Market Data | Jun 22, 2018

Multifamily market remains healthy – Can it be sustained?

New report says strong economic fundamentals outweigh headwinds.

Market Data | Jun 21, 2018

Architecture firm billings strengthen in May

Architecture Billings Index enters eighth straight month of solid growth.

Market Data | Jun 20, 2018

7% year-over-year growth in the global construction pipeline

There are 5,952 projects/1,115,288 rooms under construction, up 8% by projects YOY.

Market Data | Jun 19, 2018

ABC’s Construction Backlog Indicator remains elevated in first quarter of 2018

The CBI shows highlights by region, industry, and company size.

Market Data | Jun 19, 2018

America’s housing market still falls short of providing affordable shelter to many

The latest report from the Joint Center for Housing Studies laments the paucity of subsidies to relieve cost burdens of ownership and renting.

Market Data | Jun 18, 2018

AI is the path to maximum profitability for retail and FMCG firms

Leading retailers including Amazon, Alibaba, Lowe’s and Tesco are developing their own AI solutions for automation, analytics and robotics use cases.

Market Data | Jun 12, 2018

Yardi Matrix report details industrial sector's strength

E-commerce and biopharmaceutical companies seeking space stoke record performances across key indicators.

Market Data | Jun 8, 2018

Dodge Momentum Index inches up in May

May’s gain was the result of a 4.7% increase by the commercial component of the Momentum Index.

Market Data | Jun 4, 2018

Nonresidential construction remains unchanged in April

Private sector spending increased 0.8% on a monthly basis and is up 5.3% from a year ago.

Market Data | May 30, 2018

Construction employment increases in 256 metro areas between April 2017 & 2018

Dallas-Plano-Irving and Midland, Texas experience largest year-over-year gains; St. Louis, Mo.-Ill. and Bloomington, Ill. have biggest annual declines in construction employment amid continuing demand.