Both Nonresidential and Residential Spending Retreat from January Levels amid Extreme Winter Weather; Association Posts Inflation Alert to Aid Understanding of Squeeze on Nonresidential Construction Firms

Construction spending slumped in February as unseasonably severe weather hammered the industry and a decline in new projects squeezed nonresidential contractors experiencing rising costs and delivery times, according to an analysis of new federal construction spending data by the Associated General Contractors of America. The association posted a Construction Inflation Alert to inform project owners and government officials about the threat to project completion dates and contractors’ financial health.

“The downturn in February reflects both an unfavorable change from mild January weather and an ongoing decline in new nonresidential projects,” said Ken Simonson, the association’s chief economist. “Unfortunately, it will take more than mild weather to help nonresidential contractors overcome the multiple challenges of falling demand for many project types, steeply rising costs, and lengthening or uncertain delivery times for key materials.”

Construction spending in February totaled $1.52 trillion at a seasonally adjusted annual rate, a decrease of 0.8% from the pace in January. Although the overall total was 5.3% higher than in February 2020, the year-over-year gain was limited to residential construction, Simonson noted. That segment slipped 0.2% for the month but jumped 21% year-over-year. Meanwhile, combined private and public nonresidential spending declined 1.3% from January and 6.1% over 12 months.

Private nonresidential construction spending fell 1.0% from January to February and 9.7% since February 2020, with year-over-year decreases in all 11 subsegments. The largest private nonresidential category, power construction, retreated 9.7% year-over-year and 0.4% from January to February. Among the other large private nonresidential project types, commercial construction—comprising retail, warehouse and farm structures—slumped 7.1% year-over-year and 1.2% for the month. Manufacturing construction tumbled 10.4% from a year earlier despite a pickup of 0.3% in February. Office construction decreased 5.0% year-over-year and 0.5% in February.

Public construction spending dipped 0.9% year-over-year and 1.7% for the month. Among the largest segments, highway and street construction declined 1.0% from a year earlier and 0.6% for the month, while educational construction decreased 2.3 percent year-over-year and 3.2 percent in February. Spending on transportation facilities declined 2.3 percent over 12 months and 2.5 percent in February.

Association officials said that rising materials prices and unreliable delivery schedules are making it hard for firms to remain profitable as they have difficulty passing raising prices for construction work. They said that proposed new infrastructure projects will help boost demand for many types of construction projects. But they urged Washington officials to also take steps to address supply-chain challenges, including by ending tariffs on key materials like lumber and steel.

“Contractors are having a hard time finding work, and when they do, they are getting squeezed by rapidly rising materials prices,” said Stephen E. Sandherr, the association’s chief executive officer. “New infrastructure investments will certainly help with demand, but the industry also needs Washington to help address supply-chain problems and rising costs.”

Related Stories

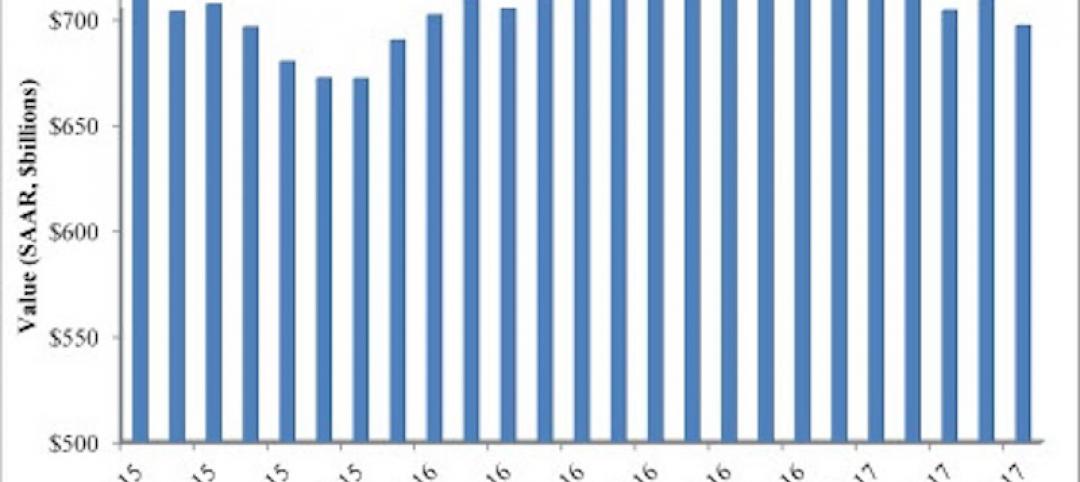

Market Data | Aug 2, 2017

Nonresidential Construction Spending falls in June, driven by public sector

June’s weak construction spending report can be largely attributed to the public sector.

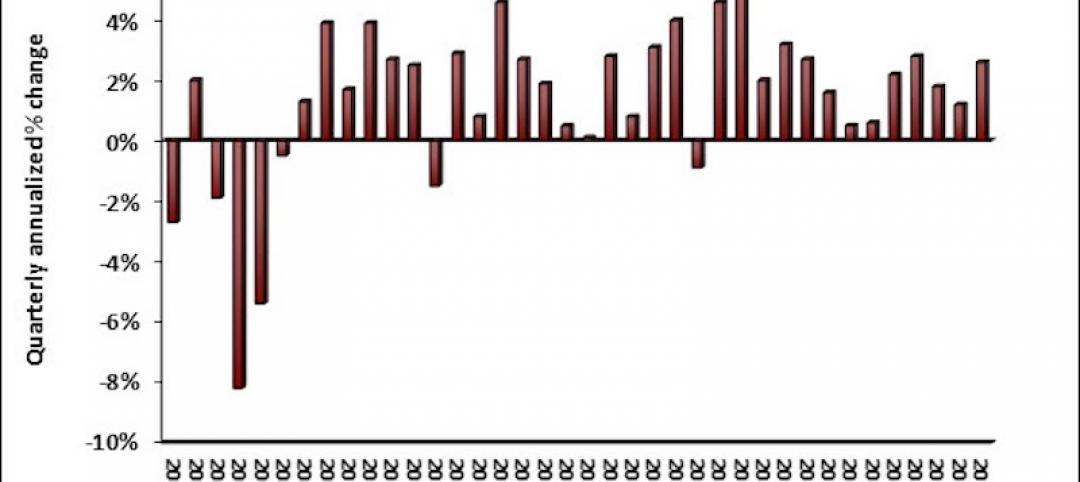

Market Data | Jul 31, 2017

U.S. economic growth accelerates in second quarter; Nonresidential fixed investment maintains momentum

Nonresidential fixed investment, a category of GDP embodying nonresidential construction activity, expanded at a 5.2% seasonally adjusted annual rate.

Multifamily Housing | Jul 27, 2017

Apartment market index: Business conditions soften, but still solid

Despite some softness at the high end of the apartment market, demand for apartments will continue to be substantial for years to come, according to the National Multifamily Housing Council.

Market Data | Jul 25, 2017

What's your employer value proposition?

Hiring and retaining talent is one of the top challenges faced by most professional services firms.

Market Data | Jul 25, 2017

Moderating economic growth triggers construction forecast downgrade for 2017 and 2018

Prospects for the construction industry have weakened with developments over the first half of the year.

Industry Research | Jul 6, 2017

The four types of strategic real estate amenities

From swimming pools to pirate ships, amenities (even crazy ones) aren’t just perks, but assets to enhance performance.

Market Data | Jun 29, 2017

Silicon Valley, Long Island among the priciest places for office fitouts

Coming out on top as the most expensive market to build out an office is Silicon Valley, Calif., with an out-of-pocket cost of $199.22.

Market Data | Jun 26, 2017

Construction disputes were slightly less contentious last year

But poorly written and administered contracts are still problems, says latest Arcadis report.

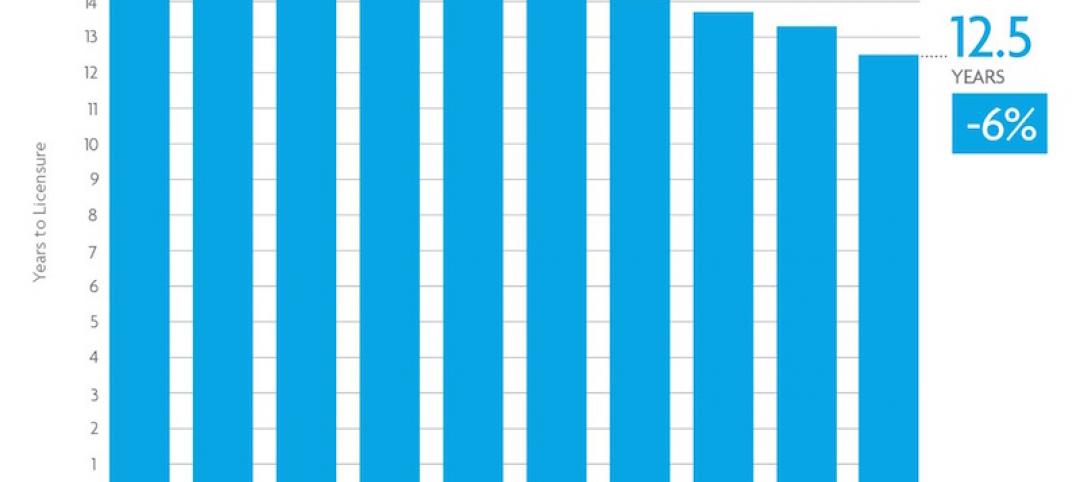

Industry Research | Jun 26, 2017

Time to earn an architecture license continues to drop

This trend is driven by candidates completing the experience and examination programs concurrently and more quickly.

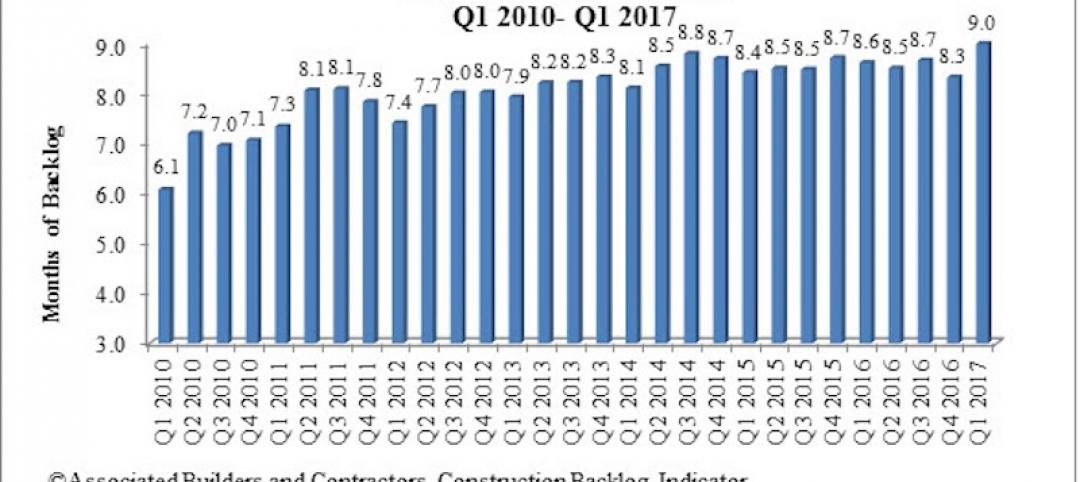

Industry Research | Jun 22, 2017

ABC's Construction Backlog Indicator rebounds in 2017

The first quarter showed gains in all categories.