Through the first half of 2022, nonresidential construction spending returned to “nomimal growth.” But JLL, in its Construction Outlook for the second half of the year, foresees nonresidential spending being flat, on an inflation-adjusted basis, and year-over-year growth returning to historical levels in 2024, “as disruptions are likely to persist into 2023.”

Those disruptions include supply-chain issues that contributed to construction materials costs increasing by 42.5 percent from prepandemic levels. Labor costs related to workforce shortages were 10.5 percent higher than they were in March 2020.

“Labor availability remains a deep-set structural challenge for the industry and will be a larger issue as construction demand persists and shifts focus,” JLL observes. “Estimates of future need based on these upcoming expenditures show the gap will only widen, with a particular need for nonbuilding and public workers.”

Too much work, too few workers

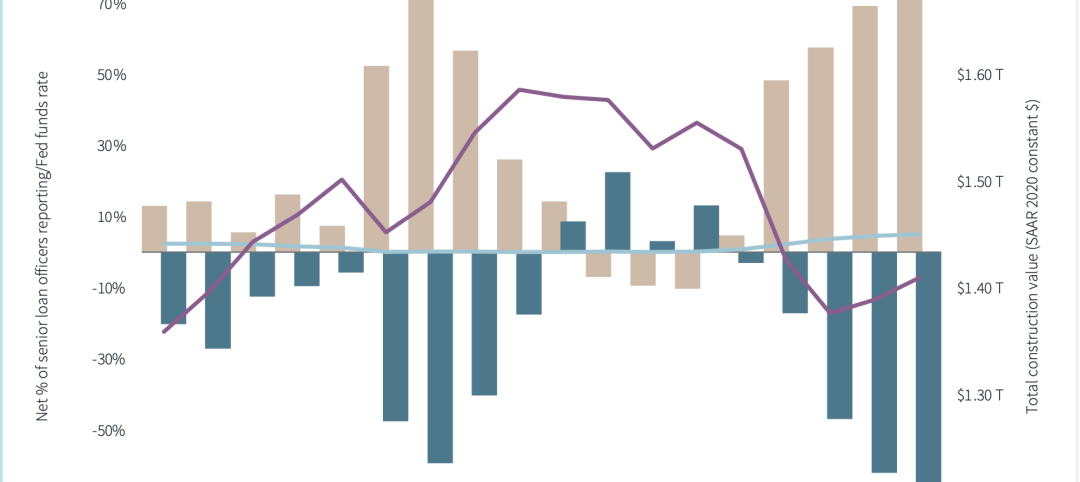

Job openings for construction labor have been consistently elevated, even as hiring expanded above prepandemic rates and separations fell to extremely low levels. In June 2022, unemployment fell to 3.7 percent, just 0.1 percent above the national average and job openings finally pulled back, dropping by 109,000 openings to 330,000. As such, the pullback is likely to continue, as firms stabilize backlogs and plan for difficult times.

Wage growth in the first half of 2022 was modest as well, significantly outpaced by inflation. Workers in the construction industry have actually experienced real wage losses of roughly 1.9 percent since the start of the pandemic. That gap widened in the first half of 2022 for construction employees.

“It is unlikely that the pullback will result in significantly lower demand side pressure in the construction labor market, as the current volume and array of work are sufficient to keep demand high for the next several years,” states JLL, especially once spending from the Infrastructure Investment and Jobs Act (IIJA) is in full swing.

The industry’s dilemma, however, is that it doesn’t have the capacity to fill every construction job that’s expected to be added in the next few years. At current forecasts of incoming IIJA funds bumping public spending by 10 percent or more annually from 2024 on, the increased need for construction employment equates to roughly 350,000 jobs from that spending alone —well above capacity identified in the historical record.

The largest impacts could be continued wage pressure and potential delays in projects. JLL predicts that the favorable situation for labor is expected to accelerate wage growth in the second half of the year, continuing to pressure margins. Though outright cancellations have remained limited, delays due to labor shortages are a nearly universal experience “with no relief in sight.”

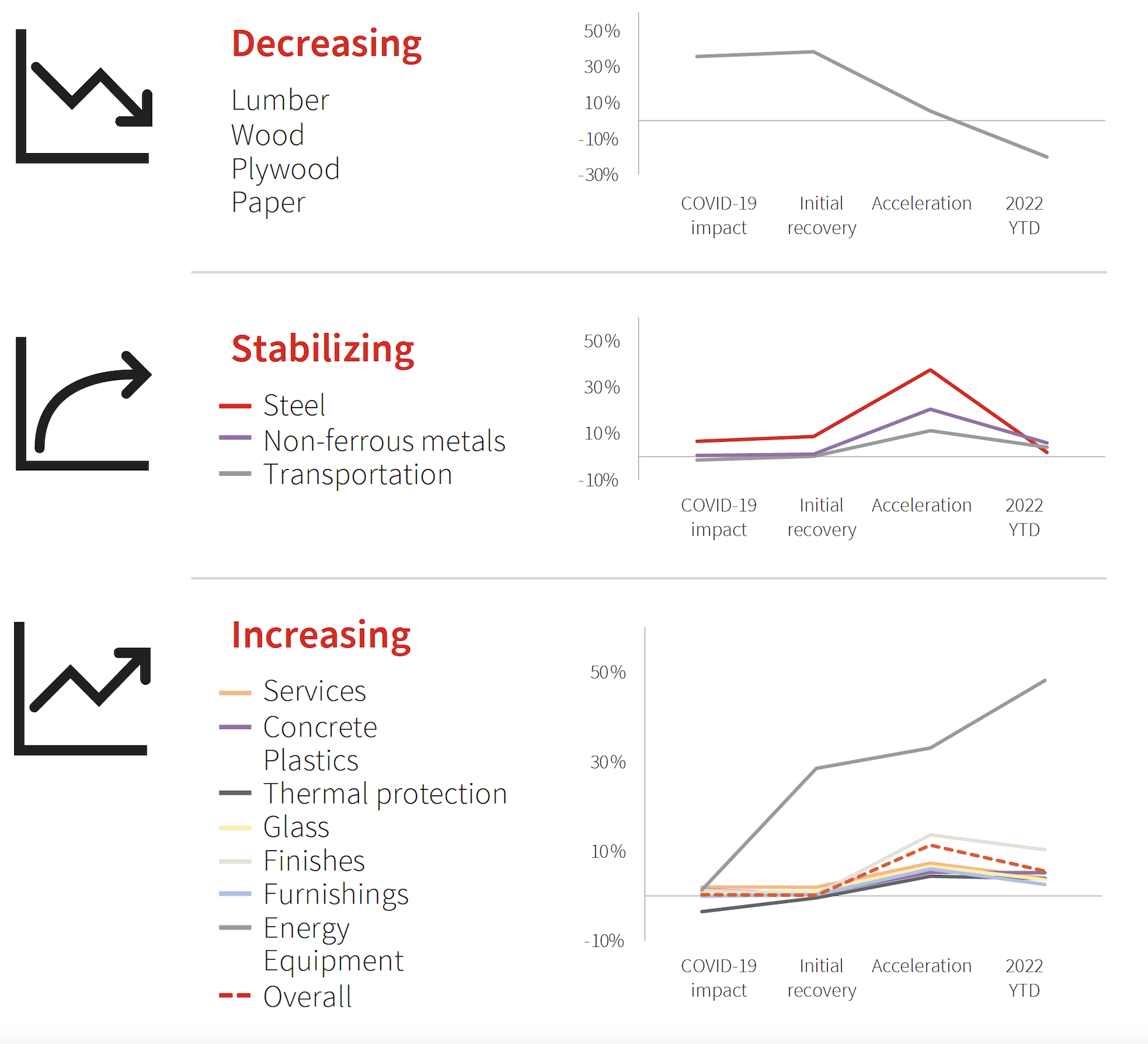

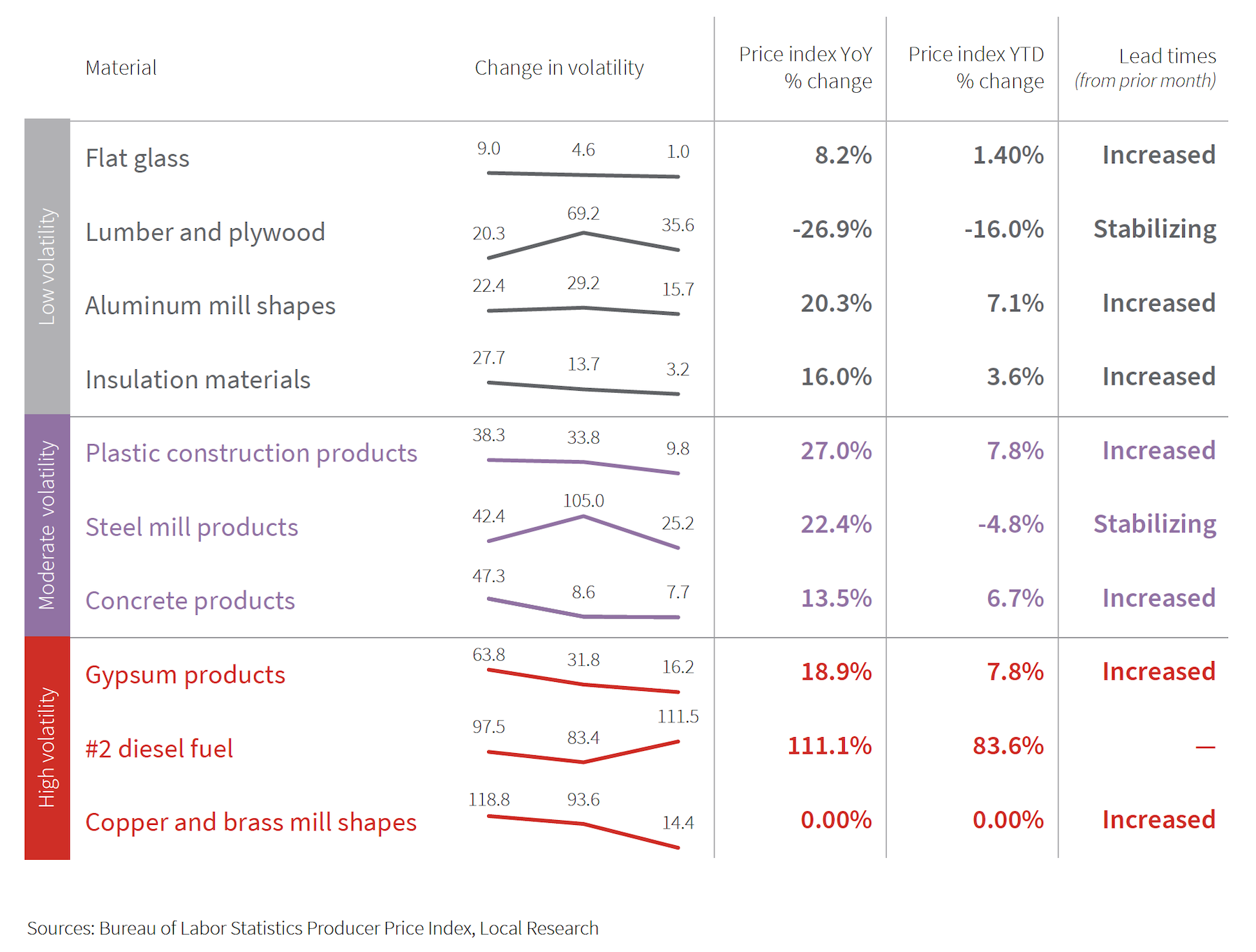

Uneven price stability

JLL’s Outlook is mixed about construction materials availability and costs. Steel and lumber, once the poster children for price inflation, have stabilized, thanks in part to domestic steel construction that’s 30 percent higher than prepandemic levels. However, “volatility has not gone down uniformly” across the spectrum of construction products.

That is particularly true of energy related materials that have been affected by Russia’s invasion of Ukraine, whose damages to its built environment are estimated at $750 billion and rising. Cement, glass manufacture, and semiconductors for equipment and machinery “are among some of the larger price increases,” with concrete and glass disproportionately reliant on few producers with extremely high energy usage for production. Plus, the 10 percent increase in domestic cement and concrete production hasn’t stabilized prices yet.

Consequently, JLL has revised its previous outlook and now projects that materials prices will be up between 12 and 18 percent this year. “Uncertainty is still widespread and, as demonstrated by the current changing patterns of costs, novel issues are likely to emerge and disrupt supply chains and pricing in the near term.”

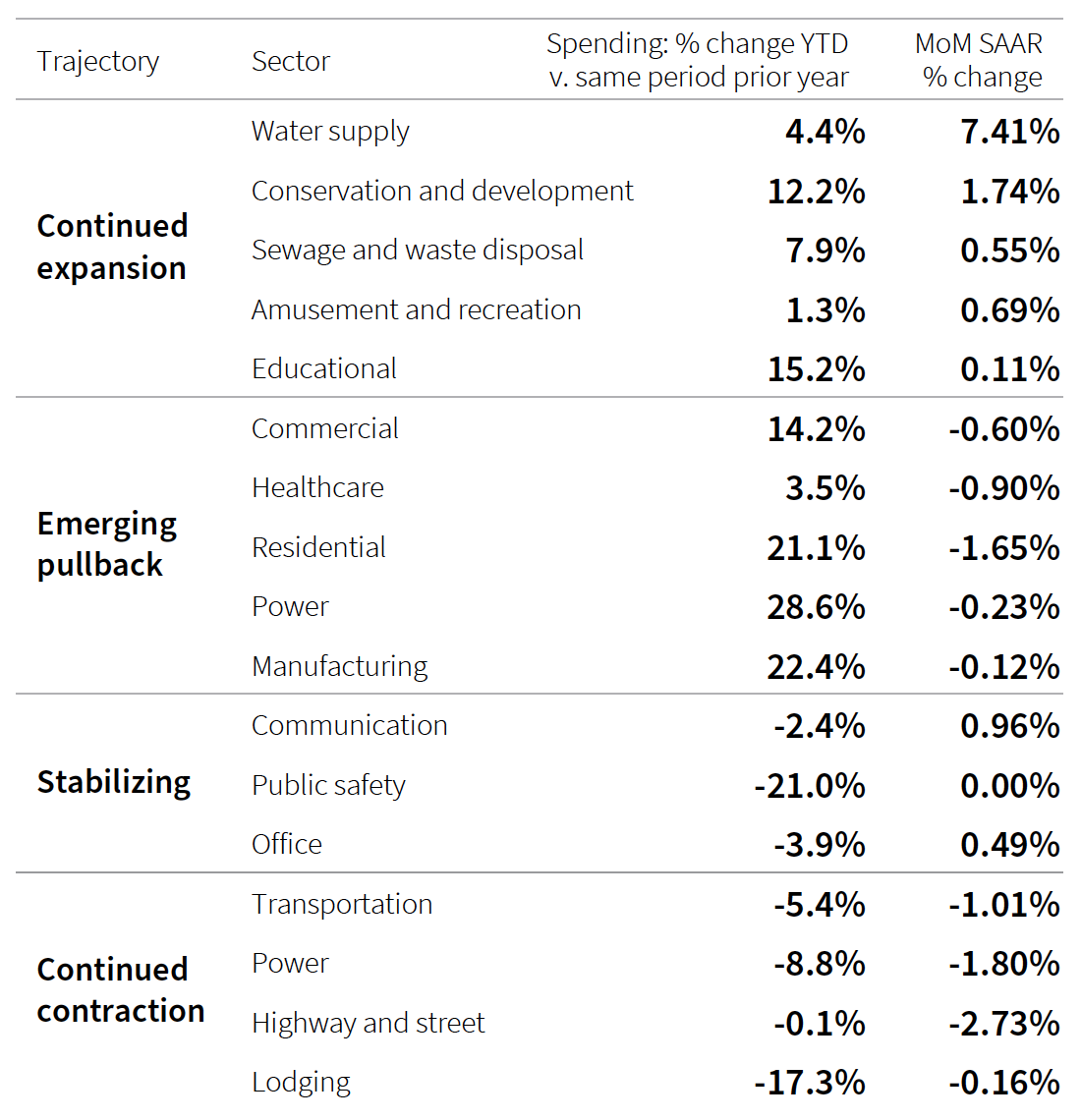

An active industry

From January to May 2022, the seasonally adjusted annual rate of total construction spending expanded at a monthly rate of 0.63 percent, above the growth rate observed in 2021. June, though, was down a percentage point, and any increases through the first half of the year were attributable to inflation.

On the bright side, JLL expects construction activity to remain healthy, global economic concerns notwithstanding. In the U.S., the Northeast has faltered with numerous months of contraction in the first half of 2022, while the West has picked up the pace of billing and backlog increases in recent months. The South and Midwest have maintained billings growth that is beginning to decelerate but will nevertheless create an appreciable pipeline of construction activity in the regions.

Related Stories

Contractors | Sep 12, 2023

The average U.S. contractor has 9.2 months worth of construction work in the pipeline, as of August 2023

Associated Builders and Contractors' Construction Backlog Indicator declined to 9.2 months in August, down 0.1 month, according to an ABC member survey conducted from Aug. 21 to Sept. 6. The reading is 0.5 months above the August 2022 level.

Contractors | Sep 11, 2023

Construction industry skills shortage is contributing to project delays

Relatively few candidates looking for work in the construction industry have the necessary skills to do the job well, according to a survey of construction industry managers by the Associated General Contractors of America (AGC) and Autodesk.

Market Data | Sep 6, 2023

Far slower construction activity forecast in JLL’s Midyear update

The good news is that market data indicate total construction costs are leveling off.

Giants 400 | Sep 5, 2023

Top 80 Construction Management Firms for 2023

Alfa Tech, CBRE Group, Skyline Construction, Hill International, and JLL top the rankings of the nation's largest construction management (as agent) and program/project management firms for nonresidential buildings and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Sep 5, 2023

Top 150 Contractors for 2023

Turner Construction, STO Building Group, DPR Construction, Whiting-Turner Contracting Co., and Clark Group head the ranking of the nation's largest general contractors, CM at risk firms, and design-builders for nonresidential buildings and multifamily buildings work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Market Data | Sep 5, 2023

Nonresidential construction spending increased 0.1% in July 2023

National nonresidential construction spending grew 0.1% in July, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.08 trillion and is up 16.5% year over year.

Giants 400 | Aug 31, 2023

Top 35 Engineering Architecture Firms for 2023

Jacobs, AECOM, Alfa Tech, Burns & McDonnell, and Ramboll top the rankings of the nation's largest engineering architecture (EA) firms for nonresidential buildings and multifamily buildings work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

Top 115 Architecture Engineering Firms for 2023

Stantec, HDR, Page, HOK, and Arcadis North America top the rankings of the nation's largest architecture engineering (AE) firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

2023 Giants 400 Report: Ranking the nation's largest architecture, engineering, and construction firms

A record 552 AEC firms submitted data for BD+C's 2023 Giants 400 Report. The final report includes 137 rankings across 25 building sectors and specialty categories.

Giants 400 | Aug 22, 2023

Top 175 Architecture Firms for 2023

Gensler, HKS, Perkins&Will, Corgan, and Perkins Eastman top the rankings of the nation's largest architecture firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.