Despite rising demand, the construction industry is expected to see a serious falloff in building starts, according Jones Lang Lasalle’s Construction Trends and Midyear Update, which JLL released this morning.

The report takes a fresh look at the industry’s overall health, the current availability and pricing for labor and materials, and the direction that total construction costs may be headed.

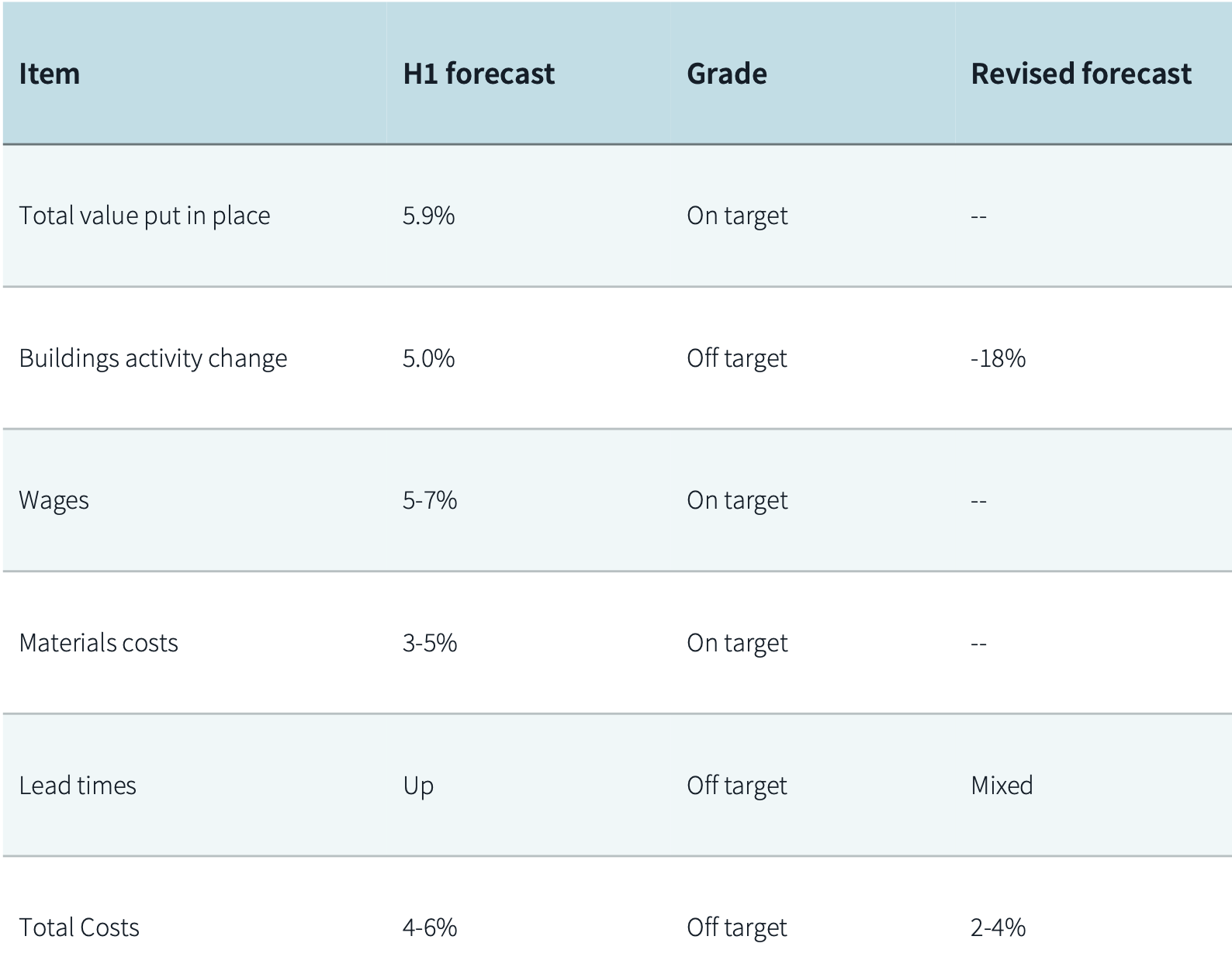

JLL still sees the construction sector in “uncharted economic territory,” as global threats remain unrealized “but full of disruptive potential” even as construction continues at breakneck speed to address post-pandemic built-environment needs. Consequently, JLL updated its projections for three of the seven barometers it tracks (see chart).

The outlook’s four key takeaways are:

•Industry Health: Financing constraints have driven a rapid decline in construction starts over the last quarter;

•Labor: Firms are prioritizng talent retention strategies;

•Materials: Supply chain issues have largely stabilized, and future cost increases should be manageable;

•Total Costs: Firms' responses to the impending slowdown have led to a drop in total costs during the third quarter, prompting JLL to revise its total cost growth forecast down to 2-4%, from 4-6% in the first half of the year.

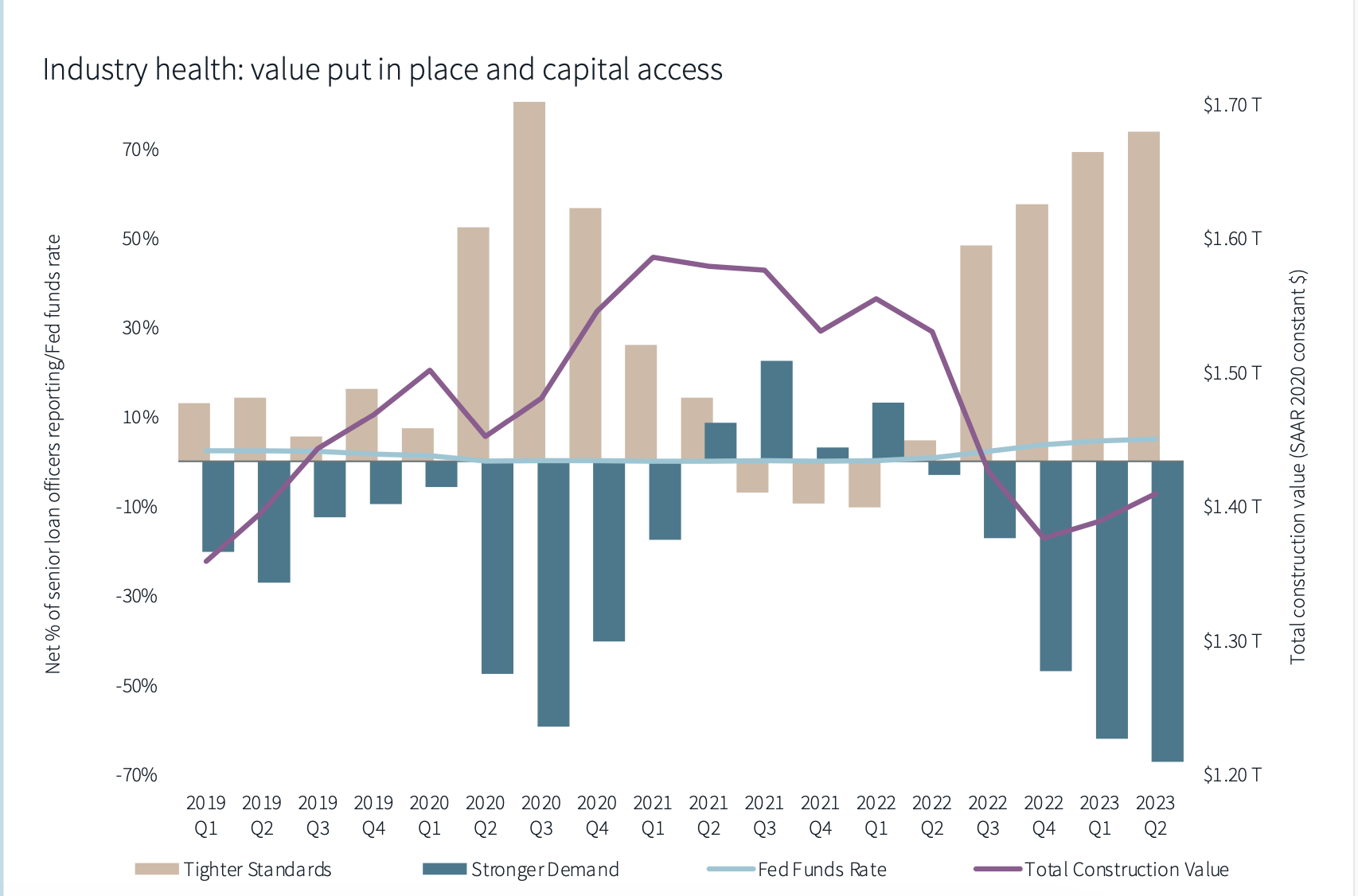

Interest rates are curtailing building starts

Based on midyear data, JLL’s forecast for construction value put in place aligns with its previous expectations. Overall, industry sentiment is strong, but construction is expected to cool depending on resolution or escalation of threats ranging from inflation to geopolitical turmoil. JLL’s revised forecast anticipates an 18% decline in building activity, compared with its 5% growth forecast for the first half of the year.

Rising interest rates are slowing construction starts. But demand for infrastructure and other non-building projects remains strong. JLL predicts interest rates will peak near the end of this year, and construction activity should rev up, “with specialization and complexity management playing vital roles.“

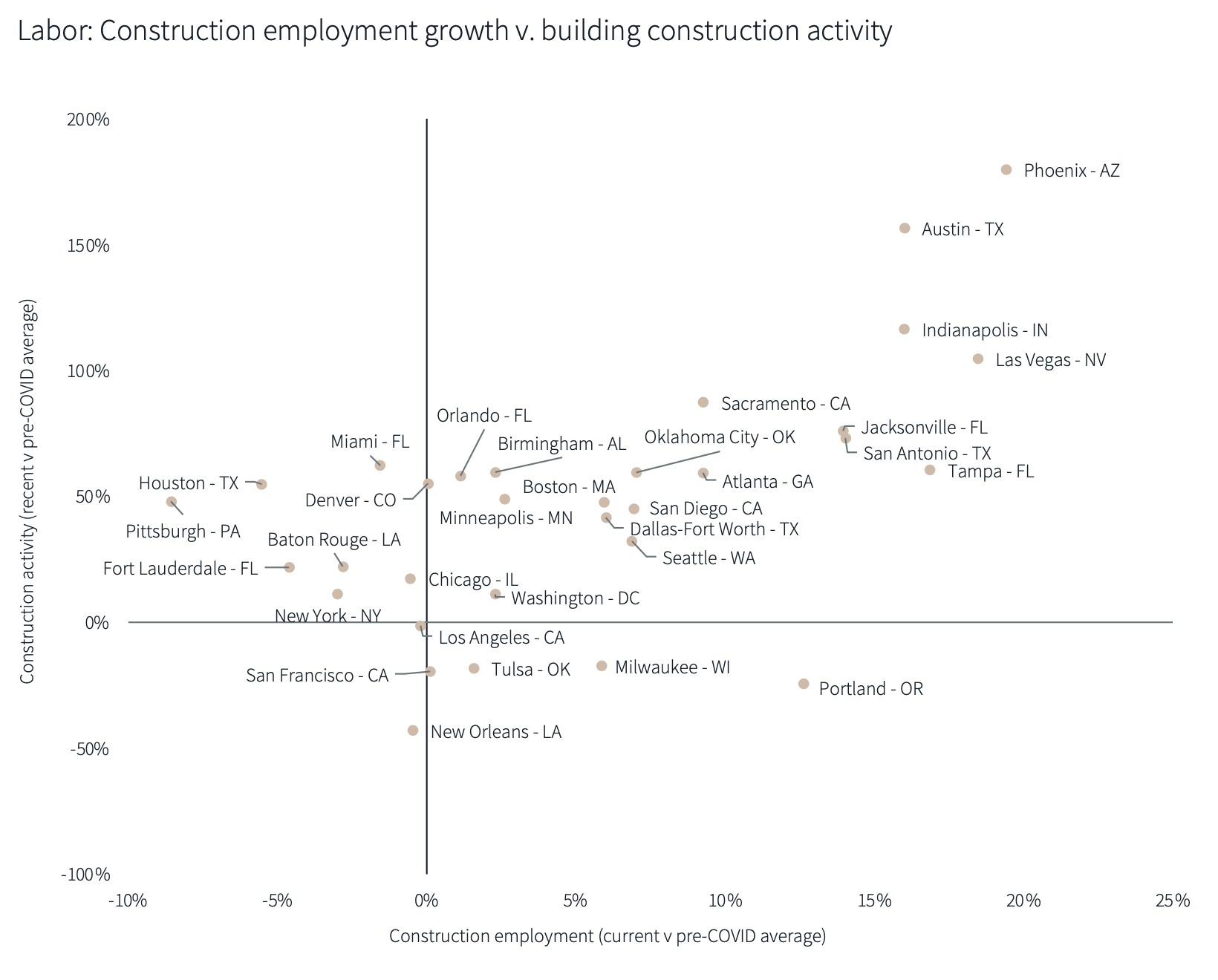

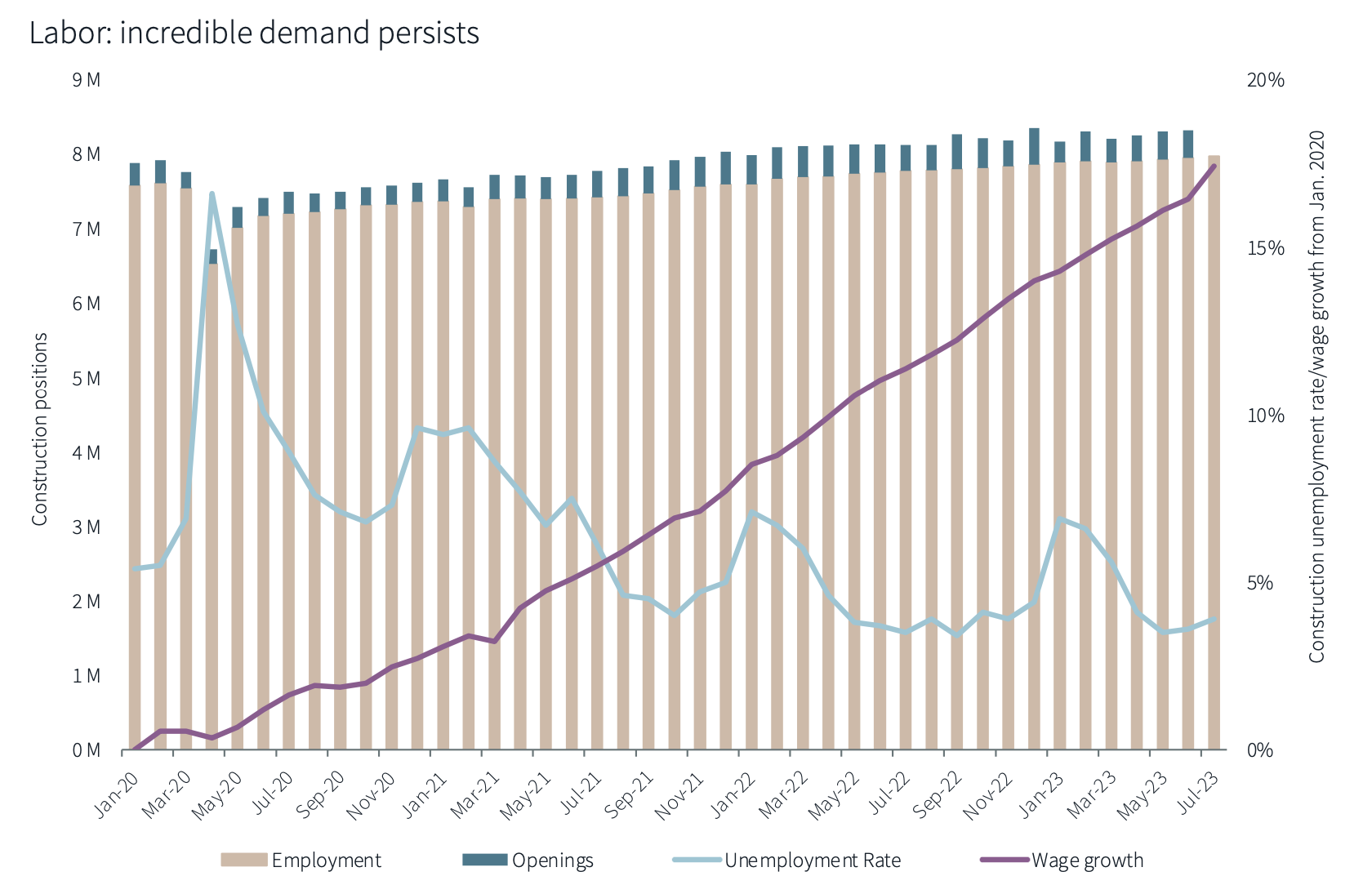

JLL continues to stand by its forecast of 5-7% growth in labor costs. Job openings remain high, and unemployment is unusually low. There is “persistent” wage competition for skilled workers. However, contractors remain confident about their ability to weather the expected downturn. JLL foresees minimal disruption in sectors buoyed by public sector spending; other sectors could see more of a dropoff, though. Construction activity per employee will remain above pre-pandemic levels for the foreseeable future.

Total costs are stabilizing

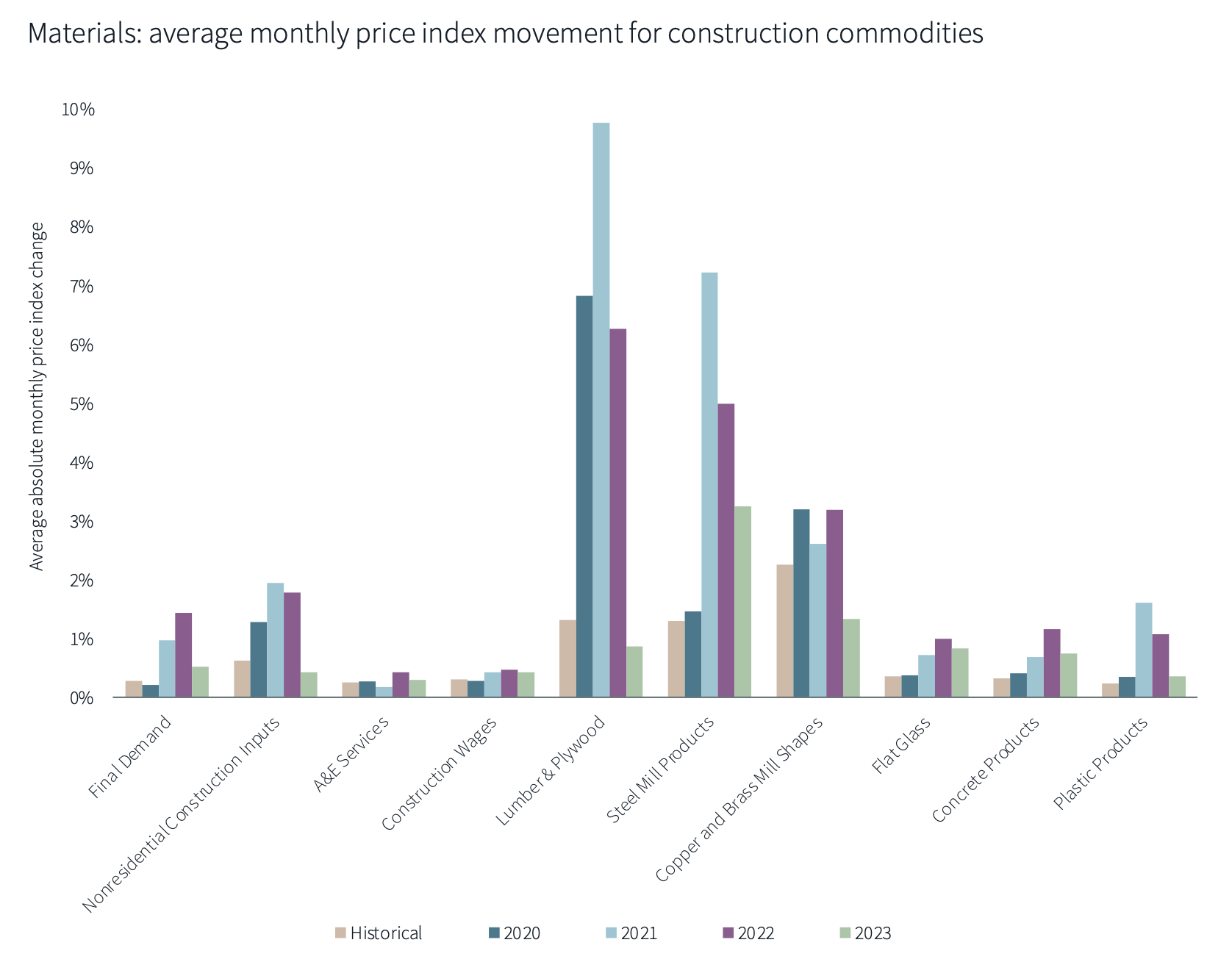

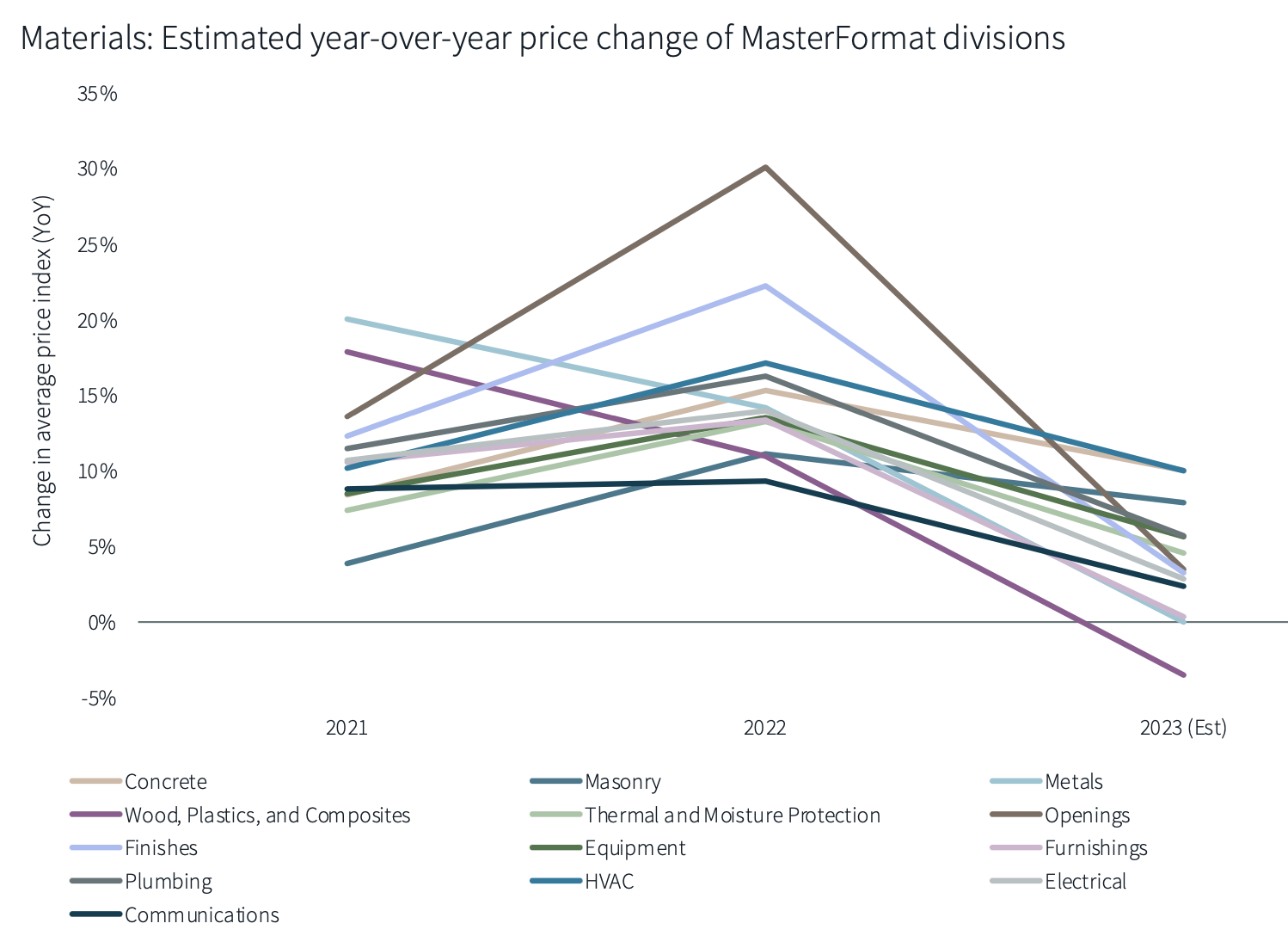

JLL also believes that its prediction of a 3-5% increase in materials costs remains on target. Commodities are exhibiting varying price fluctuations. Lead times were high in the first half of 2023, especially for MEP goods, making it harder for contractors to keep up with electrification and data center demand. Steel, concrete, glass, and plastic products’ price movements are also above historic levels. JLL expects materials costs to continue to rise at their current modest (single-digit) pace, having less impact on demand. But summer wildfires are likely to impact the supply of Canadian softwood.

Mixing these factors, JLL concludes that total construction costs have stabilized, having recorded the slowest period of growth (and the first declines) since the immediate aftermath of COVID-19 being declared a global emergency. Firms are navigating wage hikes, and expect sales and profit to grow modestly and stabilize, respectively. Labor retention is a priority to hold the line on costs. JLL adjusts its projection for total cost growth down to between 2-4%, from 4-6% in the first half.

Related Stories

Market Data | Sep 23, 2020

Architectural billings in August still show little sign of improvement

The pace of decline during August remained at about the same level as in July and June.

Market Data | Sep 23, 2020

7 must reads for the AEC industry today: September 23, 2020

The new Theodore Presidential Library and the AIA/HUD's Secretary's Awards honor affordable, accessible housing.

Market Data | Sep 22, 2020

6 must reads for the AEC industry today: September 22, 2020

Construction employment declined in 39 states and no ease of lumber prices in sight.

Market Data | Sep 21, 2020

Washington is the US state with the most value of construction projects underway, says GlobalData

Of the top 10 largest projects in the Washington state, nine were in the execution stage as of August 2020.

Market Data | Sep 21, 2020

Construction employment declined in 39 states between August 2019 and 2020

31 states and DC added jobs between July and August.

Market Data | Sep 21, 2020

6 must reads for the AEC industry today: September 21, 2020

Four projects receive 202 AIA/ALA Library Building Award and Port San Antonio's new Innovation Center.

Market Data | Sep 18, 2020

Follow up survey of U.S. code officials demonstrates importance of continued investment in virtual capabilities

Existing needs highlight why supporting building and fire prevention departments at the federal, state, and local levels is critical.

Market Data | Sep 18, 2020

6 must reads for the AEC industry today: September 18, 2020

Sagrada Familia completion date pushed back and energy code appeals could hamper efficiency progress.

Market Data | Sep 17, 2020

6 must reads for the AEC industry today: September 17, 2020

Foster + Partners-designed hospital begins construction in Cairo and heat pumps are the future for hot water.

Market Data | Sep 16, 2020

6 must reads for the AEC industry today: September 16, 2020

REI sells unused HQ building and Adjaye Associates will design The Africa Institute.