Most contractors expect demand for many types of construction to shrink in 2021 even as the pandemic is prompting many owners to delay or cancel already-planned projects, meaning few firms will hire new workers, according to survey results released today by the Associated General Contractors of America and Sage Construction and Real Estate. The findings are detailed in The Pandemic’s Growing Impacts on the Construction Industry: The 2021 Construction Hiring and Business Outlook Report.

“This is clearly going to be a difficult year for the construction industry,” said Stephen E. Sandherr, the association's chief executive officer. “Demand looks likely to continue shrinking, projects are getting delayed or canceled, productivity is declining, and few firms plan to expand their headcount.”

The percentage of respondents who expect a market segment to contract exceeds the percentage who expect it to expand – known as the net reading – in 13 of the 16 categories of projects included in the survey. Contractors are most pessimistic about the market for retail construction, which has a net reading of negative 64%. They are similarly concerned about the markets for lodging and private office construction, which both have a net reading of negative 58%.

Other construction categories with a high negative net reading include higher education construction, which has a net reading of negative 40%; public buildings, with a net negative of 38%, and K-12 school construction which has a net reading of negative 27%. Among the three market segments with a positive net reading, two – warehouse construction (+4%) and the construction of clinics, testing facilities and medical labs (+11%) – track closely with the few segments of the economy to benefit from the impacts of the coronavirus.

Firms report that many of their already-scheduled projects have either been delayed or canceled. Fifty-nine percent of firms report they had projects scheduled to start in 2020 that have been postponed until 2021. Forty-four percent report they had projects canceled in 2020 that have not been rescheduled. Eighteen percent of firms report that projects scheduled to start between January and June 2021 have been delayed. And 8% report projects scheduled to start in that time frame have been canceled.

Few firms expect the industry will recover to pre-pandemic levels soon. Only one-third of firms report business has already matched or exceeded year-ago levels, while 12% of firms expect demand to return to pre-pandemic levels within the next six months. Fifty-five percent report they either do not expect their firms’ volume of business to return to pre-pandemic levels for more than six months or they are unsure when their businesses will recover.

Only 35% of firms report they plan to add staff this year. Meanwhile, 24% plan to decrease their headcount in 2021 and 41 percent expect to make no changes in staff size. Firms do vary by region in their hiring outlook. In the South, the percentage of firms that expect to add employees – 39 percent – is more than double the percentage that expect to reduce headcount – 17 percent. The outlook among firms in the Northeast is nearly opposite: fewer than one-quarter of respondents expect to increase their headcount in 2021 while 41 percent foresee a reduction.

Despite the low hiring expectations, most contractors report it remains difficult to fill some or all open positions. Fifty-four percent of firms report difficulty finding qualified workers to hire, either to expand headcount or replace departing staff. And 49% expect it will either get harder, or remain as hard, to find qualified workers in 2021.

“The unfortunate fact is too few of the newly unemployed are considering construction careers, despite the high pay and significant opportunities for advancement,” said Ken Simonson, the association's chief economist. “The pandemic is also undermining construction productivity as contractors make significant changes to project staffing to protect workers and communities from the virus.”

Simonson noted that 64% of contractors report their new coronavirus procedures mean projects are taking longer to complete than originally anticipated. And 54% of firms report that the cost of completing projects has been higher than expected.

Officials with Sage noted that firms are being more strategic about information technology as they try to remain competitive in the current environment. Sixty-two percent of contractors indicate they currently have a formal IT plan that supports business objectives, up from 48% last year. An additional 7% plan to create a formal plan in 2021.

“While the past year has been filled with many challenges, technology has played an integral role in keeping people connected and businesses up and running,” said Dustin Anderson, vice president of Sage Construction and Real Estate. “While many firms have had to scale back other investments, technology remains an important part of most business plans as we move into the new year.”

Anderson added that most firms plan to keep their technology investment about the same as last year. When asked whether they planned to increase or decrease investment or stay the same in 15 different types of technologies, the majority of respondents – ranging between 71 and 89% – said their investments would remain the same as last year.

“The outlook for the industry could improve, however, if federal officials are able to boost investments in infrastructure, backfill state and local construction budgets and avoid the temptation to impose costly new regulatory barriers,” Sandherr said “But even as we work to advocate for measures to rebuild demand for construction, we also need to take longer-term steps to continue developing the construction workforce.”

Association officials noted with traffic still below pre-pandemic levels and a large pool of workers available, now is an ideal time to improve highways, repair transit systems, upgrade airports, modernize waterways and otherwise improve other types of public works. They added that one of the lessons from the late 2000s is that boosting federal infrastructure investments without backfilling state and local construction budgets is counterproductive. And that Congress and the incoming administration need to appreciate the risks of imposing burdensome new regulatory measures on an already-crippled economy.

Sandherr said the association is addressing the workforce challenge by crafting a new plan that focuses on continued advocacy, helping chapters and members establish or improve training programs and launching a new, national workforce recruiting effort. This new effort, “Construction is Essential,” will use targeted digital advertising to complement and build on the many existing local and regional construction workforce campaigns already in place.

“Our objective is to make sure contractors end the year on a far better note than many are starting it,” Sandherr said.

The Outlook was based on survey results from more than 1,300 firms from all 50 states and the District of Columbia. Varying numbers responded to each question. Contractors of every size answered over 20 questions about their hiring, workforce, business and information technology plans. Click here for The Pandemic’s Growing Impacts on the Construction Industry: The 2021 Construction Hiring and Business Outlook Report. Click here for the survey results. Click here for a brief video summarizing the findings.

Related Stories

Senior Living Design | May 9, 2017

Designing for a future of limited mobility

There is an accessibility challenge facing the U.S. An estimated 1 in 5 people will be aged 65 or older by 2040.

Industry Research | May 4, 2017

How your AEC firm can go from the shortlist to winning new business

Here are four key lessons to help you close more business.

Engineers | May 3, 2017

At first buoyed by Trump election, U.S. engineers now less optimistic about markets, new survey shows

The first quarter 2017 (Q1/17) of ACEC’s Engineering Business Index (EBI) dipped slightly (0.5 points) to 66.0.

Market Data | May 2, 2017

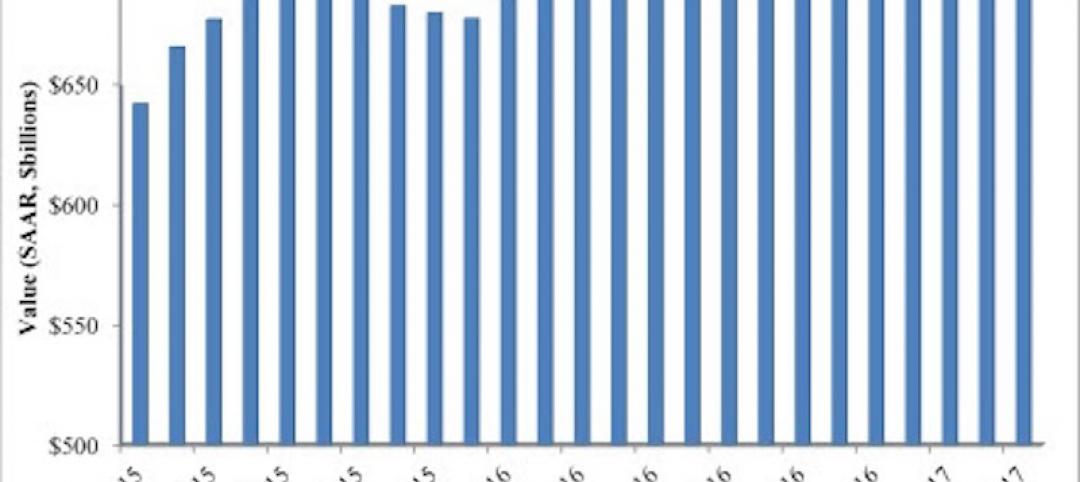

Nonresidential Spending loses steam after strong start to year

Spending in the segment totaled $708.6 billion on a seasonally adjusted, annualized basis.

Market Data | May 1, 2017

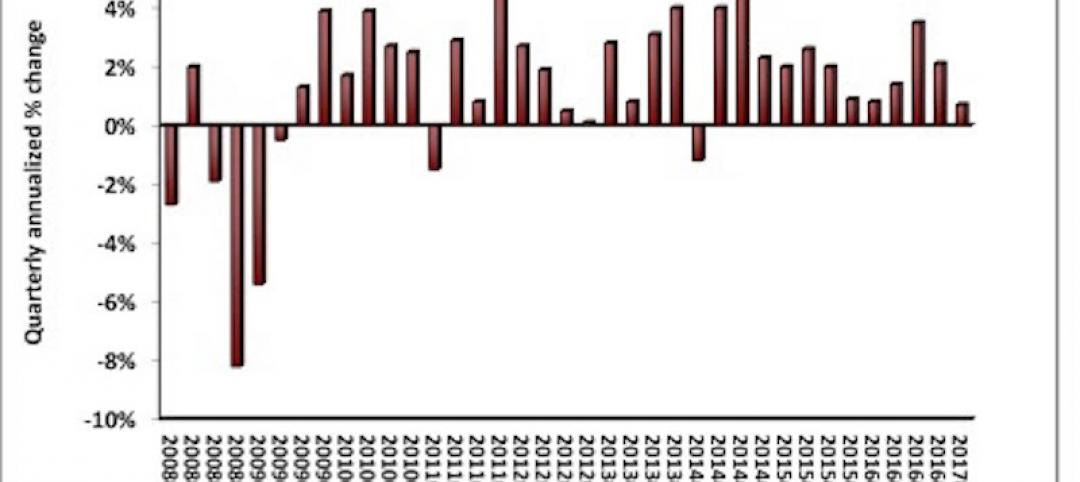

Nonresidential Fixed Investment surges despite sluggish economic in first quarter

Real gross domestic product (GDP) expanded 0.7 percent on a seasonally adjusted annualized rate during the first three months of the year.

Industry Research | Apr 28, 2017

A/E Industry lacks planning, but still spending large on hiring

The average 200-person A/E Firm is spending $200,000 on hiring, and not budgeting at all.

Market Data | Apr 19, 2017

Architecture Billings Index continues to strengthen

Balanced growth results in billings gains in all regions.

Market Data | Apr 13, 2017

2016’s top 10 states for commercial development

Three new states creep into the top 10 while first and second place remain unchanged.

Market Data | Apr 6, 2017

Architecture marketing: 5 tools to measure success

We’ve identified five architecture marketing tools that will help your firm evaluate if it’s on the track to more leads, higher growth, and broader brand visibility.

Market Data | Apr 3, 2017

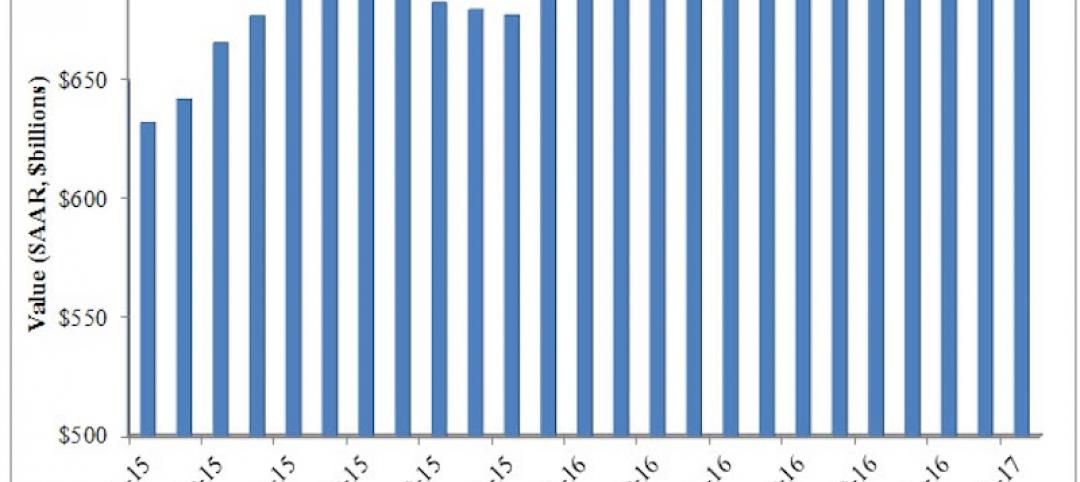

Public nonresidential construction spending rebounds; overall spending unchanged in February

The segment totaled $701.9 billion on a seasonally adjusted annualized rate for the month, marking the seventh consecutive month in which nonresidential spending sat above the $700 billion threshold.