The overall economy, as well as the economy in which they do business, might be down, but contractor panelists who provided these insights still see nonresidential construction on the upswing, according to FMI’s Second Quarter Nonresidential Construction Index (NRCI) Report.

Raleigh, N.C.-based FMI provides management consulting, investment banking, and people development services. Its quarterly index is based on voluntary responses from panelists to a 10-minute survey. The respondents represent a fairly wide cross-section of trades, company sizes, and markets. About 15% of the respondents are national contractors, 56% are Commercial General Building Contractors, and 39% operate businesses that generate between $51 million and $200 million in annual revenue. FMI declined to provide the number of panelists surveyed.

Chart: FMI

Chart: FMI

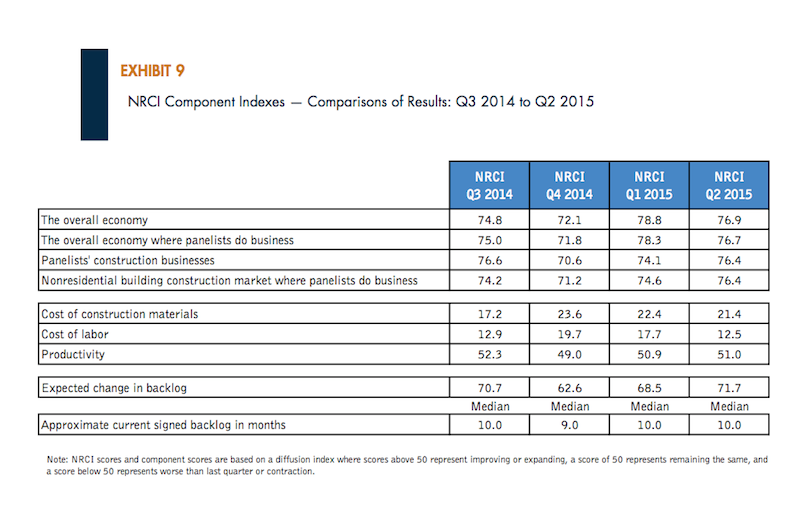

The NRCI for the second quarter was 64.9, virtually unchanged from the first quarter but improved from the 62.8 Index in the second quarter of 2014. FMI states that scores above 50 indicate expansion.

The panelists’ business outlook for specific nonresidential sectors is more ambivalent, however. Indices for healthcare and office construction are up, compared to a year ago, but down (albeit still on the growth side) for education, lodging, and manufacturing.

These scores might reflect the panelists’ perceptions of a still-volatile overall economy, whose second-quarter Index of 76.9 is down from the 78.8 Index in the first quarter. The panelists report that their own markets’ economies are off, too.

On the other hand, the panelists report improving productivity and steady backlogs. Half of the panelists said that their second-quarter backlogs grew faster than the previous quarter.

The indices for costs of materials and labor are down from the previous quarterly and yearly measurements, meaning those costs are rising. The NRCI Index for Construction Materials stood at 21.4, and 58.1% of the panelists said their materials costs increased from the first quarter. The Labor Cost Index was at 12.5, with 75% of the panelists reporting that their labor costs were higher in the second quarter than the first.

Chart: FMI

Chart: FMI

The survey also found that:

• Green construction made up only 28.6 percent of the panelists’ second-quarter backlogs, on average. FMI concludes from this finding that contractors no longer see green as anything special because it has become engrained into the mainstream of their businesses.

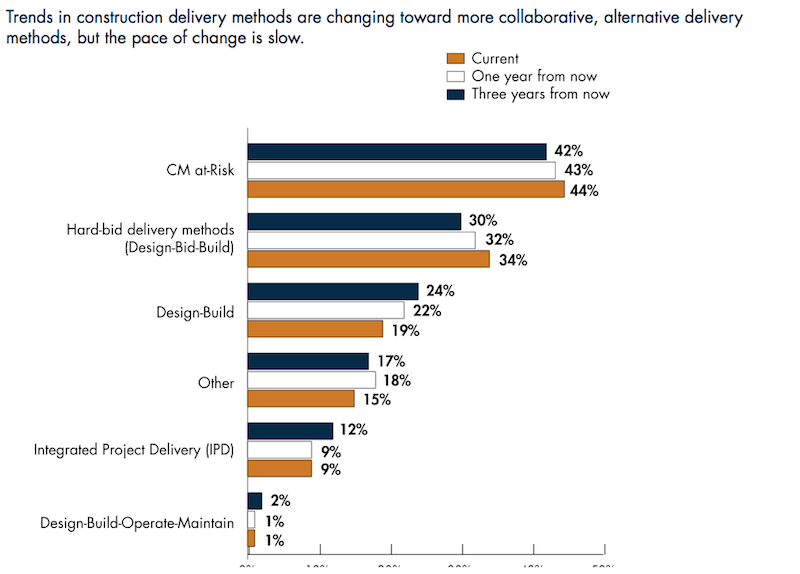

• The expediency of certain delivery methods during the recession is slowly yielding to more collaborative approaches among Building Teams and owners. “CM at-Risk is now allowed by most states, but those building CM at-Risk projects won’t quickly move to IPD [integrated project delivery].” FMI writes. “Design-build and IPD are expected to be growth areas for delivery methods; but IPD in particular, even though it offers many benefits to all parties, is not for everyone at this time. IPD, and even what has been called IPDish, requires more sophisticated owners, designers and contractors in order to realize the full benefits of this delivery approach.”

• Based on the panelists’ responses, FMI notes that other trends in construction—such as prefabrication, modularization, use of robotics, and 3D printing—are also likely to take a longer time to become mainstream like green construction has. “But the ongoing shortages of skilled labor will certainly hasten their coming.”

Related Stories

Market Data | Apr 2, 2018

Construction spending in February inches up from January

Association officials urge federal, state and local officials to work quickly to put recently enacted funding increases to work to improve aging and over-burdened infrastructure, offset public-sector spending drops.

Contractors | Mar 27, 2018

Shawmut Design and Construction’s burgeoning L.A. office looks to hospitality and interiors for future growth

A new division also taps the luxury homes market.

Contractors | Mar 9, 2018

Undoing 5 myths of IPD and Lean construction

The Lean Construction Institute, one of this year’s Movers+Shapers, has been sponsoring valuable research recently.

Contractors | Mar 6, 2018

Skender revolutionizes how the industry builds, integrates design, construction, and manufacturing

Envisioning a radically more efficient future for the building industry, Skender announces its expansion beyond construction, becoming a vertically integrated company including construction, design and building component manufacturing functions. The expansion includes significant investment in the launch of a new Chicago-based advanced manufacturing subsidiary and the acquisition of the boutique design firm Ingenious Architecture.

Multifamily Housing | Mar 4, 2018

Katerra, a tech-driven GC, plots ambitious expansion

Investors flock to this vertically integrated startup, which automates its design and construction processes.

Office Buildings | Feb 13, 2018

Office market vacancy rate at 10-year low

Cautious development and healthy absorption across major markets contributed to the decline in vacancy, according to a new Transwestern report.

Contractors | Feb 2, 2018

Construction employers add 36,000 jobs in January and 226,000 over the year

Industry employment is most since August 2008 As unemployment rate falls sharply.

Healthcare Facilities | Feb 1, 2018

Early supplier engagement provides exceptional project outcomes

Efficient supply chains enable companies to be more competitive in the marketplace.

Industry Research | Jan 30, 2018

AIA’s Kermit Baker: Five signs of an impending upturn in construction spending

Tax reform implications and rebuilding from natural disasters are among the reasons AIA’s Chief Economist is optimistic for 2018 and 2019.

Market Data | Jan 30, 2018

AIA Consensus Forecast: 4.0% growth for nonresidential construction spending in 2018

The commercial office and retail sectors will lead the way in 2018, with a strong bounce back for education and healthcare.