A new research report explores the past, present, and future of the workplace and reveals how organizations are using new strategies to improve the productivity and success of employees.

The International Facility Management Association (IFMA) released Distributed Work Revisited: Research Report #37, which is a follow-up to its 2009 Distributed Work report. Workplace strategy and design experts HOK helped IFMA develop and analyze the survey, collect the case studies and write the report.

IFMA members from 538 different organizations worldwide—83% were from the U.S. and Canada—completed an online questionnaire about their on- and off-site workplace accommodations, operational needs, technologies, specific facilities, change management processes and measurements for success. The area occupied by participating organizations ranges from 50,000 to more than 1 million sf. Distributed Work Revisited summarizes the complete survey results and provides a detailed analysis of the findings.

The report features case studies describing innovative distributed work programs across different stages of maturity in eight organizations: Microsoft, GSK, eBay, Credit Suisse, the U.S. General Services Administration, Accenture, Rockwell Collins and the City of Calgary. Results of the study reveal some surprising details about today’s workplace. Highlights include:

• Distributed work is still a relatively new concept. Sixty-one percent of facility professionals responding to this survey reported using unassigned workspaces in their facilities. Only 18% of survey participants have had a distributed work program in place for more than 10 years and 37% for more than five years.

• One hundred percent of survey respondents who reported implementing unassigned on-site distributed work options cited work-life balance as being a “very important” reason for doing so. Other factors listed as “very important” were to accommodate changes in the organization’s size (64%), leverage new technology (62%), increased productivity (60%), align with organizational goals (59%), cost savings (57%), improved flexibility (56%) and benefits for employees (55%).

• Employee benefits are the major drivers for off-premise solutions, enabling organizations to improve flexibility and support work-life balance.

• Respondents reported that distributed work strategies appeal most to Generation X (aged 35-48) employees, possibly because they work more independently than other groups and are more likely to have family commitments that require flexibility in how and where they work.

• The most popular on-site distributed work settings among respondents are spaces that promote collaboration and innovation, including war/project rooms (72%), huddle rooms (70%) and open lounge/soft seating areas (67%).

• More organizations are providing incentives to employees adopting distributed work. Thirty-three percent of respondents reported that when they adopted a distributed work policy, they provided an incentive—typically technology such as a laptop or mobile device—to employees. This is up from 18% in 2009.

• More organizations are measuring the results of their distributed work programs. Almost one-third of the organizations engage their workforces in testing and carrying out distributed work settings. This is up from 19% in 2009.

• Despite the expressed importance of employee engagement and satisfaction in achieving successful distributed work programs stated in the interviews, only 45% of the respondents mentioned use of change management processes.

The complete version of Distributed Work Revisited: Research Report #37 is available for sale on IFMA’s website. Funds raised support ongoing and future research.

Related Stories

Market Data | May 2, 2017

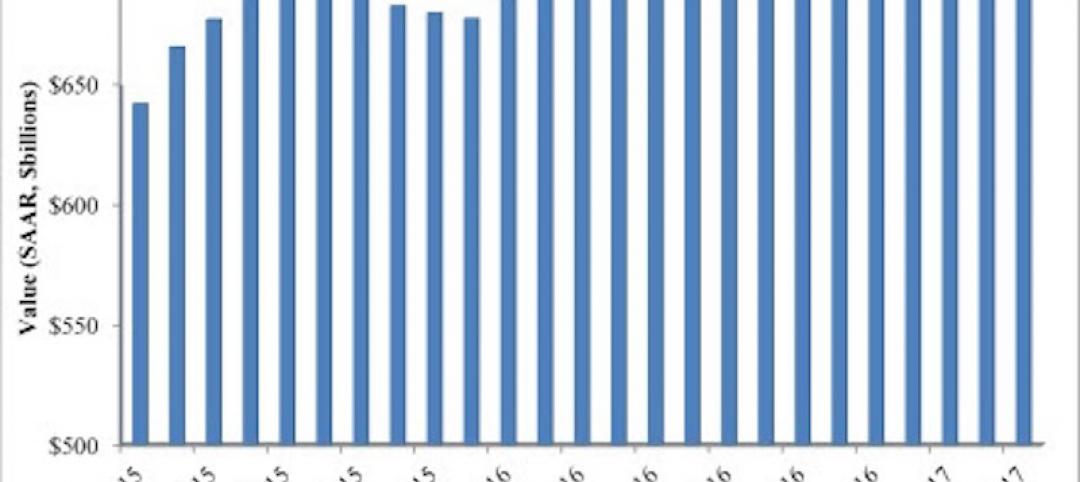

Nonresidential Spending loses steam after strong start to year

Spending in the segment totaled $708.6 billion on a seasonally adjusted, annualized basis.

Market Data | May 1, 2017

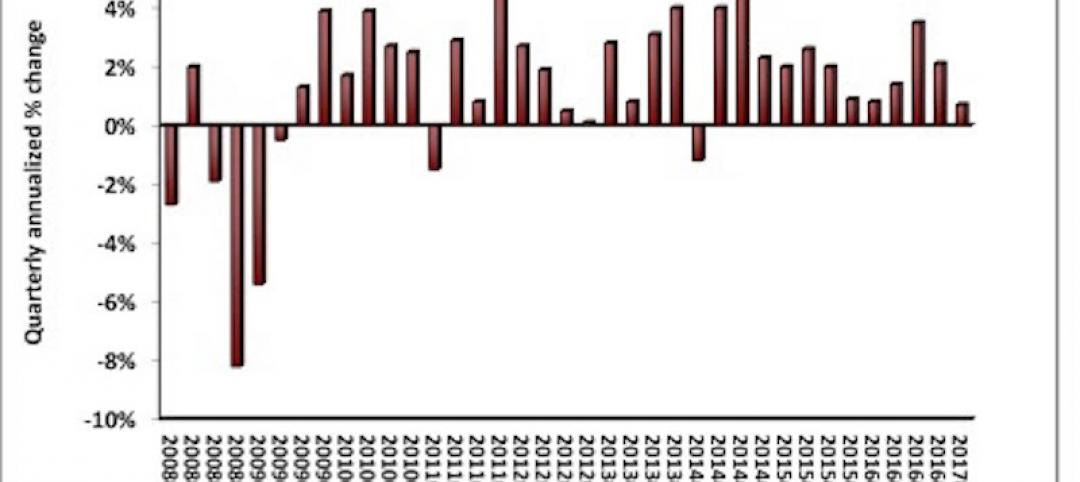

Nonresidential Fixed Investment surges despite sluggish economic in first quarter

Real gross domestic product (GDP) expanded 0.7 percent on a seasonally adjusted annualized rate during the first three months of the year.

Industry Research | Apr 28, 2017

A/E Industry lacks planning, but still spending large on hiring

The average 200-person A/E Firm is spending $200,000 on hiring, and not budgeting at all.

Architects | Apr 27, 2017

Number of U.S. architects holds steady, while professional mobility increases

New data from NCARB reveals that while the number of architects remains consistent, practitioners are looking to get licensed in multiple states.

Market Data | Apr 6, 2017

Architecture marketing: 5 tools to measure success

We’ve identified five architecture marketing tools that will help your firm evaluate if it’s on the track to more leads, higher growth, and broader brand visibility.

Market Data | Apr 3, 2017

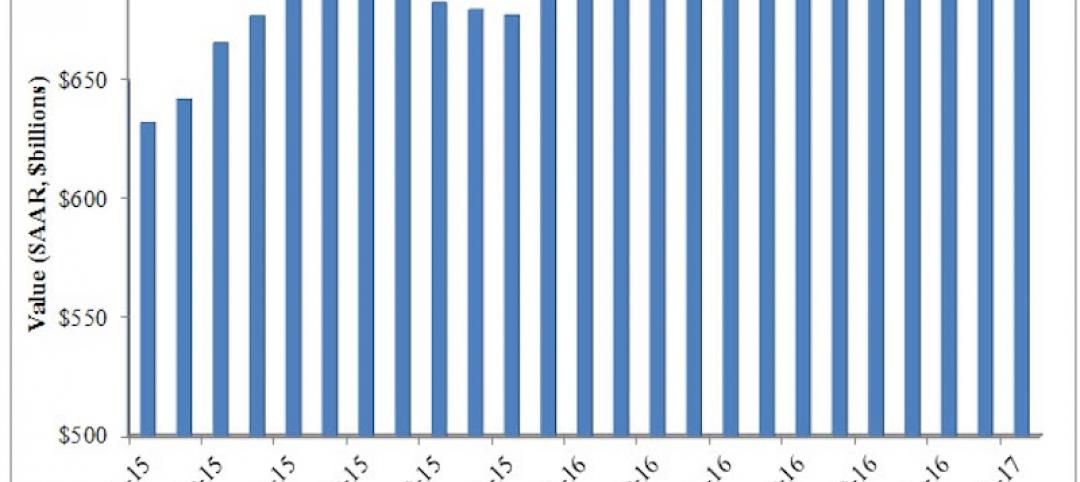

Public nonresidential construction spending rebounds; overall spending unchanged in February

The segment totaled $701.9 billion on a seasonally adjusted annualized rate for the month, marking the seventh consecutive month in which nonresidential spending sat above the $700 billion threshold.

Market Data | Mar 29, 2017

Contractor confidence ends 2016 down but still in positive territory

Although all three diffusion indices in the survey fell by more than five points they remain well above the threshold of 50, which signals that construction activity will continue to be one of the few significant drivers of economic growth.

Industry Research | Mar 24, 2017

The business costs and benefits of restroom maintenance

Businesses that have pleasant, well-maintained restrooms can turn into customer magnets.

Industry Research | Mar 22, 2017

Progress on addressing US infrastructure gap likely to be slow despite calls to action

Due to a lack of bipartisan agreement over funding mechanisms, as well as regulatory hurdles and practical constraints, Moody’s expects additional spending to be modest in 2017 and 2018.

Industry Research | Mar 21, 2017

Staff recruitment and retention is main concern among respondents of State of Senior Living 2017 survey

The survey asks respondents to share their expertise and insights on Baby Boomer expectations, healthcare reform, staff recruitment and retention, for-profit competitive growth, and the needs of middle-income residents.