Lodging Econometrics (LE) has released its bi-annual Global Construction Pipeline Trend Report, which compiles the construction pipeline counts for every country and market around the world, states that the total global construction pipeline stands at 12,839 projects/2,158,422 rooms which are at all-time highs. The construction pipeline is up an extraordinary 86% by projects over the cyclical low established in 2011 when global counts were at 6,907 projects/1,257,296 rooms.

There are 5,988 projects/1,133,017 rooms currently under construction worldwide. Projects scheduled to start construction in the next 12 months are at 3,945 projects/570,731 rooms, both counts are at record highs. Projects in the early planning stage stand at 2,906 rooms/454,674 projects, just 134 projects short of the record high established in the fourth quarter of 2017.

The top countries by project count are the United States, which has been rising since 2011, with 5,312 projects/634,501 rooms and China with 2,523 projects/556,645 rooms which has been topping out for the last 4.5 years. The U.S. accounts for 41% of projects in the total global construction pipeline while China accounts for 20%, resulting in 61% of projects in the global pipeline being concentrated in just these two countries. Distantly following are Indonesia with 394 projects/66,759 rooms, Germany with 247 projects/47,155 rooms, and the United Kingdom with 247 projects/36,487 rooms.

The cities with the largest pipeline counts are New York with 169 projects/29,365 rooms, Dubai with 163 projects/47,783 rooms, and Dallas with 156 projects/18,908 rooms. Followed by Houston with 150 projects/16,321 rooms, and Shanghai with 121 projects/24,759 rooms. Of the top 10 cities having pipelines with more than 100 projects, 6 are located in the U.S. while 3 are located in China.

The leading 5 franchise companies in the global construction pipeline by project count are Marriott International with 2,324 projects/391,058 rooms, Hilton Worldwide with 2,202 projects/327,723 rooms, InterContinental Hotels Group (IHG) with 1,653 projects/244,038 rooms, AccorHotels with 809 projects/147,647 rooms, and Choice Hotels with 1024 projects/84,350 rooms. Hyatt, at 212 rooms/45,117 projects, is also significant with their portfolio of large luxury and upper upscale projects as well Best Western with 275 projects/29,243 rooms which are concentrated in the middle three chain scales.

The twenty-five-year explosion of hotel brands now totals 610 globally. Marriott leads with 29 labels, followed by Accor with 25, Hilton with 15, IHG and Hyatt with 12 each, and Choice with 11.

Leading pipeline brands for each of these companies are Marriott’s Fairfield Inn with 345 projects/37,224 rooms, Hilton’s Hampton Inn with 604 projects/77,193 rooms, IHG’s Holiday Inn Express with 713 projects/88,689 rooms, AccorHotels ibis Brands with 358 projects/53,387 rooms, and Choice’s Comfort with 322 projects/26,878 rooms.

As a result of record pipeline totals, new hotel openings continue to hit record levels. In 2020, totals could reach a lofty 3,000 new hotel openings, approximately 1,250 of them being in the U.S.

Related Stories

Market Data | Apr 20, 2021

Demand for design services continues to rapidly escalate

AIA’s ABI score for March rose to 55.6 compared to 53.3 in February.

Market Data | Apr 16, 2021

Construction employment in March trails March 2020 mark in 35 states

Nonresidential projects lag despite hot homebuilding market.

Market Data | Apr 13, 2021

ABC’s Construction Backlog slips in March; Contractor optimism continues to improve

The Construction Backlog Indicator fell to 7.8 months in March.

Market Data | Apr 9, 2021

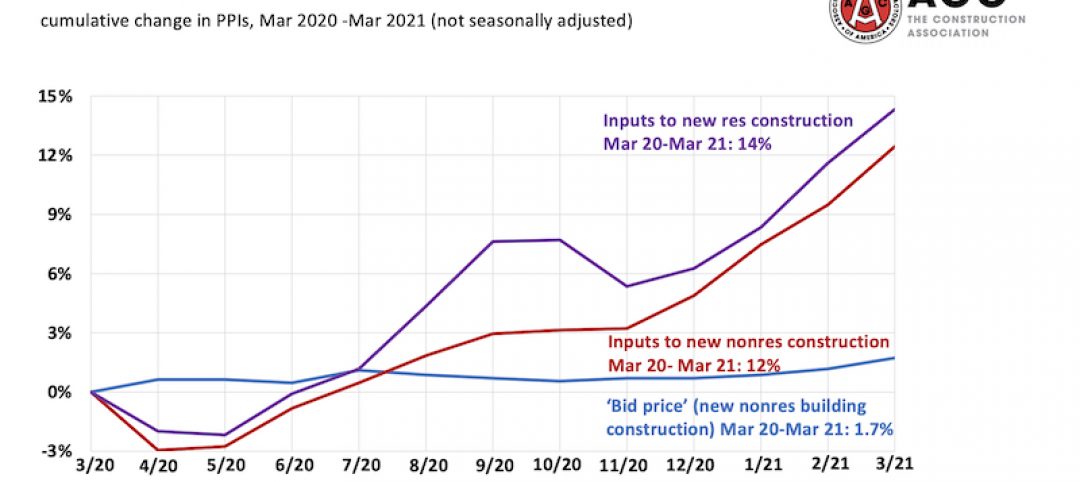

Record jump in materials prices and supply chain distributions threaten construction firms' ability to complete vital nonresidential projects

A government index that measures the selling price for goods used construction jumped 3.5% from February to March.

Contractors | Apr 9, 2021

Construction bidding activity ticks up in February

The Blue Book Network's Velocity Index measures month-to-month changes in bidding activity among construction firms across five building sectors and in all 50 states.

Industry Research | Apr 9, 2021

BD+C exclusive research: What building owners want from AEC firms

BD+C’s first-ever owners’ survey finds them focused on improving buildings’ performance for higher investment returns.

Market Data | Apr 7, 2021

Construction employment drops in 236 metro areas between February 2020 and February 2021

Houston-The Woodlands-Sugar Land and Odessa, Texas have worst 12-month employment losses.

Market Data | Apr 2, 2021

Nonresidential construction spending down 1.3% in February, says ABC

On a monthly basis, spending was down in 13 of 16 nonresidential subcategories.

Market Data | Apr 1, 2021

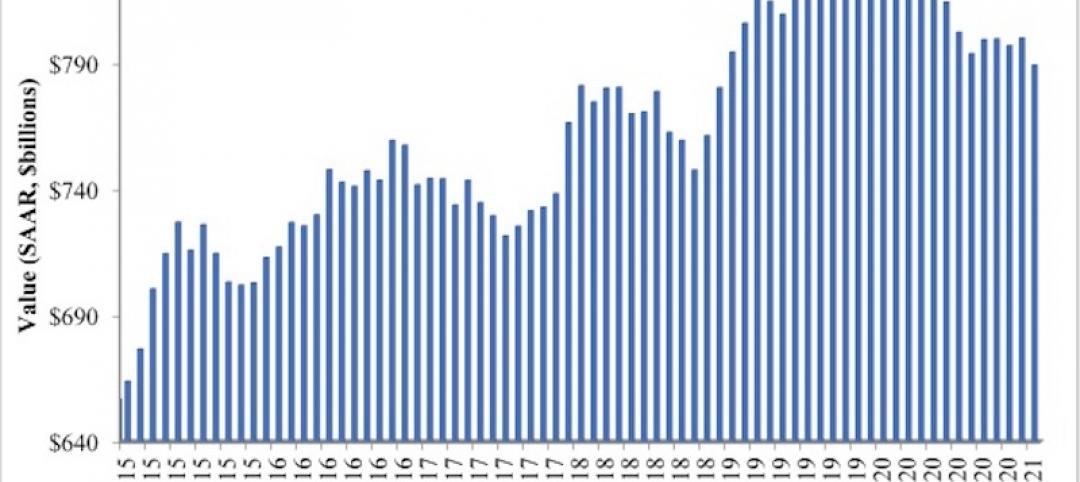

Construction spending slips in February

Shrinking demand, soaring costs, and supply delays threaten project completion dates and finances.

Market Data | Mar 26, 2021

Construction employment in February trails pre-pandemic level in 44 states

Soaring costs, supply-chain problems jeopardize future jobs.