From 2021 to 2023, the construction industry faced a tumultuous economic climate, marked by a confluence of challenging trends that have tested the resilience of industry executives. This period saw a significant surge in the demand for construction labor, primarily driven by an uptick in infrastructure project spending.

This rise in demand coincided with an increase in inflation, which exerted additional upward pressure on construction wages, culminating in a notable 20% nominal wage increase over the two years, as per a comprehensive January 2024 report by Gordian and ConstructConnect. Unfortunately, a major change in construction labor dynamics at the federal level is likely to compound this rising cost structure in 2024 and beyond.

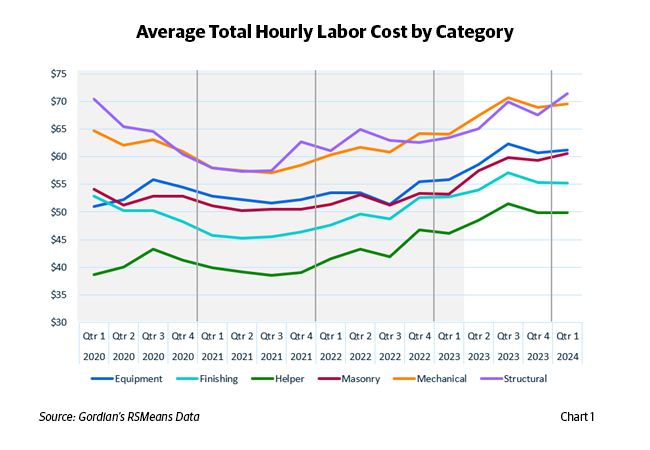

The tightening labor market within the construction sector has reached unprecedented levels. Demand for skilled workers has outpaced supply, creating a competitive environment where wages have soared to attract the necessary workforce. This dynamic has been further complicated by the highest sustained inflation in the U.S. economy since 1981, as indicated by the Consumer Price Index (CPI-U). The Infrastructure Investment and Jobs Act (IIJA) further amplified labor demand with its significant financial injection into public works and infrastructure projects. Construction wages increased to match both the surge in demand and general inflation, rising an average of 20% from 2021 to 2023. See Chart 1 for a detailed breakdown by category.

Chart 1: Average Wage Growth by Trade, 2021 to 2023

Federal Mandates Include the New Prevailing Wage Calculation

Looking ahead to 2024 and beyond, two pivotal changes in federal construction labor dynamics are likely to exacerbate the increasing cost structure. The first is the mandate of Project Labor Agreements (PLAs) for all federally funded projects exceeding $35 million in contract value, as decreed by an Executive Order in February 2022. PLAs are known to potentially inflate project labor costs by 12%-20%. Considering that approximately 40% of the $34 billion federal construction budget may be affected by PLAs, contractors are bracing for a widespread impact on labor costs.

The second significant change involves the Department of Labor's overhaul of the Davis-Bacon Act in 2023. This revision reinstated the "3-step process" for calculating prevailing wages, which had previously been a "2-step process" for over 40 years. Since 1983, prevailing wage has been calculated using only two steps:

- The wage rate paid to a majority of workers in the classification, or

- If no rate is paid to at least 50% of workers, then the weighted average rate in the classification.

By reinstating the 3-step process, the prevailing wage is calculated as follows:

- The wage rate paid to a majority of workers in the classification, or

- If no majority exists, the rate paid to 30% of workers, or

- If no rate paid to at least 30% of that classification’s workers, then the weighted average in the classification.

The overhaul also changed the mechanisms by which urban and rural wages are differentiated and updated between survey releases. With an estimated 1.2 million workers in the construction industry affected by these changes, the new calculation method is expected to elevate wages, particularly in regions with moderate-to-weak union presence, where collective bargaining agreements will now have greater influence in establishing prevailing wages. This change, coupled with more frequent updates to rural prevailing wage estimates, suggests that rural laborers' wages are also set to rise at a quicker pace than before.

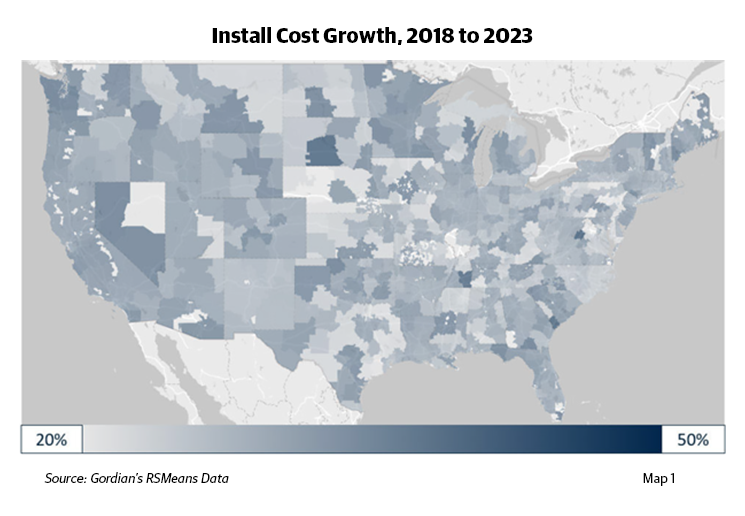

These legislative and economic adjustments have also led to emerging regional disparities in labor costs across the United States. Traditionally low-cost areas are witnessing a sharper incline in construction trade wages, a trend that has started to manifest itself with increasing clarity. See Map 1 below.

MAP 1: Install Cost Growth, 2018 to 2023

The situation presents a complex challenge for businesses within the construction industry. They are now tasked with managing the delicate balance of compensating their workforce adequately while grappling with reduced productivity per labor hour. The increased costs are not only felt in wages but also in the broader economic impact, including the prices of materials and the overall cost of construction projects.

Mitigating the Impact of Federal Mandates

As companies strategize to navigate this new landscape, they are exploring various approaches to mitigate the impact of these changes. Some are investing in technology and automation to improve efficiency and reduce their reliance on an increasingly expensive labor force. Others are reevaluating their project management strategies, seeking ways to streamline operations and optimize the use of available labor.

Moreover, the industry is placing a greater emphasis on training and development, aiming to upskill the existing workforce to meet the evolving demands of modern construction projects. By enhancing the skill set of their workers, companies hope to increase productivity and offset some of the rising labor costs.

In addition to internal strategies, there is also a push for policy advocacy. Industry leaders are engaging with policymakers to discuss the implications of the recent changes and to explore potential measures that could ease the burden on the construction sector. These discussions are crucial in shaping a regulatory environment that supports the sustainable growth of the industry while ensuring fair compensation for its workforce.

As the construction industry continues to adapt to these economic pressures, the importance of strategic planning and proactive management has never been more critical. Companies that successfully navigate this "perfect storm" will be those that are agile, innovative and forward-thinking in their approach to labor management and cost control. With the right strategies in place, the industry can continue to thrive despite the challenges, building a robust future for both its businesses and its workforce.

About the Author

Samuel Giffin (s.giffin@gordian.com), Director of Data Operations at Gordian, is responsible for leading and developing engineering, research and professional services teams in providing data to power Gordian's construction estimating and procurement solutions.

Related Stories

Healthcare Facilities | Apr 13, 2023

Healthcare construction costs for 2023

Data from Gordian breaks down the average cost per square foot for a three-story hospital across 10 U.S. cities.

Higher Education | Apr 13, 2023

Higher education construction costs for 2023

Fresh data from Gordian breaks down the average cost per square foot for a two-story college classroom building across 10 U.S. cities.

Market Data | Apr 13, 2023

Construction input prices down year-over-year for first time since August 2020

Construction input prices increased 0.2% in March, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics Producer Price Index data released today. Nonresidential construction input prices rose 0.4% for the month.

Market Data | Apr 6, 2023

JLL’s 2023 Construction Outlook foresees growth tempered by cost increases

The easing of supply chain snags for some product categories, and the dispensing with global COVID measures, have returned the North American construction sector to a sense of normal. However, that return is proving to be complicated, with the construction industry remaining exceptionally busy at a time when labor and materials cost inflation continues to put pricing pressure on projects, leading to caution in anticipation of a possible downturn. That’s the prognosis of JLL’s just-released 2023 U.S. and Canada Construction Outlook.

| Sep 8, 2022

U.S. construction costs expected to rise 14% year over year by close of 2022

Coldwell Banker Richard Ellis (CBRE) is forecasting a 14.1% year-on-year increase in U.S. construction costs by the close of 2022.

Market Data | Oct 11, 2021

No decline in construction costs in sight

Construction cost gains are occurring at a time when nonresidential construction spending was down by 9.5 percent for the 12 months through July 2021.