Nonresidential construction activity should remain strong in the U.S. through 2016, although labor shortages and the rising cost of sheet glass will make projects more expensive, according to JLL’s latest Construction Outlook.

JLL sees the South as the country’s “new frontier” for construction, thanks to the region’s low labor and land costs. Conversely, the erosion in oil prices is cramping building in places like Houston whose economics rely heavily on their energy industries.

Sustainable office development pushed renovation activity to new heights in 2015. “This push for new build-outs was not limited to office spaces, with retail and industrial developers redeveloping existing space to include new technology and engage consumers in unique ways,” JLL’s 34-page report states, adding that this trend should continue this year.

The report sees positive signs in construction employment, which outpaced the country’s 4% growth rate. JLL also surveyed development firms that, in the main, agree that construction activity should be steady at least through the second half of 2016, and possibly well beyond that.

Building materials costs, which had increased incrementally since 2010, appear to have plateaued last year. The steel market was flooded by low-cost product, for example. The one notable exception was sheet glass, whose prices have skyrocketed, leading, some construction companies to acquire glass makers to stabilize their costs.

While materials costs are always a concern, JLL notes that labor costs—wages and benefits—have spiked, particularly for skilled workers. Average weekly wages for construction workers rose in December 2015 by 4.2% compared to the same month a year earlier. Massachusetts, New York, and Washington D.C. have the highest weekly construction wages; Georgia, Missouri, and Colorado the lowest.

Industrial sector a ‘shining star’

JLL estimates the value of construction put in place rose 10.2% last year through November, with the Education (up 12% in construction activity) and Manufacturing sectors driving the train. But all of the top construction markets also saw at least a 1% increase in construction costs from the second to the fourth quarter of last year.

“For financial viability, project sponsors will need to strike a balance between the lower costs for some materials, like steel, and the ever-increasing cost of glass and labor,” says Todd Burns, President, Project and Development Services, JLL Americas. “Location continues to be a key driver in finding success throughout various industry sectors. With a slowed growth in construction, executives need to think strategically in terms of where they will invest.”

The researcher sees parallels between construction costs and rents. It points specifically to the San Francisco Bay Area, where construction and office leasing are among the highest in the country.

Nationwide, office deliveries outpaced starts for the first time since the recession, in terms of total square footage, and approached pre-recession numbers. Office completions in every quarter last year were higher than corresponding quarters in 2014. And with the exception of Houston, where office construction was off nearly 42% last year, office construction activity was steady in most top markets.

As of the fourth quarter of last year, there were 88.5 million sf of office space under construction, nearly 9% more than in fourth-quarter 2014. The quarter-to-quarter gains in industrial construction were even more pronounced during this period: 23%. (JLL refers to the industrial sector as nonresidential construction’s “shining star,” and estimates that 178.4 million sf of industrial space were delivered last year.)

Dallas (with 19.7 million sf of industrial space under construction as of the fourth quarter) and Atlanta (19.6 million sf) eclipsed California’s Inland Empire as this sector’s leading markets.

JLL’s take on Retail construction is that while it was off slightly last year, it still showed fourth-quarter gains in all major markets. (Ironically, Houston was the leader, with 2.9 million sf under construction in the fourth quarter, followed by New York City, with 2.7 million.) Retail vacancies across the country declined as the economy improved.

“We have never seen a greater sense of urgency from retailers to address their stores’ role in delivering a ‘True Omni Branded Experience’ for consumers,” says Aaron Spiess, Executive Vice President, Managing Director, Project and Development Services, JLL Americas. “The pressure of emerging digital experiences and platforms has escalated the need to exceed consumer expectations of the store. With the continuous advent of new e-commerce capabilities, this is a trend we expect to continue.”

The 2016 general election looms large in JLL’s forecast. “The upcoming fight over the debt ceiling could delay government buildings and other public works,” its report states. JLL also notes that a slowing global economy could have a silver lining by causing material prices to fall further.

But don’t expect wage costs to taper off any time soon, it predicts. “There remains a dearth of trained construction employees, especially in trade positions, and wages are rising as a result.”

In its final analysis, JLL foresees construction starts will increase at a slower rate than last year, but ahead of the overall economy. “Demand from downstream markets such as Austin, Chicago, Atlanta, and Charlotte will bolster the industry, and construction profit margins will continue to rise, keeping construction growing at a faster rate than the overall economy.”

Related Stories

Market Data | Sep 3, 2019

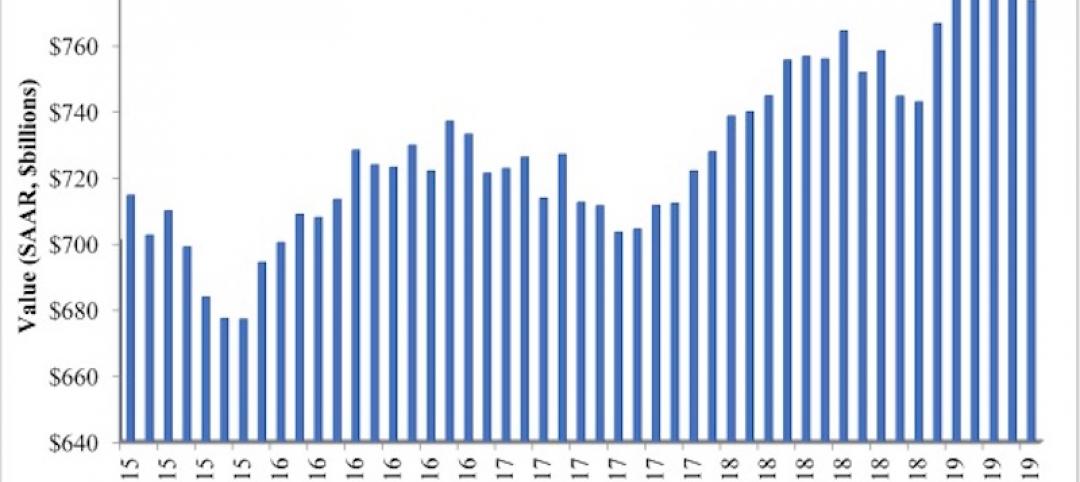

Nonresidential construction spending slips in July 2019, but still surpasses $776 billion

Construction spending declined 0.3% in July, totaling $776 billion on a seasonally adjusted annualized basis.

Industry Research | Aug 29, 2019

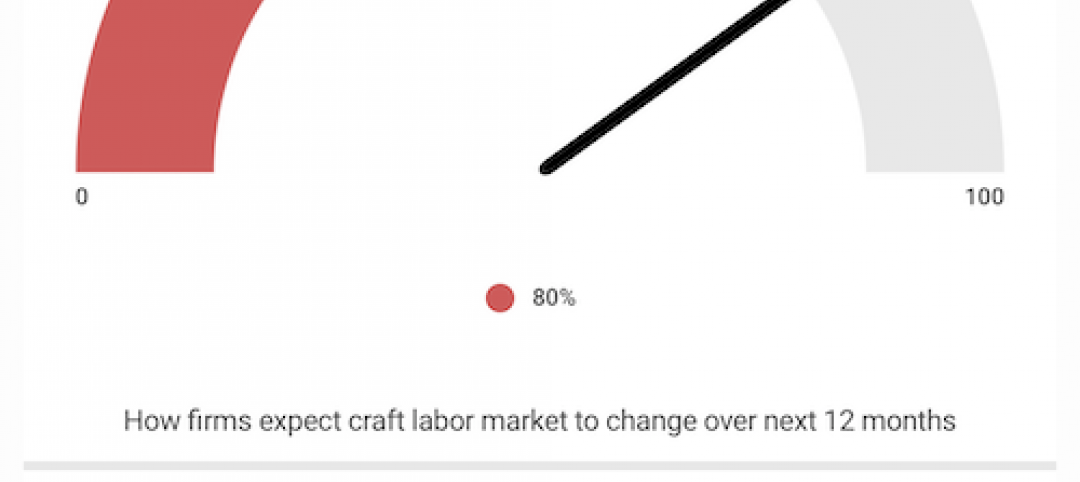

Construction firms expect labor shortages to worsen over the next year

A new AGC-Autodesk survey finds more companies turning to technology to support their jobsites.

Market Data | Aug 21, 2019

Architecture Billings Index continues its streak of soft readings

Decline in new design contracts suggests volatility in design activity to persist.

Market Data | Aug 19, 2019

Multifamily market sustains positive cycle

Year-over-year growth tops 3% for 13th month. Will the economy stifle momentum?

Market Data | Aug 16, 2019

Students say unclean restrooms impact their perception of the school

The findings are part of Bradley Corporation’s Healthy Hand Washing Survey.

Market Data | Aug 12, 2019

Mid-year economic outlook for nonresidential construction: Expansion continues, but vulnerabilities pile up

Emerging weakness in business investment has been hinting at softening outlays.

Market Data | Aug 7, 2019

National office vacancy holds steady at 9.7% in slowing but disciplined market

Average asking rental rate posts 4.2% annual growth.

Market Data | Aug 1, 2019

Nonresidential construction spending slows in June, remains elevated

Among the 16 nonresidential construction spending categories tracked by the Census Bureau, seven experienced increases in monthly spending.

Market Data | Jul 31, 2019

For the second quarter of 2019, the U.S. hotel construction pipeline continued its year-over-year growth spurt

The growth spurt continued even as business investment declined for the first time since 2016.

Market Data | Jul 23, 2019

Despite signals of impending declines, continued growth in nonresidential construction is expected through 2020

AIA’s latest Consensus Construction Forecast predicts growth.