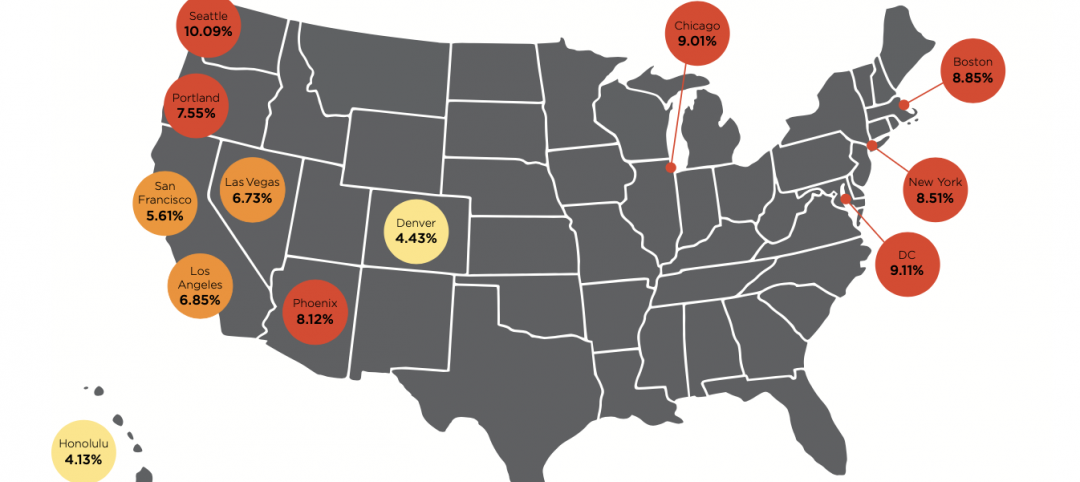

Leopardo Companies, a construction firm serving Chicago and the Midwest, has released its 2017 Construction Economics Report and Outlook, an in-depth analysis of factors that impact development, renovation and build-out costs in commercial facilities, including the office, industrial/manufacturing, retail, multifamily, healthcare and lodging sectors.

Nationally, year-over- year construction spending increased by 4.2 percent in December 2016, as total volume reached an estimated $1.182 trillion. The pace of growth, however, was less than in 2015, when volume increased by 8.7 percent. The slowdown in growth was due to firms pulling back on capital expenditures and speculative development amid concerns about the global economy, political uncertainty, volatility in energy prices, rising construction labor costs and a cautious environment for construction financing.

Chicago and suburban areas experienced construction gains in the office, industrial, healthcare and multifamily sectors, while volume was flat in the retail and homebuilding sectors. The Chicagoland market also saw a 1.4 percent drop in construction employment, compared to a national average increase of 2.2 percent. The loss of construction jobs exacerbates the challenge of rising labor costs in the sector, which will continue into 2017 and beyond.

“We expect to see the construction market resume its healthy pace of growth this year, after a slight slowdown in the second half of 2016 due in part to the uncertainty of the presidential election,” said Leopardo Vice President Mark Yanik. “Although it’s too soon to know the impact of the Trump administration on demand for commercial real estate, some early signs are potentially favorable to our industry, such as plans to withdraw from the Trans-Pacific Partnership, renegotiate the North American Free Trade Agreement, and ease banking regulations.”

Key findings in the report include:

Office construction spending grew 20.9 percent during 2016, driven by growth of the technology sector. Office space will continue to be in high demand in cities like Chicago that are well-suited to millennials’ desire for live-work- play neighborhoods. However, companies that are concerned about high labor cost are increasingly interested in lower-cost markets like Salt Lake City, Denver and San Antonio.

Construction spending in the U.S. manufacturing sector contracted 4.3 percent in 2016 after a record-setting 33.3 percent growth rate in 2015. In the Chicago area, however, industrial/manufacturing construction reached an all-time high last year, as record levels of net absorption reduced occupancies and increased rental rates across the region.

U.S. healthcare construction spending grew 1.7 percent to $41.4 billion by the end of 2016, down 5.4 percent from the previous year. Rising healthcare costs have prompted a shift from hospitals to outpatient facilities, driving demand for medical office buildings and helping to backfill vacancies in retail strip centers. This trend extends to the Chicago area, where new regional clinics are under way to be closer to patient populations.

Download the full 2017 Construction Economics Report and Outlook for free.

Related Stories

Market Data | Jan 31, 2022

Canada's hotel construction pipeline ends 2021 with 262 projects and 35,325 rooms

At the close of 2021, projects under construction stand at 62 projects/8,100 rooms.

Market Data | Jan 27, 2022

Record high counts for franchise companies in the early planning stage at the end of Q4'21

Through year-end 2021, Marriott, Hilton, and IHG branded hotels represented 585 new hotel openings with 73,415 rooms.

Market Data | Jan 27, 2022

Dallas leads as the top market by project count in the U.S. hotel construction pipeline at year-end 2021

The market with the greatest number of projects already in the ground, at the end of the fourth quarter, is New York with 90 projects/14,513 rooms.

Market Data | Jan 26, 2022

2022 construction forecast: Healthcare, retail, industrial sectors to lead ‘healthy rebound’ for nonresidential construction

A panel of construction industry economists forecasts 5.4 percent growth for the nonresidential building sector in 2022, and a 6.1 percent bump in 2023.

Market Data | Jan 24, 2022

U.S. hotel construction pipeline stands at 4,814 projects/581,953 rooms at year-end 2021

Projects scheduled to start construction in the next 12 months stand at 1,821 projects/210,890 rooms at the end of the fourth quarter.

Market Data | Jan 19, 2022

Architecture firms end 2021 on a strong note

December’s Architectural Billings Index (ABI) score of 52.0 was an increase from 51.0 in November.

Market Data | Jan 13, 2022

Materials prices soar 20% in 2021 despite moderating in December

Most contractors in association survey list costs as top concern in 2022.

Market Data | Jan 12, 2022

Construction firms forsee growing demand for most types of projects

Seventy-four percent of firms plan to hire in 2022 despite supply-chain and labor challenges.

Market Data | Jan 7, 2022

Construction adds 22,000 jobs in December

Jobless rate falls to 5% as ongoing nonresidential recovery offsets rare dip in residential total.

Market Data | Jan 6, 2022

Inflation tempers optimism about construction in North America

Rider Levett Bucknall’s latest report cites labor shortages and supply chain snags among causes for cost increases.