Leopardo Companies, a construction firm serving Chicago and the Midwest, has released its 2017 Construction Economics Report and Outlook, an in-depth analysis of factors that impact development, renovation and build-out costs in commercial facilities, including the office, industrial/manufacturing, retail, multifamily, healthcare and lodging sectors.

Nationally, year-over- year construction spending increased by 4.2 percent in December 2016, as total volume reached an estimated $1.182 trillion. The pace of growth, however, was less than in 2015, when volume increased by 8.7 percent. The slowdown in growth was due to firms pulling back on capital expenditures and speculative development amid concerns about the global economy, political uncertainty, volatility in energy prices, rising construction labor costs and a cautious environment for construction financing.

Chicago and suburban areas experienced construction gains in the office, industrial, healthcare and multifamily sectors, while volume was flat in the retail and homebuilding sectors. The Chicagoland market also saw a 1.4 percent drop in construction employment, compared to a national average increase of 2.2 percent. The loss of construction jobs exacerbates the challenge of rising labor costs in the sector, which will continue into 2017 and beyond.

“We expect to see the construction market resume its healthy pace of growth this year, after a slight slowdown in the second half of 2016 due in part to the uncertainty of the presidential election,” said Leopardo Vice President Mark Yanik. “Although it’s too soon to know the impact of the Trump administration on demand for commercial real estate, some early signs are potentially favorable to our industry, such as plans to withdraw from the Trans-Pacific Partnership, renegotiate the North American Free Trade Agreement, and ease banking regulations.”

Key findings in the report include:

Office construction spending grew 20.9 percent during 2016, driven by growth of the technology sector. Office space will continue to be in high demand in cities like Chicago that are well-suited to millennials’ desire for live-work- play neighborhoods. However, companies that are concerned about high labor cost are increasingly interested in lower-cost markets like Salt Lake City, Denver and San Antonio.

Construction spending in the U.S. manufacturing sector contracted 4.3 percent in 2016 after a record-setting 33.3 percent growth rate in 2015. In the Chicago area, however, industrial/manufacturing construction reached an all-time high last year, as record levels of net absorption reduced occupancies and increased rental rates across the region.

U.S. healthcare construction spending grew 1.7 percent to $41.4 billion by the end of 2016, down 5.4 percent from the previous year. Rising healthcare costs have prompted a shift from hospitals to outpatient facilities, driving demand for medical office buildings and helping to backfill vacancies in retail strip centers. This trend extends to the Chicago area, where new regional clinics are under way to be closer to patient populations.

Download the full 2017 Construction Economics Report and Outlook for free.

Related Stories

Market Data | Aug 12, 2021

Steep rise in producer prices for construction materials and services continues in July.

The producer price index for new nonresidential construction rose 4.4% over the past 12 months.

Market Data | Aug 6, 2021

Construction industry adds 11,000 jobs in July

Nonresidential sector trails overall recovery.

Market Data | Aug 2, 2021

Nonresidential construction spending falls again in June

The fall was driven by a big drop in funding for highway and street construction and other public work.

Market Data | Jul 29, 2021

Outlook for construction spending improves with the upturn in the economy

The strongest design sector performers for the remainder of this year are expected to be health care facilities.

Market Data | Jul 29, 2021

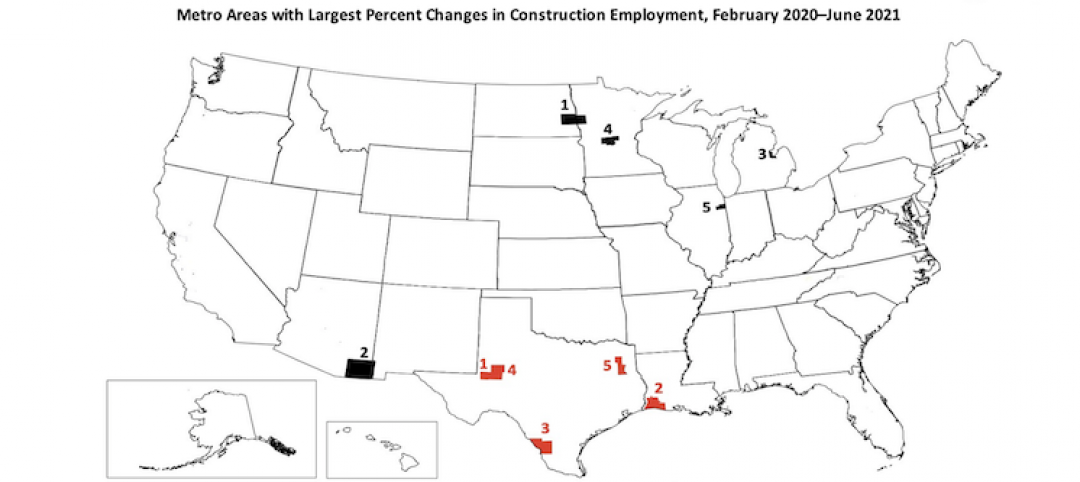

Construction employment lags or matches pre-pandemic level in 101 metro areas despite housing boom

Eighty metro areas had lower construction employment in June 2021 than February 2020.

Market Data | Jul 28, 2021

Marriott has the largest construction pipeline of U.S. franchise companies in Q2‘21

472 new hotels with 59,034 rooms opened across the United States during the first half of 2021.

Market Data | Jul 27, 2021

New York leads the U.S. hotel construction pipeline at the close of Q2‘21

Many hotel owners, developers, and management groups have used the operational downtime, caused by COVID-19’s impact on operating performance, as an opportunity to upgrade and renovate their hotels and/or redefine their hotels with a brand conversion.

Market Data | Jul 26, 2021

U.S. construction pipeline continues along the road to recovery

During the first and second quarters of 2021, the U.S. opened 472 new hotels with 59,034 rooms.

Market Data | Jul 21, 2021

Architecture Billings Index robust growth continues

AIA’s Architecture Billings Index (ABI) score for June remained at an elevated level of 57.1.

Market Data | Jul 20, 2021

Multifamily proposal activity maintains sizzling pace in Q2

Condos hit record high as all multifamily properties benefit from recovery.