Leopardo Companies, a construction firm serving Chicago and the Midwest, has released its 2017 Construction Economics Report and Outlook, an in-depth analysis of factors that impact development, renovation and build-out costs in commercial facilities, including the office, industrial/manufacturing, retail, multifamily, healthcare and lodging sectors.

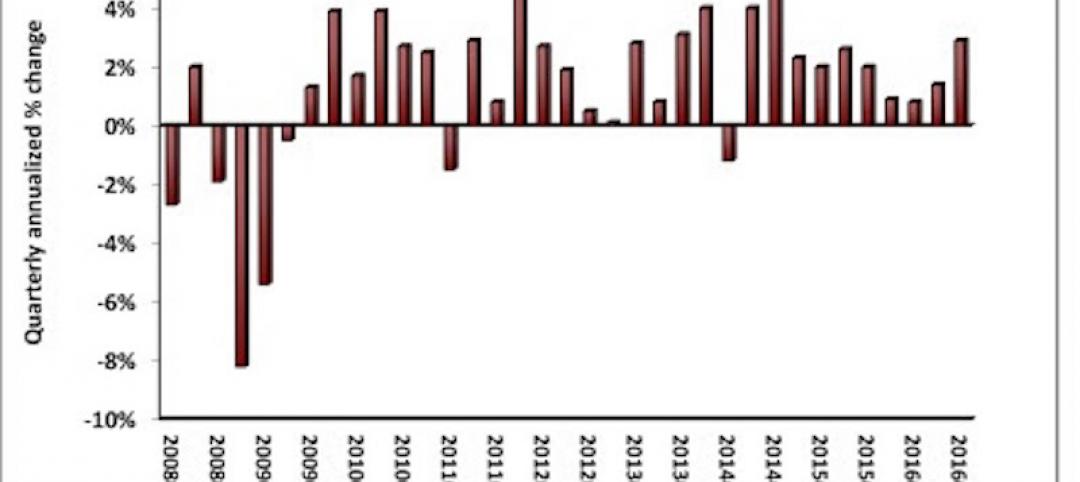

Nationally, year-over- year construction spending increased by 4.2 percent in December 2016, as total volume reached an estimated $1.182 trillion. The pace of growth, however, was less than in 2015, when volume increased by 8.7 percent. The slowdown in growth was due to firms pulling back on capital expenditures and speculative development amid concerns about the global economy, political uncertainty, volatility in energy prices, rising construction labor costs and a cautious environment for construction financing.

Chicago and suburban areas experienced construction gains in the office, industrial, healthcare and multifamily sectors, while volume was flat in the retail and homebuilding sectors. The Chicagoland market also saw a 1.4 percent drop in construction employment, compared to a national average increase of 2.2 percent. The loss of construction jobs exacerbates the challenge of rising labor costs in the sector, which will continue into 2017 and beyond.

“We expect to see the construction market resume its healthy pace of growth this year, after a slight slowdown in the second half of 2016 due in part to the uncertainty of the presidential election,” said Leopardo Vice President Mark Yanik. “Although it’s too soon to know the impact of the Trump administration on demand for commercial real estate, some early signs are potentially favorable to our industry, such as plans to withdraw from the Trans-Pacific Partnership, renegotiate the North American Free Trade Agreement, and ease banking regulations.”

Key findings in the report include:

Office construction spending grew 20.9 percent during 2016, driven by growth of the technology sector. Office space will continue to be in high demand in cities like Chicago that are well-suited to millennials’ desire for live-work- play neighborhoods. However, companies that are concerned about high labor cost are increasingly interested in lower-cost markets like Salt Lake City, Denver and San Antonio.

Construction spending in the U.S. manufacturing sector contracted 4.3 percent in 2016 after a record-setting 33.3 percent growth rate in 2015. In the Chicago area, however, industrial/manufacturing construction reached an all-time high last year, as record levels of net absorption reduced occupancies and increased rental rates across the region.

U.S. healthcare construction spending grew 1.7 percent to $41.4 billion by the end of 2016, down 5.4 percent from the previous year. Rising healthcare costs have prompted a shift from hospitals to outpatient facilities, driving demand for medical office buildings and helping to backfill vacancies in retail strip centers. This trend extends to the Chicago area, where new regional clinics are under way to be closer to patient populations.

Download the full 2017 Construction Economics Report and Outlook for free.

Related Stories

Market Data | Oct 31, 2016

Nonresidential fixed investment expands again during solid third quarter

The acceleration in real GDP growth was driven by a combination of factors, including an upturn in exports, a smaller decrease in state and local government spending and an upturn in federal government spending, says ABC Chief Economist Anirban Basu.

Market Data | Oct 28, 2016

U.S. construction solid and stable in Q3 of 2016; Presidential election seen as influence on industry for 2017

Rider Levett Bucknall’s Third Quarter 2016 USA Construction Cost Report puts the complete spectrum of construction sectors and markets in perspective as it assesses the current state of the industry.

Industry Research | Oct 25, 2016

New HOK/CoreNet Global report explores impact of coworking on corporate real rstate

“Although coworking space makes up less than one percent of the world’s office space, it represents an important workforce trend and highlights the strong desire of today’s employees to have workplace choices, community and flexibility,” says Kay Sargent, Director of WorkPlace at HOK.

Market Data | Oct 24, 2016

New construction starts in 2017 to increase 5% to $713 billion

Dodge Outlook Report predicts moderate growth for most project types – single family housing, commercial and institutional building, and public works, while multifamily housing levels off and electric utilities/gas plants decline.

High-rise Construction | Oct 21, 2016

The world’s 100 tallest buildings: Which architects have designed the most?

Two firms stand well above the others when it comes to the number of tall buildings they have designed.

Market Data | Oct 19, 2016

Architecture Billings Index slips consecutive months for first time since 2012

“This recent backslide should act as a warning signal,” said AIA Chief Economist, Kermit Baker.

Market Data | Oct 11, 2016

Building design revenue topped $28 billion in 2015

Growing profitability at architecture firms has led to reinvestment and expansion

Market Data | Oct 4, 2016

Nonresidential spending slips in August

Public sector spending is declining faster than the private sector.

Industry Research | Oct 3, 2016

Structure Tone survey shows cost is still a major barrier to building green

Climate change, resilience and wellness are also growing concerns.

Industry Research | Sep 27, 2016

Sterling Risk Sentiment Index indicates risk exposure perception remains stable in construction industry

Nearly half (45%) of those polled say election year uncertainty has a negative effect on risk perception in the construction market.