In the second quarter of 2021, analysts at Lodging Econometrics (LE) report that the top franchise companies with the largest construction pipelines are: Marriott International with 1,301 projects/170,847 rooms, Hilton Worldwide with 1,216 projects/139,172 rooms, and InterContinental Hotels Group (IHG) with 777 projects/78,929 rooms. Development projects with these three franchise companies comprise 69% of all projects in the total construction pipeline.

The largest brands for each of these companies are Marriott’s Fairfield Inn with 257 projects/25,051 rooms, Hilton’s Home2 Suites by Hilton, with 379 projects/39,584 rooms and IHG’s Holiday Inn Express with 303 projects/29,055 rooms. These three brands make up 20% of the total construction pipeline rooms in the U.S.

Other high-volume brands in the pipeline for each of these franchises are Marriott’s TownePlace Suites with 198 projects/19,422 rooms and Residence Inn with 189 projects/23,493 rooms; Hilton’s Hampton by Hilton with 269 projects/28,071 rooms and Tru by Hilton with 235 projects/22,521 rooms; and IHG’s Avid Hotel with 157 projects/13,842 rooms and Staybridge Suites with 122 projects/12,607 rooms.

In the second quarter of 2021, LE recorded 583 conversion projects/63,807 rooms. Of these conversion totals, Best Western leads with 116 conversion projects/10,289 rooms, accounting for 20% of the conversion pipeline by projects. Following Best Western is Choice Hotels, Marriott International, and Hilton Worldwide. Best Western and these three franchise companies combined account for 61% of all the rooms in the conversion pipeline across the United States.

472 new hotels with 59,034 rooms opened across the United States during the first half of 2021. Marriott, Hilton, and IHG collectively opened 74% of the hotels. Marriott opened 152 hotels with 20,416 rooms, Hilton opened 125 hotels/16,970 rooms, and IHG opened 72 hotels/7,249 rooms.

Related Stories

Market Data | Jun 22, 2018

Multifamily market remains healthy – Can it be sustained?

New report says strong economic fundamentals outweigh headwinds.

Market Data | Jun 21, 2018

Architecture firm billings strengthen in May

Architecture Billings Index enters eighth straight month of solid growth.

Market Data | Jun 20, 2018

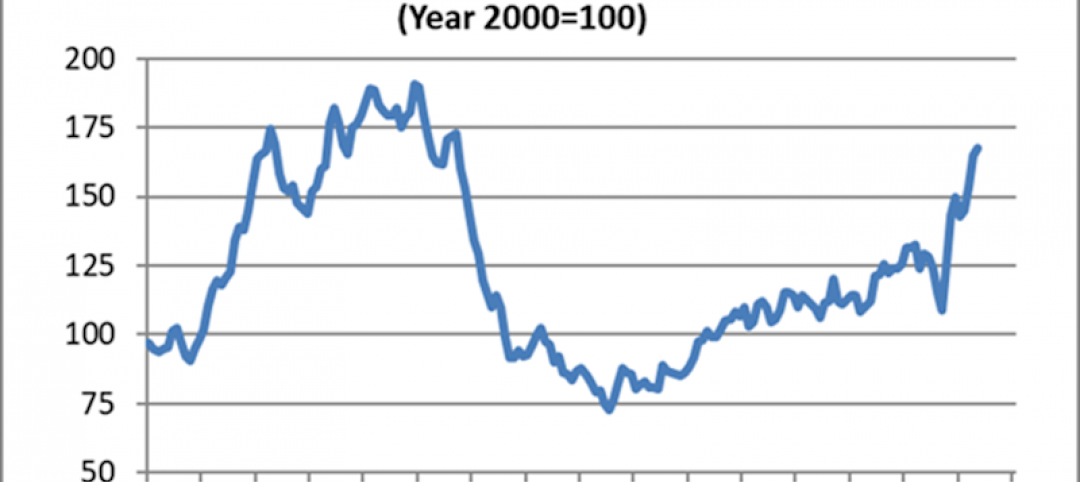

7% year-over-year growth in the global construction pipeline

There are 5,952 projects/1,115,288 rooms under construction, up 8% by projects YOY.

Market Data | Jun 19, 2018

ABC’s Construction Backlog Indicator remains elevated in first quarter of 2018

The CBI shows highlights by region, industry, and company size.

Market Data | Jun 19, 2018

America’s housing market still falls short of providing affordable shelter to many

The latest report from the Joint Center for Housing Studies laments the paucity of subsidies to relieve cost burdens of ownership and renting.

Market Data | Jun 18, 2018

AI is the path to maximum profitability for retail and FMCG firms

Leading retailers including Amazon, Alibaba, Lowe’s and Tesco are developing their own AI solutions for automation, analytics and robotics use cases.

Market Data | Jun 12, 2018

Yardi Matrix report details industrial sector's strength

E-commerce and biopharmaceutical companies seeking space stoke record performances across key indicators.

Market Data | Jun 8, 2018

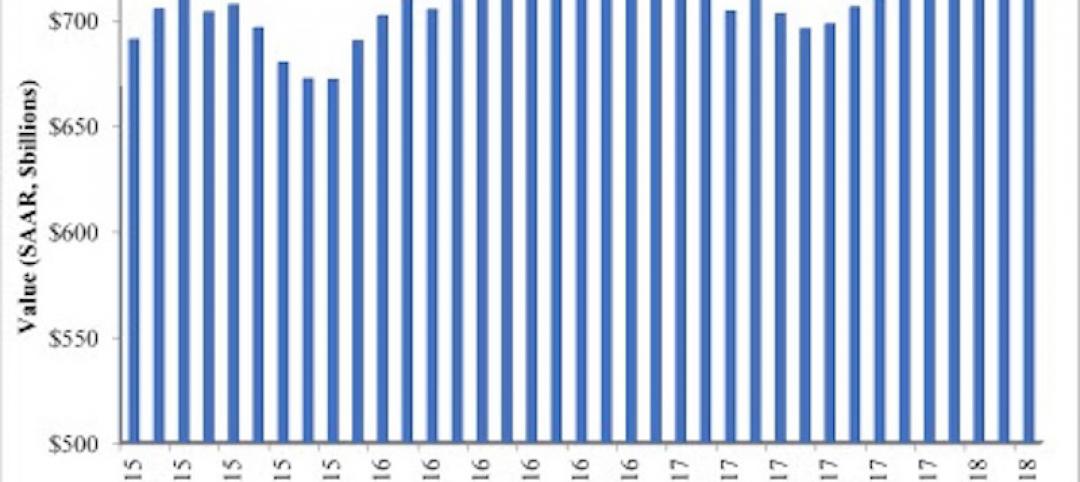

Dodge Momentum Index inches up in May

May’s gain was the result of a 4.7% increase by the commercial component of the Momentum Index.

Market Data | Jun 4, 2018

Nonresidential construction remains unchanged in April

Private sector spending increased 0.8% on a monthly basis and is up 5.3% from a year ago.

Market Data | May 30, 2018

Construction employment increases in 256 metro areas between April 2017 & 2018

Dallas-Plano-Irving and Midland, Texas experience largest year-over-year gains; St. Louis, Mo.-Ill. and Bloomington, Ill. have biggest annual declines in construction employment amid continuing demand.