Dodge Data & Analytics today released its 2017 Dodge Construction Outlook. The report predicts that total U.S. construction starts for 2017 will advance 5% to $713 billion, following gains of 11% in 2015 and an estimated 1% in 2016.

“The U.S. construction industry has witnessed signs of deceleration in 2016, following several years of steady growth,” says Robert Murray, chief economist for Dodge Data & Analytics. “Total construction starts during the first half of this year lagged behind what was reported in 2015, raising some concern that the current construction expansion may have run its course. However, the early 2016 shortfall reflected the comparison to unusually elevated activity during the first half of 2015, lifted by 13 very large projects valued each at $1 billion or more, such as a $9 billion liquefied natural gas export terminal in Texas and a $2.5 billion office tower in New York City. As 2016 has proceeded, the year-to-date shortfall has grown smaller, easing concern that the construction industry may be in the early stage of cyclical decline. Instead, the construction industry has now entered a more mature phase of its expansion, one that is characterized by slower rates of growth than what took place during the 2012-2015 period, but still growth. Since the construction start statistics will lead the pattern of construction spending, this means that construction spending can be expected to see moderate gains through 2017 and beyond.

“On balance, there are a number of positive factors which suggest the construction expansion has room to proceed. The U.S. economy in 2017 is anticipated to see moderate job growth, market fundamentals for commercial real estate should remain generally healthy, and more funding support is coming from state and local bond measures. Although the global economy in 2017 will remain sluggish, energy prices appear to have stabilized, interest rate hikes will be gradual and few, and a new U.S. President will have been elected. For 2017, total construction starts are forecast to rise 5% to $713 billion. Gains of 8% are expected for both residential building and nonresidential building, while nonbuilding construction slides a further 3%.”

The pattern of construction starts by more specific sectors is the following:

- Single family housing will rise 12% in dollars, corresponding to a 9% increase in units to 795,000 (Dodge basis). Access to home mortgage loans is improving, and some of the caution exercised by potential homebuyers will ease with continued employment growth and low mortgage rates. Older members of the Millennial generation are now moving into the 30 to 35 year-old age bracket, which should begin to lift demand for single family housing.

- Multifamily housing will be flat in dollars and down 2% in units to 435,000 (Dodge basis). This project type now appears to have peaked in 2015, lifted in particular by an exceptional amount of activity in the New York NY metropolitan area, which is now settling back. Continued growth for multifamily housing in other metropolitan areas, along with still generally healthy market fundamentals, will enable the retreat at the national level to stay gradual.

- Commercial building will increase 6% on top of the 12% gain estimated for 2016. Office construction is showing improvement from very low levels, lifted by the start of several signature office towers and broad development efforts in downtown markets. Store construction should show some improvement from a very subdued 2016, and warehouses will register further growth. Hotel construction, while still healthy, will begin to retreat after a strong 2016.

- Institutional building will advance 10%, resuming its expansion after pausing in 2015 and 2016. The educational facilities category is seeing an increasing amount of K-12 school construction, supported by the passage of recent school construction bond measures. More growth is expected for the amusement category (convention centers, sports arenas, casinos) and transportation terminals.

- Manufacturing plant construction will increase 6%, beginning to recover after steep declines in 2015 and 2016 that reflected the pullback for large petrochemical plant starts.

- Public works construction will improve 6%, regaining upward momentum after slipping 3% in 2016. Highways and bridges will derive support from the new federal transportation bill, while environmental works should benefit from the expected passage of the Water Resources Development Act. Natural gas and oil pipeline projects are expected to stay close to the volume that’s been present in 2016.

- Electric utilities and gas plants will fall another 29% after the 26% decline in 2016. The lift that had been present in 2015 from new liquefied natural gas export terminals continues to dissipate. Power plant construction, which was supported in 2016 by the extension of investment tax credits, will ease back as new generating capacity comes on line.

The 2017 Dodge Construction Outlook was presented at the 78th annual Outlook Executive Conference held by Dodge Data & Analytics at the Gaylord National Resort and Convention Center in National Harbor, MD. Copies of the report with additional details by building sector can be ordered here or by calling (800) 591-4462.

Related Stories

Market Data | May 30, 2018

Construction employment increases in 256 metro areas between April 2017 & 2018

Dallas-Plano-Irving and Midland, Texas experience largest year-over-year gains; St. Louis, Mo.-Ill. and Bloomington, Ill. have biggest annual declines in construction employment amid continuing demand.

Market Data | May 29, 2018

America’s fastest-growing cities: San Antonio, Phoenix lead population growth

San Antonio added 24,208 people between July 2016 and July 2017, according to U.S. Census Bureau data.

Market Data | May 25, 2018

Construction group uses mobile technology to make highway work zones safer

Mobile advertising campaign urges drivers who routinely pass through certain work zones to slow down and be alert as new data shows motorists are more likely to be injured than construction workers.

Market Data | May 23, 2018

Architecture firm billings strengthen in April

Firms report solid growth for seven straight months.

Market Data | May 22, 2018

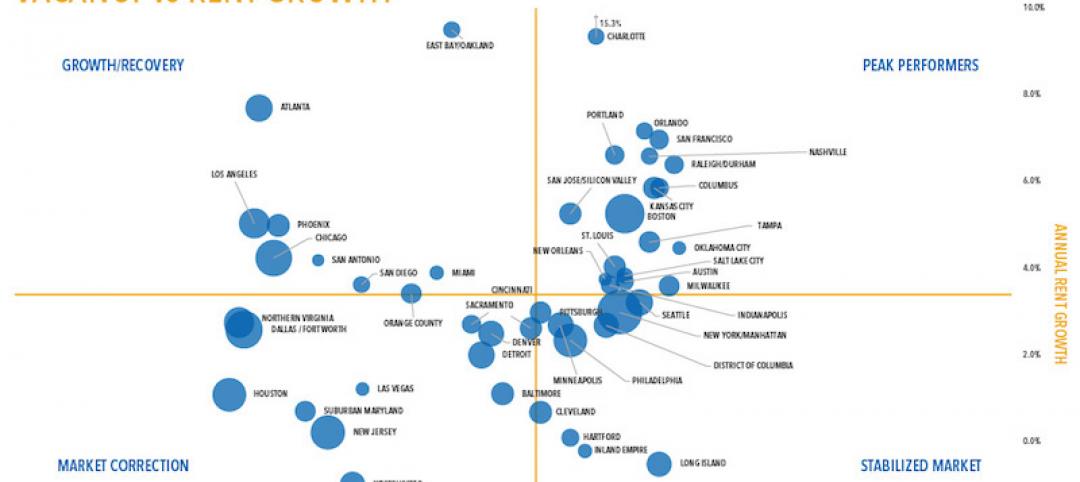

Vacancies stable, rents rising, and pipeline receding, according to Transwestern’s 1Q US Office Market report

The Big Apple still leads the new construction charge.

Market Data | May 18, 2018

Construction employment rises in 38 states and D.C. from April 2017 to April 2018

California & West Virginia have biggest annual job gains, North Dakota has largest decline; California & Louisiana have largest monthly pickup, Indiana & North Dakota lead monthly drops.

High-rise Construction | May 18, 2018

The 100 tallest buildings ever conventionally demolished

The list comes from a recent CTBUH study.

Resiliency | May 17, 2018

Architects brief lawmakers and policy-makers on disaster recovery as hurricane season approaches

Urge senate passage of disaster recovery reform act; Relationship-building with local communities.

Market Data | May 17, 2018

These 25 cities have the highest urban infill development potential

The results stem from a COMMERCIALCafé study.

Market Data | May 10, 2018

Construction costs surge in April as new tariffs and other trade measures lead to significant increases in materials prices

Association officials warn that the new tariffs and resulting price spikes have the potential to undermine benefits of tax and regulatory reform, urge administration to reconsider.