Between 2011 and 2016, the U.S. population age 50 years or older grew by 10.5 million to more than 112 million. While the vast majority of older Americans owns homes, homeownership rates are lower than the past, and a significant number of adults drawing closer to retirement might not have the financial wherewithal to afford to either buy or rent where they want to live.

That is the primary concern expressed by the latest Joint Center for Housing Studies’ report “Housing America’s Older Adults 2018,” which releases today.

The study relies mostly on data up to 2016, and reiterates a common theme in many of the Joint Center’s past papers: that America’s affordable housing stock is woefully inadequate to address demographic and economic trends that continue to reshape this country, especially in light of other trends in healthcare and the social safety net.

There are 65 million older households in the U.S. The homeownership rate for those headed by someone 50 years or older is 76.2%, and 78.7% of households headed by someone 65 or older.

The Joint Center’s report notes that the majority of older households are white, and live in single-family homes. The demographic profile of older Americans, however, is likely to get more racially and ethnically diverse. And more older adults have been moving into multifamily housing, possibly because larger buildings are more likely to offer accessibility features.

More older households now consist of older unmarried adults who are doubling up, or living in multigenerational households. This is especially true among people age 65-79.

Perhaps The Joint Center’s greatest concern is the steady decline, since 2004, in the rate for households age 50–64, and an even sharper dip for adults approaching age 50. “Since this younger group is unlikely to match the homeownership rates of previous generations, many of these households will be unable to generate the same levels of wealth for retirement through equity building,” the report posits.

Nearly a quarter of households age 50 or older rent. Given that the median income of older renters ($28,000) is less than half that of older owners ($61,000), the decision to rent often comes out of necessity. Most of the 43% growth in the number of older renters since 2006 has, in fact, been among households earning under $30,000 per year.

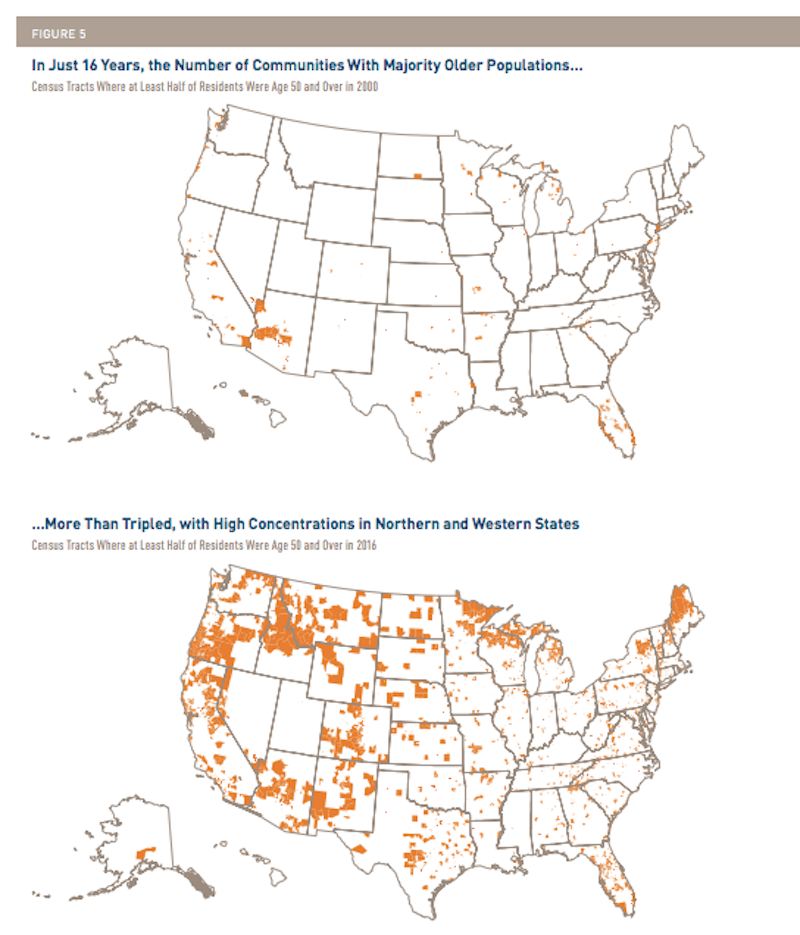

Where people reside is an important factor in this analysis. Although the number of people age 65 and over living in dense urban areas grew by nearly 800,000 between 2000 and 2016, the share of all older adults living in such neighborhoods actually fell. Meanwhile, the shares living in low-density metro tracts rose significantly, from 24% to 32%—an increase of more than six million. The growing presence of older adults in lower-density communities largely results from aging in place.

The implication here is that it might be harder for older adults to find the healthcare and services they require as they age.

More seniors at a financial precipice

The U.S. housing market is ill-prepared to cope with the explosion of seniors across the country, a sizable proportion of whom are nearing retirement facing financial uncertainty. Image: Joint Center for Housign Studies

The median homeowner aged 50–64 had a net worth of $292,000 in 2016—almost 60 times that of the same-age median renter. Even excluding home equity, the net worth of owner households aged 50–64 was still nearly 30 times higher than that of same-age renters, while the net worth of owners age 65 and over was more than 24 times higher.

This disparity might explain why more Americans are working past 65. Over the past three decades, the labor force participation rate rose 12.8 percentage points for 65–69 year olds, and 9.5 points for 70–74 year olds. In 2017, 8.3% of the population age 75 and over was either employed or actively looking for work—nearly double the share 30 years ago.

It’s a good thing they’re working because more than two-fifths of owners 65 or older still have mortgages to pay off. Between 1989 and 2016, the loan-to-vale rations doubled to 51% for mortgage holders aged 50-64, and tripled to 39% for those age 65 or older.

The number of households age 65 and over with housing cost burdens continues to climb. In 2016, 9.7 million households in this age group—nearly a third—spent more than 30% of their incomes for housing. About 4.9 million were severely burdened, paying at least half their incomes for housing

Although the cost-burdened share of 50–64 year olds did decline a fraction of a point to 19.9% in 2014–2016, a total of 10.2 million households in this age group still faced at least moderate cost burdens, and nearly half of those households had severe burdens.

Social Security payments accounted for 69% of the income for the median older household in 2016. But between 2006 and 2016, Social Security payments rose just 6% in real terms while the median rent for households age 65 and over climbed at twice that rate. Looking ahead, the ability of many older adults to afford their housing will be closely tied to the fate of the Social Security program.

The financial precariousness of older Americans is exacerbated by healthcare concerns and costs that might limit their housing options. In 2016, 26% of households age 50 and over included a member with at least one vision, hearing, cognitive, self-care, mobility, or independent living difficulty. Difficulty climbing stairs or walking is the most common disability, affecting 17% of these households. Minority households are more likely than same-age white households to have at least one difficulty, although differences narrow over time.

Consider these statistics in light of the fact that few homes in the U.S. are accessible to people with mobility problems, particularly those requiring a wheelchair.

The good news is that that some older owners have come to grips with their possible debilities. The American Housing Survey shows that among owners age 65 and over who reported home-improvement spending in 2016–2017, 11% indicated that at least one of their projects was related to accessibility. Households in the 55-and-over age group already account for more than half of home improvement spending, and Joint Center projections suggest they will drive more than three-quarters of the growth in renovation spending in 2015–2025.

But renters, as well as owners with little wealth, may require government assistance to make their homes more accessible.

As if all this weren’t daunting enough, the Joint Center states that climate change doesn’t bode well for older adults who are much more at risk from extreme weather events and natural disasters than younger age groups.

The report’s outlook is another warning shot: Many households currently in their 50s and early 60s are not financially prepared for retirement, with lower homeownership rates than their predecessors and meager gains in income and wealth. In addition, many older adults live in low-density areas and in single-family homes, which adds to the pressures on their communities to provide new housing and transportation options for households in need. And as the baby boomers begin to turn 80 in the decade ahead, growing numbers of households will require affordable, accessible housing as well as supportive services.

State and local governments, as well as the private and nonprofit sectors, all have roles to play in developing more affordable and suitable housing for older households. Families and individuals also have a responsibility to plan for the future and to advocate for more age-friendly housing and communities. But given the current and growing scale of need, addressing the challenges of housing America’s older adults must also be a federal priority.

Related Stories

Contractors | Feb 14, 2023

The average U.S. contractor has nine months worth of construction work in the pipeline

Associated Builders and Contractors reports today that its Construction Backlog Indicator declined 0.2 months to 9.0 in January, according to an ABC member survey conducted Jan. 20 to Feb. 3. The reading is 1.0 month higher than in January 2022.

Office Buildings | Feb 9, 2023

Post-Covid Manhattan office market rebound gaining momentum

Office workers in Manhattan continue to return to their workplaces in sufficient numbers for many of their employers to maintain or expand their footprint in the city, according to a survey of more than 140 major Manhattan office employers conducted in January by The Partnership for New York City.

Giants 400 | Feb 9, 2023

New Giants 400 download: Get the complete at-a-glance 2022 Giants 400 rankings in Excel

See how your architecture, engineering, or construction firm stacks up against the nation's AEC Giants. For more than 45 years, the editors of Building Design+Construction have surveyed the largest AEC firms in the U.S./Canada to create the annual Giants 400 report. This year, a record 519 firms participated in the Giants 400 report. The final report includes 137 rankings across 25 building sectors and specialty categories.

Multifamily Housing | Feb 7, 2023

Multifamily housing rents flat in January, developers remain optimistic

Multifamily rents were flat in January 2023 as a strong jobs report indicated that fears of a significant economic recession may be overblown. U.S. asking rents averaged $1,701, unchanged from the prior month, according to the latest Yardi Matrix National Multifamily Report.

Market Data | Feb 6, 2023

Nonresidential construction spending dips 0.5% in December 2022

National nonresidential construction spending decreased by 0.5% in December, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $943.5 billion for the month.

Architects | Jan 23, 2023

PSMJ report: The fed’s wrecking ball is hitting the private construction sector

Inflation may be starting to show some signs of cooling, but the Fed isn’t backing down anytime soon and the impact is becoming more noticeable in the architecture, engineering, and construction (A/E/C) space. The overall A/E/C outlook continues a downward trend and this is driven largely by the freefall happening in key private-sector markets.

Hotel Facilities | Jan 23, 2023

U.S. hotel construction pipeline up 14% to close out 2022

At the end of 2022’s fourth quarter, the U.S. construction pipeline was up 14% by projects and 12% by rooms year-over-year, according to Lodging Econometrics.

Products and Materials | Jan 18, 2023

Is inflation easing? Construction input prices drop 2.7% in December 2022

Softwood lumber and steel mill products saw the biggest decline among building construction materials, according to the latest U.S. Bureau of Labor Statistics’ Producer Price Index.

Market Data | Jan 10, 2023

Construction backlogs at highest level since Q2 2019, says ABC

Associated Builders and Contractors reports today that its Construction Backlog Indicator remained unchanged at 9.2 months in December 2022, according to an ABC member survey conducted Dec. 20, 2022, to Jan. 5, 2023. The reading is one month higher than in December 2021.

Market Data | Jan 6, 2023

Nonresidential construction spending rises in November 2022

Spending on nonresidential construction work in the U.S. was up 0.9% in November versus the previous month, and 11.8% versus the previous year, according to the U.S. Census Bureau.