In the recent U.S. Construction Pipeline Trend Report released by Lodging Econometrics (LE), at the close of Q1‘21, New York City continues to hold the lead amongst U.S. markets for the most projects in the U.S. construction pipeline with 145 projects/24,762 rooms. Other U.S. markets that follow are Los Angeles with 144 projects/23,994 rooms, Dallas with 135 projects/16,260 rooms, Atlanta with 132 projects/18,264 rooms, and Orlando with 98 projects/17,536 rooms.

New York City has the greatest number of projects under construction with 110 projects/19,457 rooms. Following New York City with the highest number of projects under construction is Los Angeles with 39 projects/6,657 rooms, and then Atlanta with 39 projects/5,500 rooms, Dallas with 32 projects/3,795 rooms, and Orlando with 27 projects/4,693 rooms.

The top 50 markets in the U.S. announced a total of 74 new projects, accounting for 10,219 rooms, during Q1 ’21. The leading markets for new project announcements include Riverside-San Bernardino, CA with 6 projects/633 rooms, Los Angeles with 5 projects accounting for 768 rooms, Phoenix with 5 projects/402 rooms, Nashville with 4 projects/692 rooms, and San Diego with 4 projects/474 rooms. New project announcements have been slow in the wake of the pandemic, due in part to the inability to conduct business in the traditional pre-COVID way, but developers are increasingly optimistic and anxious to move forward with new projects as the country fully reopens.

Experts at LE are seeing an increase in renovation and brand conversion activity throughout the top 50 markets. During Q1, 1,198 projects/190,475 rooms were in the renovation/conversion pipeline. There are over ten markets in the U.S. that currently have more than 15 substantial renovation and conversion projects underway. This group is led by Houston with 27 projects, Los Angeles, and New York, each with 22 projects, followed by Chicago, Miami, Phoenix, Washington DC, Atlanta, Dallas, Orlando, and Philadelphia.

In the first quarter of 2021, the top 50 markets saw 128 hotels/17,636 rooms open. LE is forecasting these same 50 markets to open another 367 projects/47,592 rooms over the next three quarters, for a total of 495 projects/65,228 rooms in 2021.

Related Stories

Multifamily Housing | May 18, 2021

Multifamily housing sector sees near record proposal activity in early 2021

The multifamily sector led all housing submarkets, and was third among all 58 submarkets tracked by PSMJ in the first quarter of 2021.

Market Data | May 18, 2021

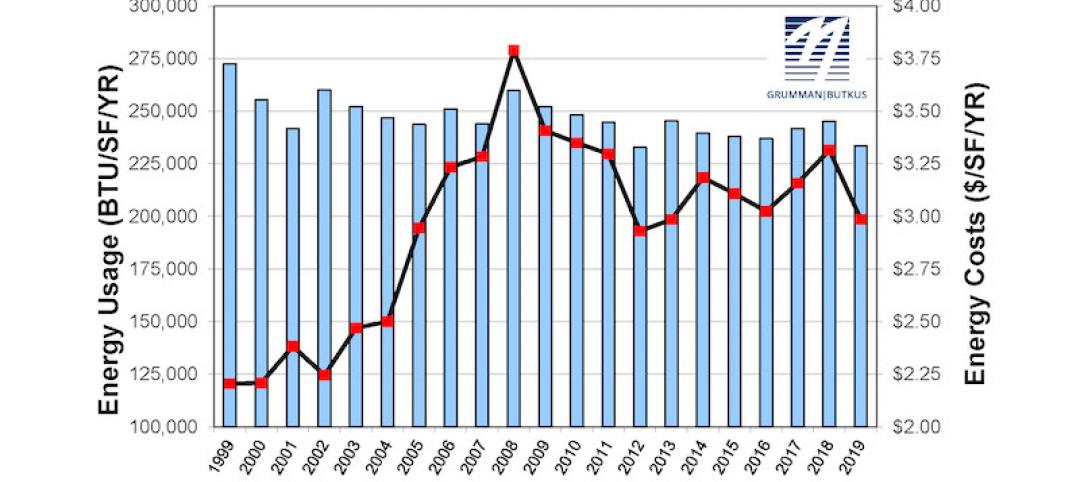

Grumman|Butkus Associates publishes 2020 edition of Hospital Benchmarking Survey

The report examines electricity, fossil fuel, water/sewer, and carbon footprint.

Market Data | May 13, 2021

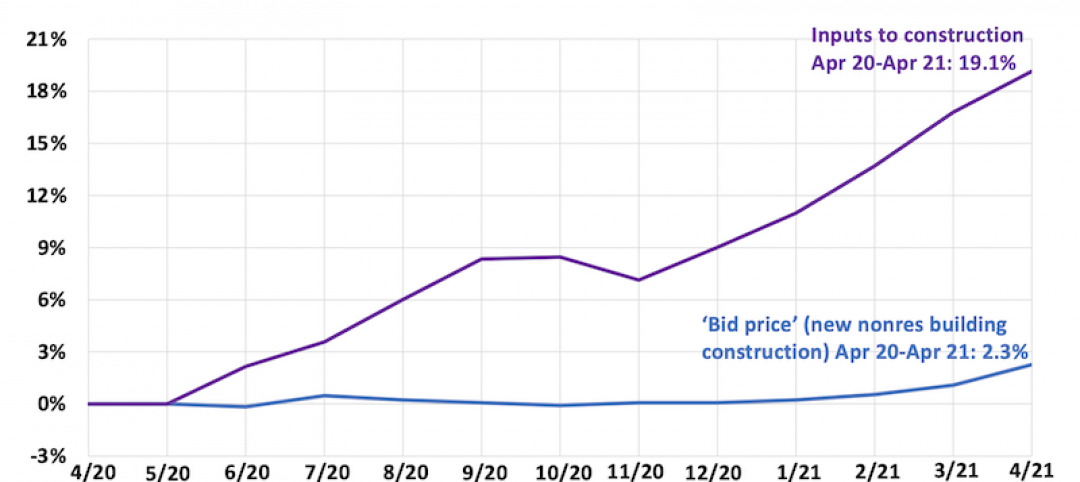

Proliferating materials price increases and supply chain disruptions squeeze contractors and threaten to undermine economic recovery

Producer price index data for April shows wide variety of materials with double-digit price increases.

Market Data | May 7, 2021

Construction employment stalls in April

Soaring costs, supply-chain challenges, and workforce shortages undermine industry's recovery.

Market Data | May 4, 2021

Nonresidential construction outlays drop in March for fourth-straight month

Weak demand, supply-chain woes make further declines likely.

Market Data | May 3, 2021

Nonresidential construction spending decreases 1.1% in March

Spending was down on a monthly basis in 11 of the 16 nonresidential subcategories.

Market Data | Apr 29, 2021

U.S. Hotel Construction pipeline beings 2021 with 4,967 projects/622,218 rooms at Q1 close

Although hotel development may still be tepid in Q1, continued government support and the extension of programs has aided many businesses to get back on their feet as more and more are working to re-staff and re-open.

Market Data | Apr 28, 2021

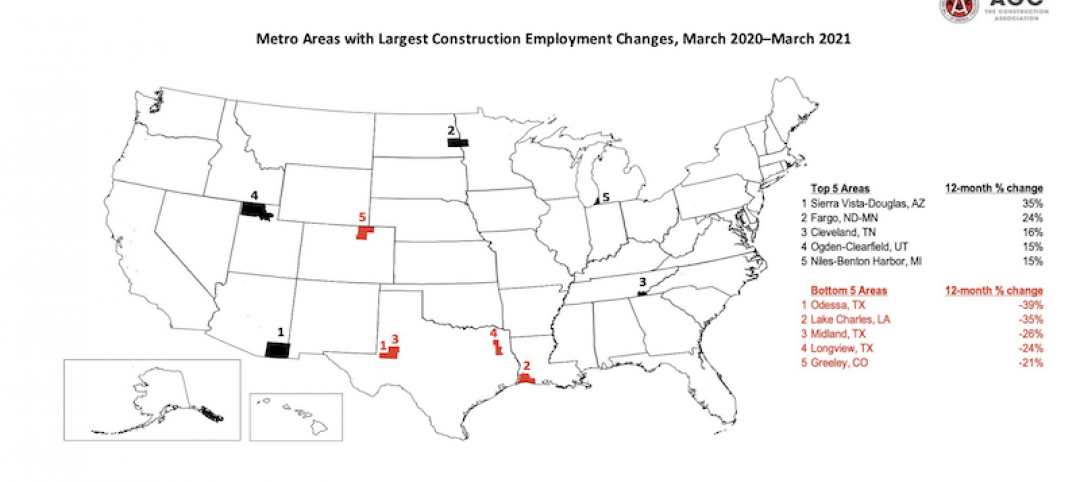

Construction employment declines in 203 metro areas from March 2020 to March 2021

The decline occurs despite homebuilding boom and improving economy.

Market Data | Apr 20, 2021

The pandemic moves subs and vendors closer to technology

Consigli’s latest market outlook identifies building products that are high risk for future price increases.

Market Data | Apr 20, 2021

Demand for design services continues to rapidly escalate

AIA’s ABI score for March rose to 55.6 compared to 53.3 in February.