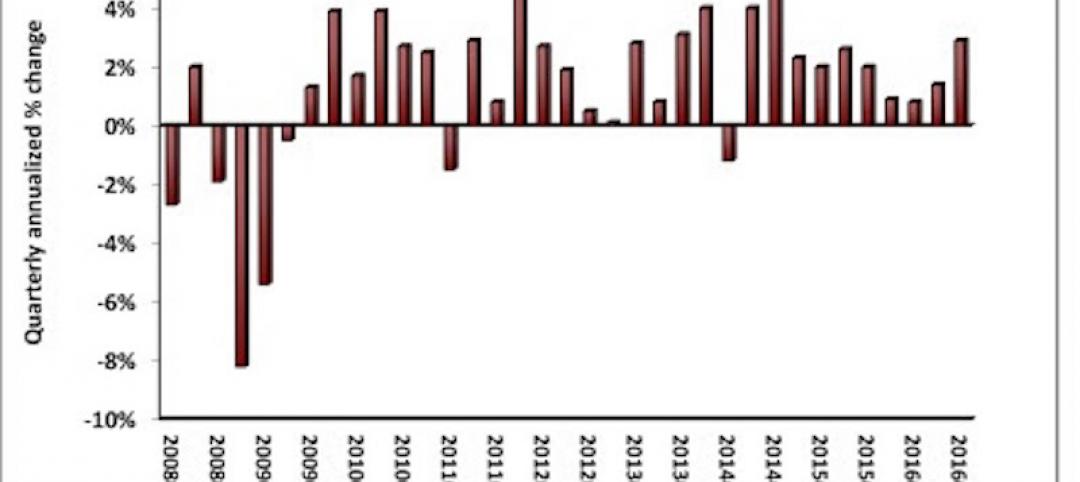

Coming off of a year when nonresidential building starts fell by an estimated 7.5%, the industry is expected to bounce back in 2016, especially during the second and third quarters when the annualized growth rate for starts could hit 15% before decelerating later in the year.

However, keeping projects on schedule and on budget will continue to be difficult if, as expected, worker shortages persist, leading to higher labor costs and, potentially, construction delays.

In Gilbane’s Winter 2015-2016 Market Conditions in Construction report, which can be downloaded from here, the giant contractor forecasts nonresidential building starts to increase by 8.5% this year to 222,764.

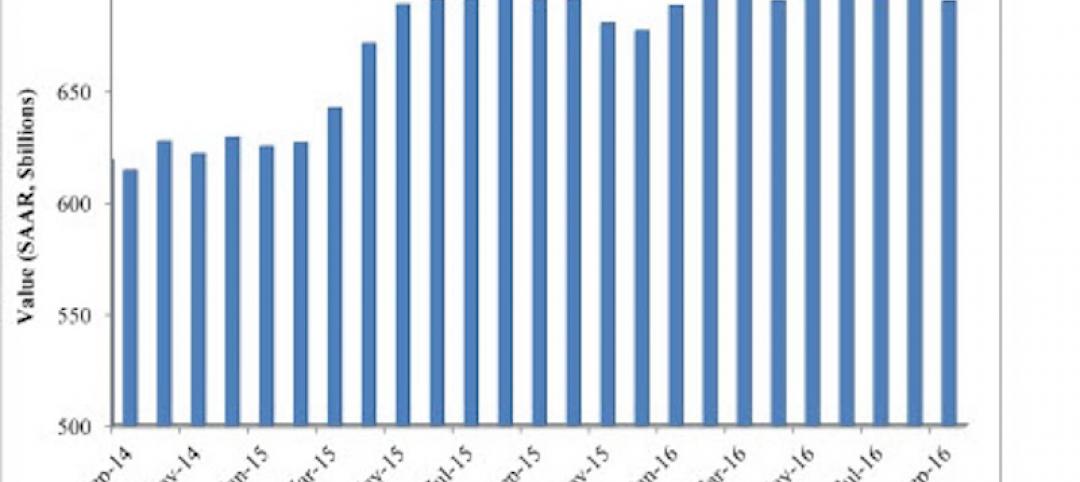

Gilbane expects spending on nonresidential buildings, which grew by 17.1% to $386.4 billion in 2015, to keep rising this year, by 13.7% to $439.2 billion. However, spending should taper off late this year, “leading to a considerably slower 2017.”

On the whole, nonresidential building sectors should enjoy good years, according to Gilbane’s report, whose spending projections for 2016 include:

•13.6% growth for Educational buildings

•A 13.8% rise for Healthcare construction

•22.5% growth for Amusement and Recreational buildings.

•A 6% spending increase for Retail space

•A retreat in spending for Office buildings, which after gains of 21.3% and 21.4% in the last two years, should increase by only 4.7% in 2016. “Although down 15% in 2015, starts have been strong and multiple months of large volume starts will help keep 2016 spending positive. Office spending is projected to grow again in 2017,” the report states.

•Spending for lodging, which grew by 31% last year, and by 90% during the 2012-2015 period, should increase by 10.8% this year, when starts are expected to be up 16%, “leading to continued spending growth in 2017.”

•Despite a nearly 30% decline in starts last year, manufacturing-related building still hit its second-highest starts level on record, and spending jumped 44.8%. Those starts should drive spending up another 10.8% in 2016.

On average, $1 billion of spending supports approximately 6,000 construction jobs, and generates up to 28,000 jobs in the economy. But Gilbane remains concerned about the ability of contractors to find skilled labor to meet the country’s escalating construction demands. It points out that while the total construction workforce is growing and is near 7.3 million, that is still about 1 million workers short of the 2006-2007 peak.

It cites the Bureau of Labor Statistics’ Job Openings and Labor Turnover Survey (JOLTS) for the construction industry, which showed 139,000 unfilled positions for October 2015. Gilbane notes that the openings rate has been trending upward since 2012. “A relatively high rate of openings … generally indicates high demand for labor and could lead to higher wage rates,” its report states.

Gilbane’s analyst Ed Zarenski expects construction job gains of between 500,000 and 600,000 through 2017. But Gilbane still foresees shortages of skilled workers over the next five years, as well as declining productivity, and rapidly increasing labor cost. “If you are in a location where a large volume of pent-up work starts all at once, you will experience these three issues.”

Related Stories

Market Data | Nov 2, 2016

Nonresidential construction spending down in September, but August data upwardly revised

The government revised the August nonresidential construction spending estimate from $686.6 billion to $696.6 billion.

Market Data | Oct 31, 2016

Nonresidential fixed investment expands again during solid third quarter

The acceleration in real GDP growth was driven by a combination of factors, including an upturn in exports, a smaller decrease in state and local government spending and an upturn in federal government spending, says ABC Chief Economist Anirban Basu.

Market Data | Oct 28, 2016

U.S. construction solid and stable in Q3 of 2016; Presidential election seen as influence on industry for 2017

Rider Levett Bucknall’s Third Quarter 2016 USA Construction Cost Report puts the complete spectrum of construction sectors and markets in perspective as it assesses the current state of the industry.

Industry Research | Oct 25, 2016

New HOK/CoreNet Global report explores impact of coworking on corporate real rstate

“Although coworking space makes up less than one percent of the world’s office space, it represents an important workforce trend and highlights the strong desire of today’s employees to have workplace choices, community and flexibility,” says Kay Sargent, Director of WorkPlace at HOK.

Market Data | Oct 24, 2016

New construction starts in 2017 to increase 5% to $713 billion

Dodge Outlook Report predicts moderate growth for most project types – single family housing, commercial and institutional building, and public works, while multifamily housing levels off and electric utilities/gas plants decline.

High-rise Construction | Oct 21, 2016

The world’s 100 tallest buildings: Which architects have designed the most?

Two firms stand well above the others when it comes to the number of tall buildings they have designed.

Market Data | Oct 19, 2016

Architecture Billings Index slips consecutive months for first time since 2012

“This recent backslide should act as a warning signal,” said AIA Chief Economist, Kermit Baker.

Market Data | Oct 11, 2016

Building design revenue topped $28 billion in 2015

Growing profitability at architecture firms has led to reinvestment and expansion

Market Data | Oct 4, 2016

Nonresidential spending slips in August

Public sector spending is declining faster than the private sector.

Industry Research | Oct 3, 2016

Structure Tone survey shows cost is still a major barrier to building green

Climate change, resilience and wellness are also growing concerns.