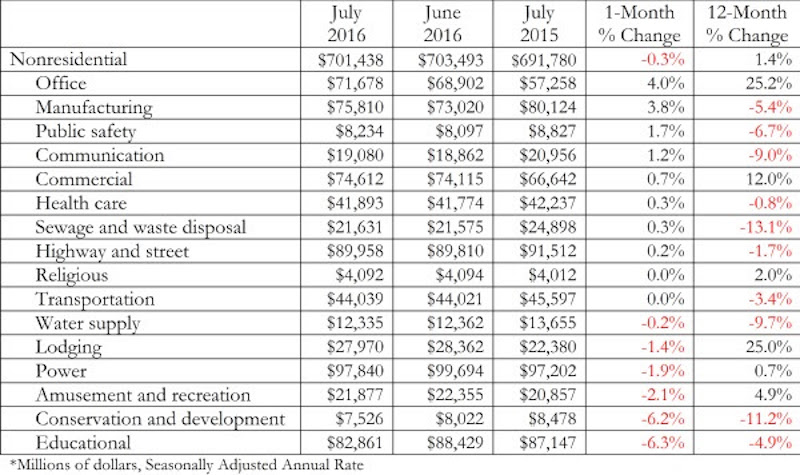

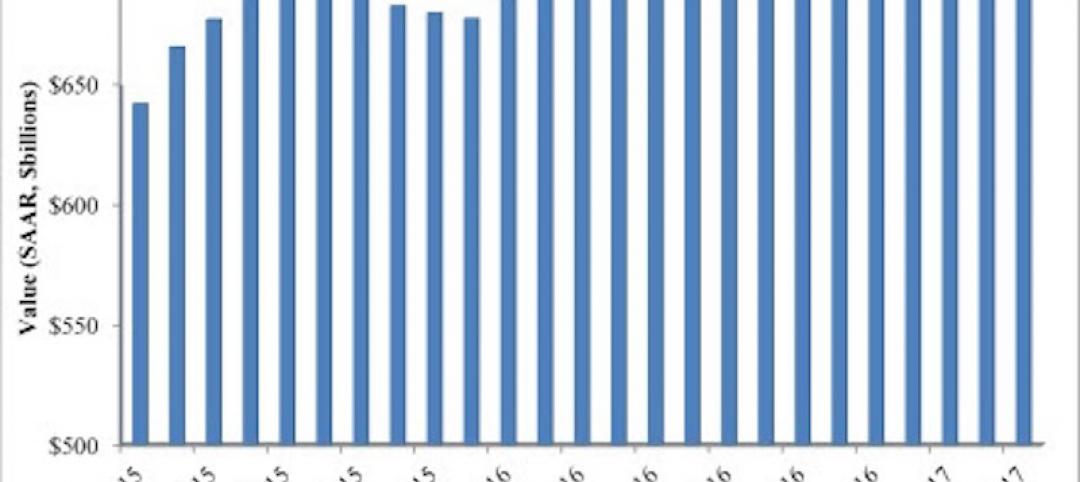

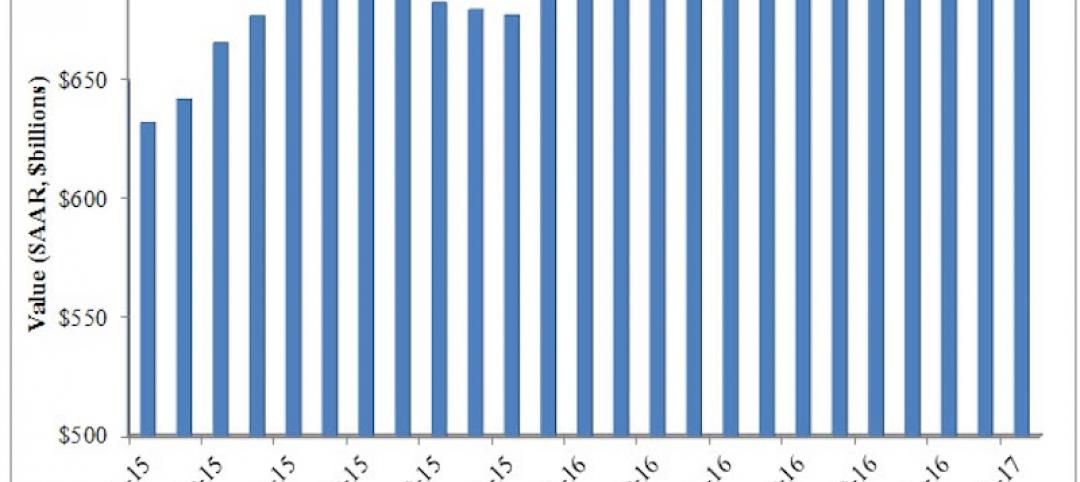

Nonresidential construction spending inched 0.3 percent lower in July largely due to a significant upward revision to June’s spending figure, according to analysis of U.S. Census Bureau data released today by Associated Builders and Contractors (ABC). Nonresidential spending totaled $701.4 billion on a seasonally adjusted annualized basis in July, the second highest month since November of 2008, right behind June, which was revised upward from $682 billion to $703.5 billion. Public nonresidential spending continued to falter, declining 3.2 percent for the month and 6.5 percent for the year.

Nonresidential construction spending has been suppressed over the last year or so with the primary factor being the lack of momentum in public spending. “This lack of public investment continues despite obvious deficiencies in water, road and other forms of infrastructure. The fact that all but two of the 12 public nonresidential public subsectors declined in July shows that the malaise is widespread,” says ABC Chief Economist Anirban Basu in a press release.

The second biggest factor deals with tightening commercial real estate standards that may have been brought on by growing regulatory pressures. “There is growing concern that key commercial real estate segments are in the process of being overbuilt, particularly in America’s largest cities, which are most likely to attract significant levels of foreign investment,” Basu says.

All is not negative, however, as the housing sector has begun to improve at a meaningful rate and the country continues to add a substantial number of jobs. Additionally, interest rates remain low.

Related Stories

Market Data | May 2, 2017

Nonresidential Spending loses steam after strong start to year

Spending in the segment totaled $708.6 billion on a seasonally adjusted, annualized basis.

Market Data | May 1, 2017

Nonresidential Fixed Investment surges despite sluggish economic in first quarter

Real gross domestic product (GDP) expanded 0.7 percent on a seasonally adjusted annualized rate during the first three months of the year.

Industry Research | Apr 28, 2017

A/E Industry lacks planning, but still spending large on hiring

The average 200-person A/E Firm is spending $200,000 on hiring, and not budgeting at all.

Architects | Apr 27, 2017

Number of U.S. architects holds steady, while professional mobility increases

New data from NCARB reveals that while the number of architects remains consistent, practitioners are looking to get licensed in multiple states.

Market Data | Apr 6, 2017

Architecture marketing: 5 tools to measure success

We’ve identified five architecture marketing tools that will help your firm evaluate if it’s on the track to more leads, higher growth, and broader brand visibility.

Market Data | Apr 3, 2017

Public nonresidential construction spending rebounds; overall spending unchanged in February

The segment totaled $701.9 billion on a seasonally adjusted annualized rate for the month, marking the seventh consecutive month in which nonresidential spending sat above the $700 billion threshold.

Market Data | Mar 29, 2017

Contractor confidence ends 2016 down but still in positive territory

Although all three diffusion indices in the survey fell by more than five points they remain well above the threshold of 50, which signals that construction activity will continue to be one of the few significant drivers of economic growth.

Industry Research | Mar 24, 2017

The business costs and benefits of restroom maintenance

Businesses that have pleasant, well-maintained restrooms can turn into customer magnets.

Industry Research | Mar 22, 2017

Progress on addressing US infrastructure gap likely to be slow despite calls to action

Due to a lack of bipartisan agreement over funding mechanisms, as well as regulatory hurdles and practical constraints, Moody’s expects additional spending to be modest in 2017 and 2018.

Industry Research | Mar 21, 2017

Staff recruitment and retention is main concern among respondents of State of Senior Living 2017 survey

The survey asks respondents to share their expertise and insights on Baby Boomer expectations, healthcare reform, staff recruitment and retention, for-profit competitive growth, and the needs of middle-income residents.