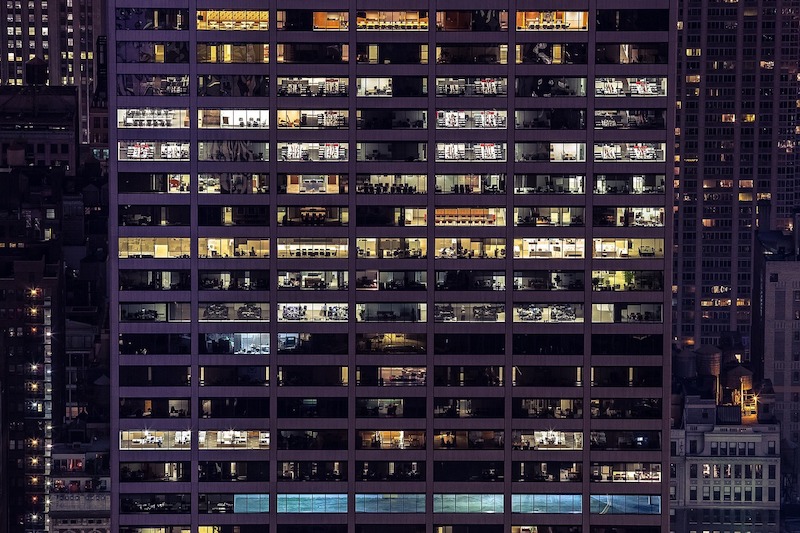

A rising tide of new office projects may be skewing the national average rental rate upward and obscuring increased leasing challenges for second-generation properties in many markets, Transwestern’s latest U.S. office market report suggests.

Monthly asking rent averaged $26.97 per square foot in the third quarter, representing a 3.4% increase from a year earlier and a five-year gain of 19.7%. Much of that national increase reflects above-market rents at new or renovated projects, where landlords have incurred elevated material and labor costs to complete amenity-rich offerings.

The national vacancy rate has plateaued near 9.8%, equal to the rate one year ago. A dozen of the 49 markets Transwestern tracks showed negative net absorption or an increase in the volume of vacant space for the 12 months ended September. Nationwide, annualized absorption through the third quarter was 57.3 million square feet, or roughly one-third less than the 85.2 million square feet absorbed in 2018.

Office construction is at a cyclical high. Building starts in the 12 months through the third quarter were up 12.1% over the year-ago period, with more than 166 million square feet of projects underway. The sector delivered 18.5 million square feet of new space in the recent quarter, less than the second quarter’s 21.7 million square feet but up 1.3% from a year earlier, while the national economy and average monthly job growth have slowed.

“Developers have responded vigorously to tenant preferences for new construction,” said Jimmy Hinton, Senior Managing Director of Investment & Analytics at Transwestern. “In many markets, new construction is outpacing already moderating tenant demand, creating extra pressure on older-vintage properties. Landlords are increasingly challenged in reconciling capital improvement needs with cycle timing and prospects for suitable investment returns.”

While high-end rents at new properties can increase a market’s average lease rate, new construction drives rent downward when landlords feel pressure to compete for tenants by lowering rates. In Houston, for example, average third quarter asking rent had declined 0.7% from a year earlier.

Stuart Showers, Vice President of Research in Houston, predicts other markets will experience a similar shift in the coming months, and could represent a late-cycle playbook for landlords in other markets, should macro conditions deteriorate.

“The volume of new office construction pushing through Houston has resulted in downward pressure on rental rates, a situation that will manifest throughout second-generation product in a number of the nation’s markets that have high construction activity,” Showers said.

Download the full third quarter 2019 U.S. office market report at: www.twurls.com/us-office-3q19

Related Stories

Apartments | Aug 22, 2023

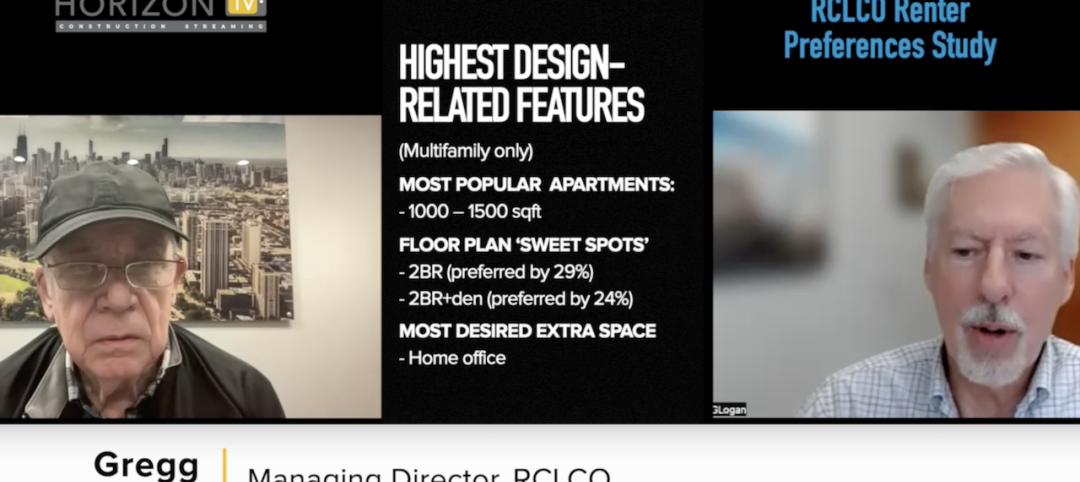

Key takeaways from RCLCO's 2023 apartment renter preferences study

Gregg Logan, Managing Director of real estate consulting firm RCLCO, reveals the highlights of RCLCO's new research study, “2023 Rental Consumer Preferences Report.” Logan speaks with BD+C's Robert Cassidy.

Market Data | Aug 18, 2023

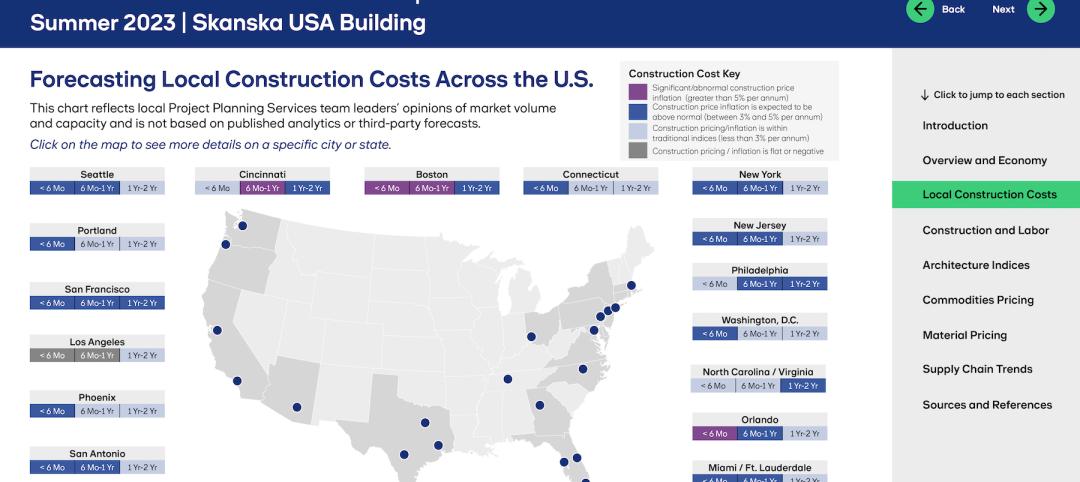

Construction soldiers on, despite rising materials and labor costs

Quarterly analyses from Skanska, Mortenson, and Gordian show nonresidential building still subject to materials and labor volatility, and regional disparities.

Apartments | Aug 14, 2023

Yardi Matrix updates near-term multifamily supply forecast

The multifamily housing supply could increase by up to nearly 7% by the end of 2023, states the latest Multifamily Supply Forecast from Yardi Matrix.

Hotel Facilities | Aug 2, 2023

Top 5 markets for hotel construction

According to the United States Construction Pipeline Trend Report by Lodging Econometrics (LE) for Q2 2023, the five markets with the largest hotel construction pipelines are Dallas with a record-high 184 projects/21,501 rooms, Atlanta with 141 projects/17,993 rooms, Phoenix with 119 projects/16,107 rooms, Nashville with 116 projects/15,346 rooms, and Los Angeles with 112 projects/17,797 rooms.

Market Data | Aug 1, 2023

Nonresidential construction spending increases slightly in June

National nonresidential construction spending increased 0.1% in June, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. Spending is up 18% over the past 12 months. On a seasonally adjusted annualized basis, nonresidential spending totaled $1.07 trillion in June.

Hotel Facilities | Jul 27, 2023

U.S. hotel construction pipeline remains steady with 5,572 projects in the works

The hotel construction pipeline grew incrementally in Q2 2023 as developers and franchise companies push through short-term challenges while envisioning long-term prospects, according to Lodging Econometrics.

Hotel Facilities | Jul 26, 2023

Hospitality building construction costs for 2023

Data from Gordian breaks down the average cost per square foot for 15-story hotels, restaurants, fast food restaurants, and movie theaters across 10 U.S. cities: Boston, Chicago, Las Vegas, Los Angeles, Miami, New Orleans, New York, Phoenix, Seattle, and Washington, D.C.

Market Data | Jul 24, 2023

Leading economists call for 2% increase in building construction spending in 2024

Following a 19.7% surge in spending for commercial, institutional, and industrial buildings in 2023, leading construction industry economists expect spending growth to come back to earth in 2024, according to the July 2023 AIA Consensus Construction Forecast Panel.

Contractors | Jul 13, 2023

Construction input prices remain unchanged in June, inflation slowing

Construction input prices remained unchanged in June compared to the previous month, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics Producer Price Index data released today. Nonresidential construction input prices were also unchanged for the month.

Contractors | Jul 11, 2023

The average U.S. contractor has 8.9 months worth of construction work in the pipeline, as of June 2023

Associated Builders and Contractors reported that its Construction Backlog Indicator remained unchanged at 8.9 months in June 2023, according to an ABC member survey conducted June 20 to July 5. The reading is unchanged from June 2022.