A rising tide of new office projects may be skewing the national average rental rate upward and obscuring increased leasing challenges for second-generation properties in many markets, Transwestern’s latest U.S. office market report suggests.

Monthly asking rent averaged $26.97 per square foot in the third quarter, representing a 3.4% increase from a year earlier and a five-year gain of 19.7%. Much of that national increase reflects above-market rents at new or renovated projects, where landlords have incurred elevated material and labor costs to complete amenity-rich offerings.

The national vacancy rate has plateaued near 9.8%, equal to the rate one year ago. A dozen of the 49 markets Transwestern tracks showed negative net absorption or an increase in the volume of vacant space for the 12 months ended September. Nationwide, annualized absorption through the third quarter was 57.3 million square feet, or roughly one-third less than the 85.2 million square feet absorbed in 2018.

Office construction is at a cyclical high. Building starts in the 12 months through the third quarter were up 12.1% over the year-ago period, with more than 166 million square feet of projects underway. The sector delivered 18.5 million square feet of new space in the recent quarter, less than the second quarter’s 21.7 million square feet but up 1.3% from a year earlier, while the national economy and average monthly job growth have slowed.

“Developers have responded vigorously to tenant preferences for new construction,” said Jimmy Hinton, Senior Managing Director of Investment & Analytics at Transwestern. “In many markets, new construction is outpacing already moderating tenant demand, creating extra pressure on older-vintage properties. Landlords are increasingly challenged in reconciling capital improvement needs with cycle timing and prospects for suitable investment returns.”

While high-end rents at new properties can increase a market’s average lease rate, new construction drives rent downward when landlords feel pressure to compete for tenants by lowering rates. In Houston, for example, average third quarter asking rent had declined 0.7% from a year earlier.

Stuart Showers, Vice President of Research in Houston, predicts other markets will experience a similar shift in the coming months, and could represent a late-cycle playbook for landlords in other markets, should macro conditions deteriorate.

“The volume of new office construction pushing through Houston has resulted in downward pressure on rental rates, a situation that will manifest throughout second-generation product in a number of the nation’s markets that have high construction activity,” Showers said.

Download the full third quarter 2019 U.S. office market report at: www.twurls.com/us-office-3q19

Related Stories

Market Data | Nov 30, 2016

Marcum Commercial Construction Index reports industry outlook has shifted; more change expected

Overall nonresidential construction spending in September totaled $690.5 billion, down a slight 0.7 percent from a year earlier.

Industry Research | Nov 30, 2016

Multifamily millennials: Here is what millennial renters want in 2017

It’s all about technology and convenience when it comes to the things millennial renters value most in a multifamily facility.

Market Data | Nov 29, 2016

It’s not just traditional infrastructure that requires investment

A national survey finds strong support for essential community buildings.

Industry Research | Nov 28, 2016

Building America: The Merit Shop Scorecard

ABC releases state rankings on policies affecting construction industry.

Multifamily Housing | Nov 28, 2016

Axiometrics predicts apartment deliveries will peak by mid 2017

New York is projected to lead the nation next year, thanks to construction delays in 2016

Market Data | Nov 22, 2016

Construction activity will slow next year: JLL

Risk, labor, and technology are impacting what gets built.

Market Data | Nov 17, 2016

Architecture Billings Index rebounds after two down months

Decline in new design contracts suggests volatility in design activity to persist.

Market Data | Nov 11, 2016

Brand marketing: Why the B2B world needs to embrace consumers

The relevance of brand recognition has always been debatable in the B2B universe. With notable exceptions like BASF, few manufacturers or industry groups see value in generating top-of-mind awareness for their products and services with consumers.

Industry Research | Nov 8, 2016

Austin, Texas wins ‘Top City’ in the Emerging Trends in Real Estate outlook

Austin was followed on the list by Dallas/Fort Worth, Texas and Portland, Ore.

Market Data | Nov 2, 2016

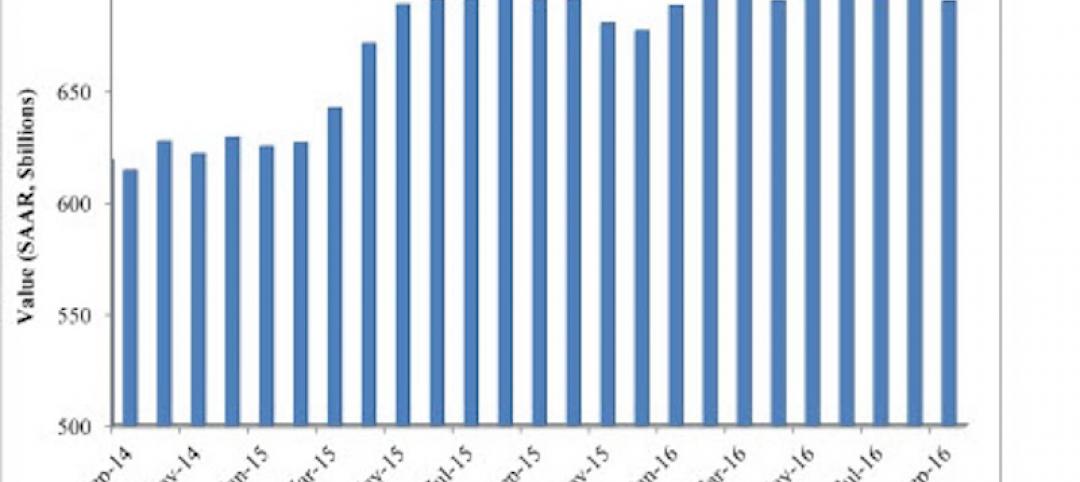

Nonresidential construction spending down in September, but August data upwardly revised

The government revised the August nonresidential construction spending estimate from $686.6 billion to $696.6 billion.