A recent survey of more than 200 subcontractors and suppliers in the Northeast found that respondents have been prefabricating 20% more than they did prior to the COVID-19 pandemic. And 71% said that they had seen an increase in requests for design-assist proposals, a strong sign that speed-to-market is a priority.

Consigli Construction’s Market Outlook Report for the first and second quarters of 2021 states that the pandemic has motivated subs and vendors to turn to technology in their shops and field processes. The survey’s respondents are also more receptive to cost-saving material management software, tool upgrades, and robotics that improve efficiency and give subs the flexibility they need to manage on-site workforces at a time when skilled labor is in short supply in some markets.

While 72% of the survey’s respondents say they aren’t concerned about staffing their projects this year, Consigli suggests they need to monitor their workforce resources for 2022, based on the amount of work in the pipeline.

PRICING AND SUPPLY ARE ISSUES FOR SEVERAL PRODUCT

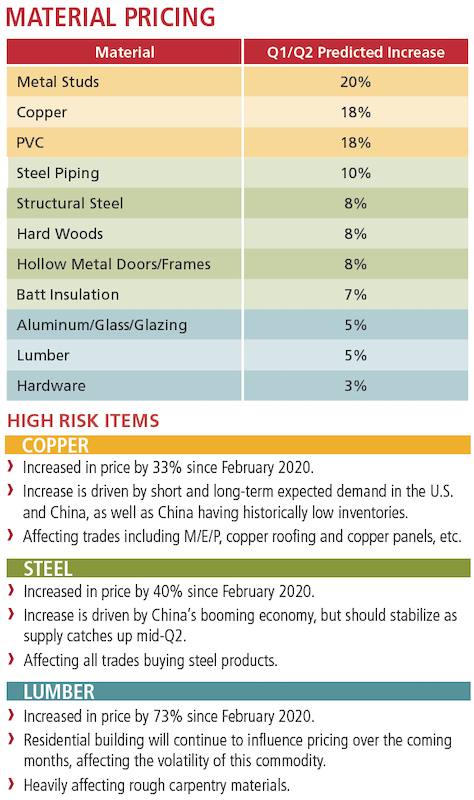

The Market Outlook expects copper and steel to manifest the greatest risk for price inflation. Chart: Consigli Construction

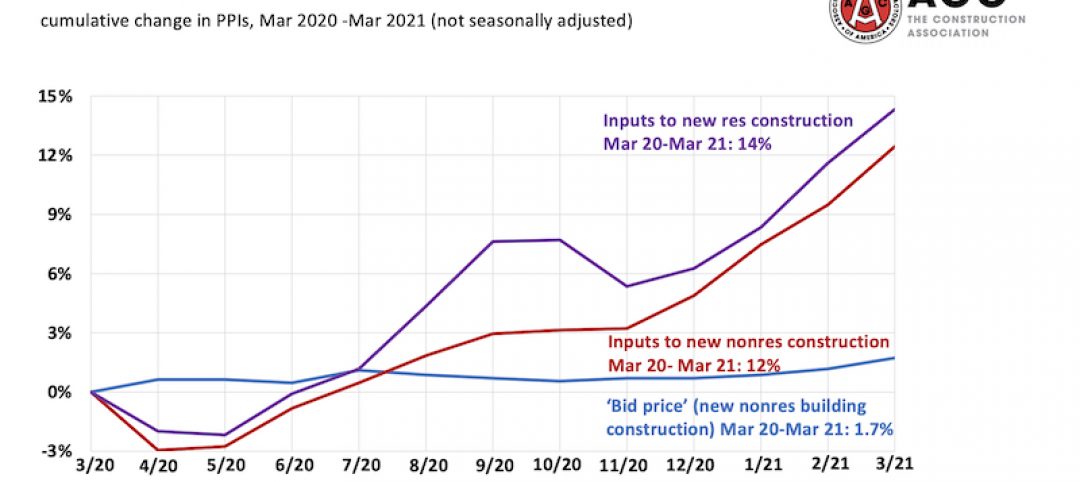

The Market Outlook Report also looks at materials price inflation in several product categories (see chart). Metal studs, copper, and PVC are the materials that the report expects to show the greatest price increases in the first half of the year. The report also suggests that lumber—whose pricing had jumped by 73% since February 2020—could be stabilizing, depending on residential demand.

(The Commerce Department reported last week that housing starts had surged to a nearly 15-year high in March.)

Consigli recommends that subs keep a close eye on high-risk materials, and lock in prices as soon as possible to avoid exposure to inflation. Subs should also watch for supply-chain disruptions, especially for products coming from overseas like flooring and cabinetry. Where possible, have access to alternate materials and delivery options.

Related Stories

Market Data | Apr 16, 2021

Construction employment in March trails March 2020 mark in 35 states

Nonresidential projects lag despite hot homebuilding market.

Market Data | Apr 13, 2021

ABC’s Construction Backlog slips in March; Contractor optimism continues to improve

The Construction Backlog Indicator fell to 7.8 months in March.

Market Data | Apr 9, 2021

Record jump in materials prices and supply chain distributions threaten construction firms' ability to complete vital nonresidential projects

A government index that measures the selling price for goods used construction jumped 3.5% from February to March.

Contractors | Apr 9, 2021

Construction bidding activity ticks up in February

The Blue Book Network's Velocity Index measures month-to-month changes in bidding activity among construction firms across five building sectors and in all 50 states.

Industry Research | Apr 9, 2021

BD+C exclusive research: What building owners want from AEC firms

BD+C’s first-ever owners’ survey finds them focused on improving buildings’ performance for higher investment returns.

Market Data | Apr 7, 2021

Construction employment drops in 236 metro areas between February 2020 and February 2021

Houston-The Woodlands-Sugar Land and Odessa, Texas have worst 12-month employment losses.

Market Data | Apr 2, 2021

Nonresidential construction spending down 1.3% in February, says ABC

On a monthly basis, spending was down in 13 of 16 nonresidential subcategories.

Market Data | Apr 1, 2021

Construction spending slips in February

Shrinking demand, soaring costs, and supply delays threaten project completion dates and finances.

Market Data | Mar 26, 2021

Construction employment in February trails pre-pandemic level in 44 states

Soaring costs, supply-chain problems jeopardize future jobs.

Market Data | Mar 24, 2021

Architecture billings climb into positive territory after a year of monthly declines

AIA’s ABI score for February was 53.3 compared to 44.9 in January.