The cost of goods and services used in construction accelerated further in April as more items logged double-digit increases over the past year, according to an analysis by the Associated General Contractors of America of government data released today. Meanwhile, nonresidential contractors struggled with delays in receiving materials and intensifying competition that limited their ability to pass on higher costs. Association officials urged the Biden administration to quickly roll back tariffs and quotas on imported construction materials that are adding to costs and availability problems.

“Today’s producer price index report—bad though it is—actually understates the severity of the problems contractors are experiencing,” said Ken Simonson, the association’s chief economist. “Many items have posted even steeper price increases since the data for this report were collected in mid-April, while lead times for producing goods and delivery times to distributors and worksites have grown ever longer and less certain.”

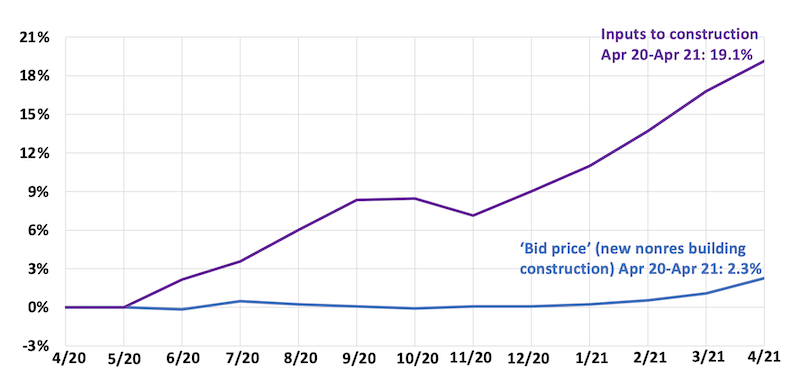

Prices for materials used in construction jumped 19.7% from April 2020 to last month. That was by far the largest increase in the 35-year history of the series, Simonson said. A series that includes services as well as goods purchased by contractors increased nearly as much, 19.1%. Meanwhile, the producer price index for new nonresidential construction—a measure of what contractors say they would charge to erect five types of nonresidential buildings—rose only 2.3% over the past 12 months, as competition for a shrinking pool of new projects forced contractors to absorb most of the increases.

Items with especially steep price increases over the past year ranged from lumber to metals to plastics. The producer price index for lumber and plywood soared 85.7% from April 2020 to last month. The index for steel mill products climbed 67%, while the index for copper and brass mill shapes rose 49% and the index for aluminum mill shapes increased 20.5%. The index for plastic construction products rose 14.2% amid growing scarcity of items such as PVC pipe, vinyl siding and moisture barriers, and resins used in paints and adhesives. The index for gypsum products such as wallboard climbed 12.1%.

Association officials said some of the supply chain problems have resulted from the pandemic or one-time events like the freeze in Texas last February that damaged plants producing inputs for construction plastics. But they added that federal policies, particularly tariffs and quotas on key building materials like lumber, steel, and aluminum have exacerbated the price spikes, supply shortages, and delivery delays. They urged the administration to end those import obstacles and explore ways to help uncork supply-chain bottlenecks.

“The Biden administration must address these unprecedented lumber and steel costs and broader supply-chain woes or risk undermining the economic recovery,” said Stephen E. Sandherr, the association’s chief executive officer. “Without tariff relief and other measures, vital construction projects will fall behind schedule or be canceled.”

View producer price index data. View chart of gap between input costs and bid prices. View AGC’s Construction Inflation Alert.

Related Stories

K-12 Schools | Feb 29, 2024

Average age of U.S. school buildings is just under 50 years

The average age of a main instructional school building in the United States is 49 years, according to a survey by the National Center for Education Statistics (NCES). About 38% of schools were built before 1970. Roughly half of the schools surveyed have undergone a major building renovation or addition.

MFPRO+ Research | Feb 27, 2024

Most competitive rental markets of early 2024

The U.S. rental market in early 2024 is moderately competitive, with apartments taking an average of 41 days to find tenants, according to the latest RentCafe Market Competitivity Report.

Construction Costs | Feb 22, 2024

K-12 school construction costs for 2024

Data from Gordian breaks down the average cost per square foot for four different types of K-12 school buildings (elementary schools, junior high schools, high schools, and vocational schools) across 10 U.S. cities.

Student Housing | Feb 21, 2024

Student housing preleasing continues to grow at record pace

Student housing preleasing continues to be robust even as rent growth has decelerated, according to the latest Yardi Matrix National Student Housing Report.

Architects | Feb 21, 2024

Architecture Billings Index remains in 'declining billings' state in January 2024

Architecture firm billings remained soft entering into 2024, with an AIA/Deltek Architecture Billings Index (ABI) score of 46.2 in January. Any score below 50.0 indicates decreasing business conditions.

Multifamily Housing | Feb 14, 2024

Multifamily rent remains flat at $1,710 in January

The multifamily market was stable at the start of 2024, despite the pressure of a supply boom in some markets, according to the latest Yardi Matrix National Multifamily Report.

Student Housing | Feb 13, 2024

Student housing market expected to improve in 2024

The past year has brought tough times for student housing investment sales due to unfavorable debt markets. However, 2024 offers a brighter outlook if debt conditions improve as predicted.

Contractors | Feb 13, 2024

The average U.S. contractor has 8.4 months worth of construction work in the pipeline, as of January 2024

Associated Builders and Contractors reported today that its Construction Backlog Indicator declined to 8.4 months in January, according to an ABC member survey conducted from Jan. 22 to Feb. 4. The reading is down 0.6 months from January 2023.

Industry Research | Feb 8, 2024

New multifamily development in 2023 exceeded expectations

Despite a problematic financing environment, 2023 multifamily construction starts held up “remarkably well” according to the latest Yardi Matrix report.

Market Data | Feb 7, 2024

New download: BD+C's February 2024 Market Intelligence Report

Building Design+Construction's monthly Market Intelligence Report offers a snapshot of the health of the U.S. building construction industry, including the commercial, multifamily, institutional, and industrial building sectors. This report tracks the latest metrics related to construction spending, demand for design services, contractor backlogs, and material price trends.