As seen in the Lodging Econometrics (LE) Q4'21 United States Construction Pipeline Trend Report, the franchise companies with the largest U.S. construction pipelines at year-end 2021 are Marriott International with 1,345 projects/170,586 rooms, followed by Hilton Worldwide with 1,239 projects/141,053 rooms, and InterContinental Hotels Group (IHG) with 761 projects/76,987 rooms. These three companies combined account for 69% of the projects and 67% of the rooms in the total U.S. construction pipeline.

At the end of Q4'21, over 56% of Hilton’s projects in the pipeline are in the early planning project stage, a record-high by projects in this stage for the company, with 689 projects/76,058 rooms. Hilton has 228 projects/29,036 under construction at Q4 and 322 projects/35,959 rooms scheduled to start within the next 12 months. Marriott also hit a record high for both projects and rooms in early planning at the end of the fourth quarter, with 534 projects/63,120 rooms. Marriott has 262 projects, accounting for 38,289 rooms under construction at the end of Q4 and 549 projects/69,177 rooms are scheduled to start in the next 12 months. IHG currently has 121 projects, accounting for 11,376 rooms, in the early planning stage. 136 projects, with 16,221 rooms, in IHG’s pipeline, are in the under construction stage while 504 projects/49,390 rooms are scheduled to start within the next 12 months.

The leading brands by project count for the top three franchise companies continue to be Hilton’s Home2 Suites by Hilton with 421 projects/43,824 rooms, IHG’s Holiday Inn Express with 288 projects/27,620 rooms, and Marriott’s Fairfield Inn with 247 projects/23,344 rooms. These three brands dominate the pipeline and combined claim 20% of the projects.

Other notable brands in the pipeline for the top franchise companies at Q4 are Marriott’s TownePlace Suites with 239 projects/22,759 rooms and Residence Inn with 212 projects/25,896 rooms; Hilton’s Tru by Hilton brand with 222 projects/21,222 rooms and the Hampton by Hilton brand with 267 projects/27,577 rooms; and IHG’s Avid Hotel with 148 projects/12,885 rooms and Staybridge Suites with 124 projects/12,734 rooms.

Through year-end 2021, Marriott, Hilton, and IHG branded hotels represented 585 new hotel openings with 73,415 rooms. 201 of the hotels were Hilton brands, 267 were Marriott brands, and another 117 were IHG brands. The LE forecast for new hotel openings in 2022 anticipates that Marriott will open 207 projects/27,258 rooms, for a growth rate of 3.1%. Next is Hilton with 165 projects/18,764 rooms, for a growth rate of 2.5%, followed by IHG with 115 projects/12,397 rooms forecast to open for a growth rate of 2.9%. In 2023, Marriot is expected to open another 211 projects/25,056 rooms for a growth rate of 2.7%. LE predicts Hilton will open 173 projects/21,450 rooms, for a 2.8% growth rate by year-end 2023, while IHG is expected to see a 3.4% growth rate in 2023, with 148 new hotel projects, accounting for 15,146 rooms.

Related Stories

Market Data | Apr 16, 2021

Construction employment in March trails March 2020 mark in 35 states

Nonresidential projects lag despite hot homebuilding market.

Market Data | Apr 13, 2021

ABC’s Construction Backlog slips in March; Contractor optimism continues to improve

The Construction Backlog Indicator fell to 7.8 months in March.

Market Data | Apr 9, 2021

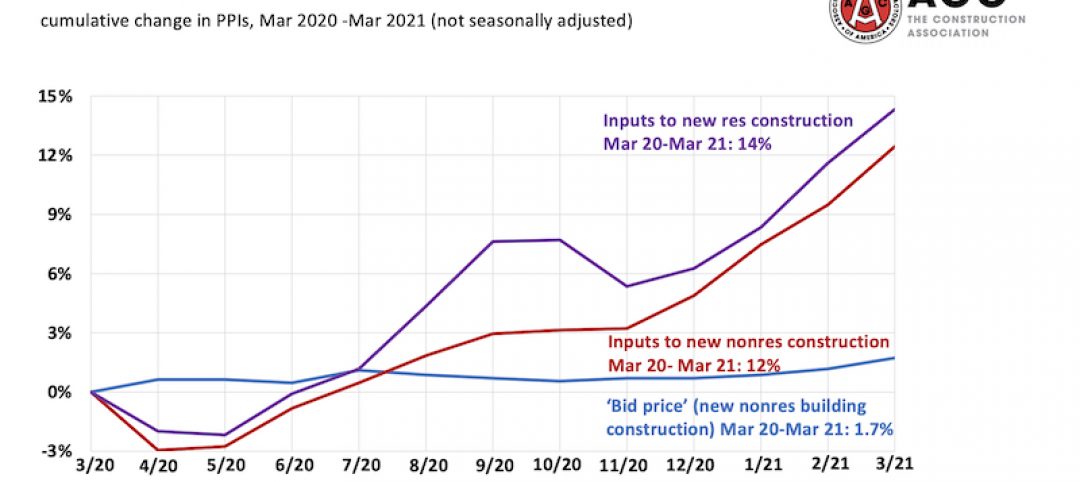

Record jump in materials prices and supply chain distributions threaten construction firms' ability to complete vital nonresidential projects

A government index that measures the selling price for goods used construction jumped 3.5% from February to March.

Contractors | Apr 9, 2021

Construction bidding activity ticks up in February

The Blue Book Network's Velocity Index measures month-to-month changes in bidding activity among construction firms across five building sectors and in all 50 states.

Industry Research | Apr 9, 2021

BD+C exclusive research: What building owners want from AEC firms

BD+C’s first-ever owners’ survey finds them focused on improving buildings’ performance for higher investment returns.

Market Data | Apr 7, 2021

Construction employment drops in 236 metro areas between February 2020 and February 2021

Houston-The Woodlands-Sugar Land and Odessa, Texas have worst 12-month employment losses.

Market Data | Apr 2, 2021

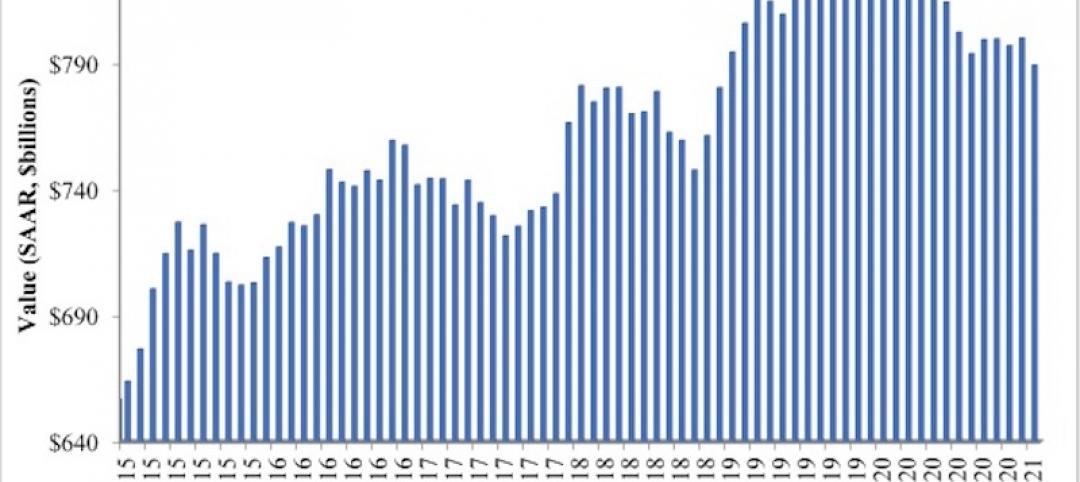

Nonresidential construction spending down 1.3% in February, says ABC

On a monthly basis, spending was down in 13 of 16 nonresidential subcategories.

Market Data | Apr 1, 2021

Construction spending slips in February

Shrinking demand, soaring costs, and supply delays threaten project completion dates and finances.

Market Data | Mar 26, 2021

Construction employment in February trails pre-pandemic level in 44 states

Soaring costs, supply-chain problems jeopardize future jobs.

Market Data | Mar 24, 2021

Architecture billings climb into positive territory after a year of monthly declines

AIA’s ABI score for February was 53.3 compared to 44.9 in January.