The current record-setting expansion in the U.S. economy and its real estate sector, which dates back to the start of this decade, should continue through 2021, but at a moderated pace.

That’s the consensus prediction, based on a recent survey of 41 economists and analysts at 32 leading real estate organizations. Those experts’ opinions about all things real estate—from transaction volumes and pricing to returns on investment and housing development—form the basis of the Urban Land Institute’s Real Estate Economic Forecast, which ULI released last week.

The trends that are likely to drive the pace of that growth are identified in Emerging Trends in Real Estate 2020, which ULI and PwC, the accounting and research firm, released last month. That 92-page report is based on survey responses from 1,450 people working for various real estate-related businesses (nearly 28% of whom are private property owners or developers), and 750 individuals whom the report’s researchers interviewed personally.

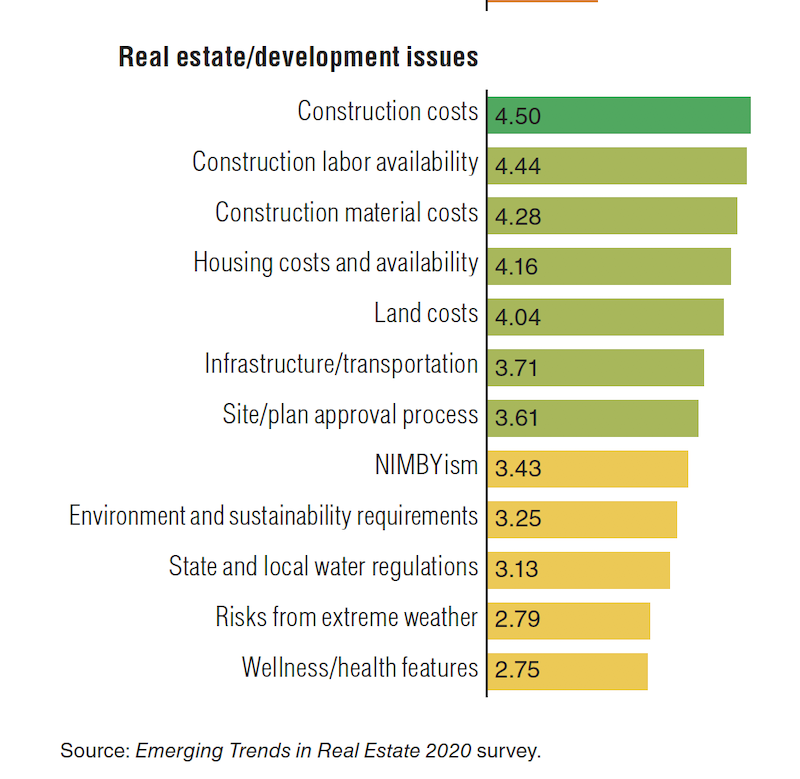

Rising construction costs lead the areas of concern that could stymie real estate growth.

Austin ranks first out of 80 metros in the U.S. for having the greatest potential for real estate for 2020, followed by Raleigh-Durham, N.C., Nashville, Charlotte, and Boston. The Emerging Trends report assesses which markets are worth watching by six criteria that include population projections, homebuilding prospects, investor demand, and redevelopment opportunities.

Manhattan and Chicago will continue to lead the pack as capital magnets for real estate investment. Philadelphia and Long Island, N.Y., are among the metros with sustained track records for capital flow and transaction volume. And Jacksonville, Fla., Salt Lake City, and Columbus, Ohio, are deemed “treasures ripe for discovery.”

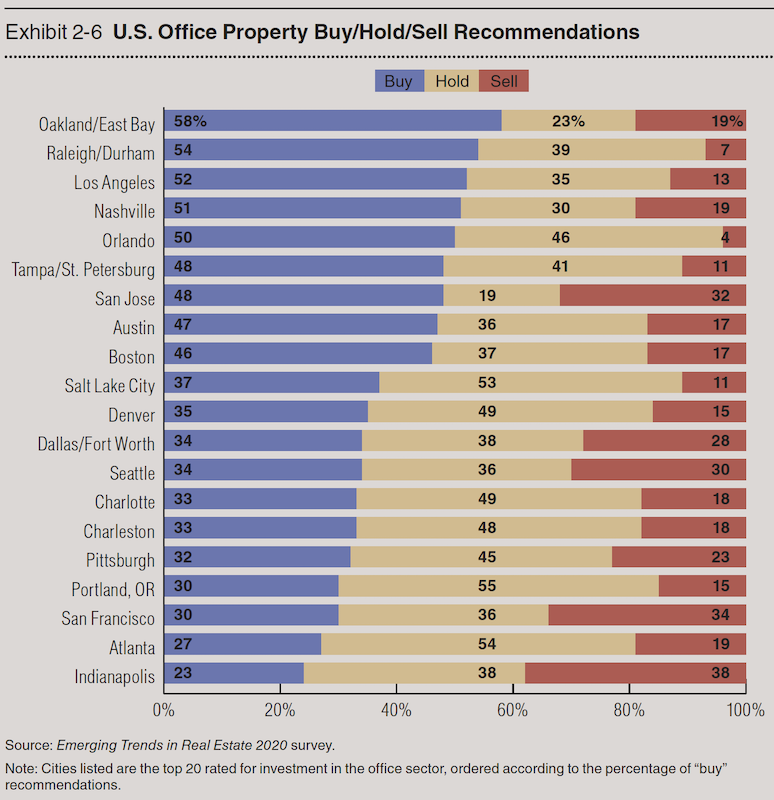

The report makes “buy-hold-sell” recommendations within metros for different building types. For example, nearly three-fifths of respondents gave Oakland/East Bay in California a “buy” recommendation for office properties. Orlando ranked highest for multifamily properties, Nashville for retail, Charleston, S.C., for hotels.

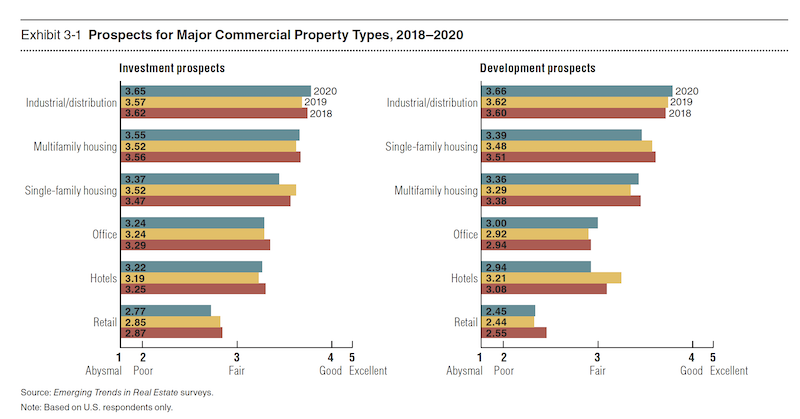

Warehouse distribution, in an era of online shopping, continues to be seen as fertlle for future development.

Nationally, industrial buildings, such as warehouses, have the greatest prospects among commercial real estate property types for 2020 in terms of their return performance and growth outlook, followed by multi- and single-family housing.

This report, though, isn’t all upbeat. Among the trends it spots is an “extended downshifting” in the economy, which is likely to have implications for commercial property demand “in the decades ahead.” The report warns against “a surfeit of capital desperately seeking placement,” which could create a real estate bubble. And the repot sees affordable housing at “a breaking point” of inadequate supply. One attempted solution: the rise in coliving.

The report sees increasing demand for communities that can deliver an authentic sense of place “rather than concocted through prescribed programming and business goals.” It also sees live-work-play districts breaking out of their urban enclaves and expanding to suburban communities to create “hipsturbias.” Real estate development in “hipsturbs” and urban downtowns should benefit from baby boomers’ expectations of staying active as they age.

Infrastructure construction and improvement are more likely to be initiated by state and local, rather than federal, governments that see them as foundations of their cities’ economic growth. And property managers are turning to technology for productivity enhancements and operational efficiencies.

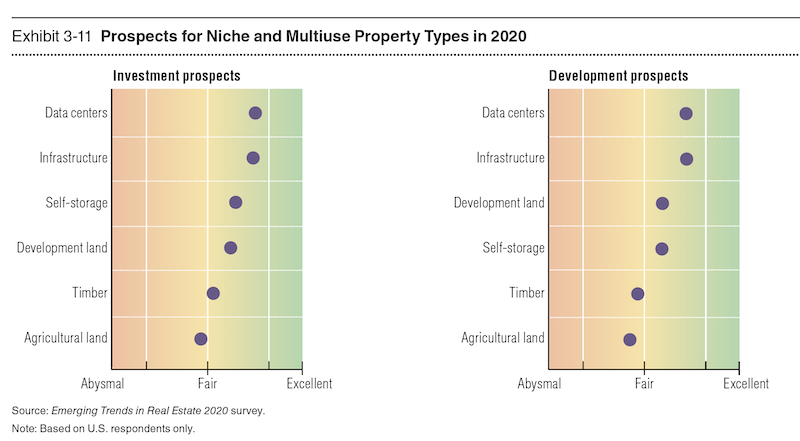

Data centers and infrastructure are two building types where experts foresee better than average growth prospects.

Many of these trends are premised on economic assumptions that ULI lays out in its Real Estate Economic Forecast. It expects the U.S. gross domestic product to increase by 2.3% this year 1.7% next year, and 1.9% in 2021. Net job growth should average 1.7 million per year through 2021. Yields on 10-year U.S. Treasury notes are expected to decline, which ULI states “should be a positive for real estate values.”

Real estate transaction volumes are expected to moderate over the forecast period, from a projected $475 billion this year to $415 billion in 2021. Real estate price growth is also expected to slow, from 5.1% this year to 3.9% in 2021.

The Oakland, Calif., market remains ripe for office development and construction.

Rent growth should be flat for all building types except industrial and hotels, which will see declines. National vacancy rates will rise slightly, predicts economists.

Total real estate returns, as well as equity real estate investment trust returns, are expected to be strong over the next two years. On the flip side, increasing construction costs are tamping down single-family housing, to the point where ULI’s report is forecasting an annual average, through 2021, of between 800,000 and 850,000 units delivered, well below the long-term annual average of 975,000. Home prices, though, should continue to average 3.2% growth per year over the forecast period.

Related Stories

Market Data | Jun 21, 2017

Design billings maintain solid footing, strong momentum reflected in project inquiries/design contracts

Balanced growth results in billings gains in all sectors.

Market Data | Jun 16, 2017

Residential construction was strong, but not enough, in 2016

The Joint Center for Housing Studies’ latest report expects minorities and millennials to account for the lion’s share of household formations through 2035.

Industry Research | Jun 15, 2017

Commercial Construction Index indicates high revenue and employment expectations for 2017

USG Corporation (USG) and U.S. Chamber of Commerce release survey results gauging confidence among industry leaders.

Market Data | Jun 2, 2017

Nonresidential construction spending falls in 13 of 16 segments in April

Nonresidential construction spending fell 1.7% in April 2017, totaling $696.3 billion on a seasonally adjusted, annualized basis, according to analysis of U.S. Census Bureau data released today by Associated Builders and Contractors.

Industry Research | May 25, 2017

Project labor agreement mandates inflate cost of construction 13%

Ohio schools built under government-mandated project labor agreements (PLAs) cost 13.12 percent more than schools that were bid and constructed through fair and open competition.

Market Data | May 24, 2017

Design billings increasing entering height of construction season

All regions report positive business conditions.

Market Data | May 24, 2017

The top franchise companies in the construction pipeline

3 franchise companies comprise 65% of all rooms in the Total Pipeline.

Industry Research | May 24, 2017

These buildings paid the highest property taxes in 2016

Office buildings dominate the list, but a residential community climbed as high as number two on the list.

Market Data | May 16, 2017

Construction firms add 5,000 jobs in April

Unemployment down to 4.4%; Specialty trade jobs dip slightly.

Multifamily Housing | May 10, 2017

May 2017 National Apartment Report

Median one-bedroom rent rose to $1,012 in April, the highest it has been since January.