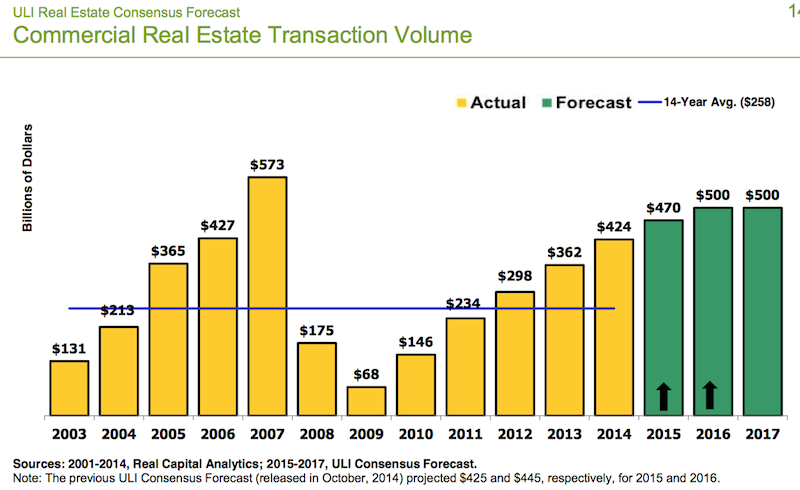

Driven by sparser availability of warehouses, offices, and retail, the real estate industry is positioned for solid growth this year and next, before tapering off at a still-respectable $500 billion in annual transactions in 2017.

Those predictions highlight Urban Land Institute’s (ULI) latest three-year Real Estate Consensus Forecast, based on the median of forecasts from 46 economists and analysts at 33 leading real estate organizations, who were surveyed from February 27 through March 23.

The expert consensus projects an 18% increase, to $470 billion, in commercial real estate transactions for 2015, followed by a 6.4%, to $500 billion, in 2016.

ULI’s forecast is more optimistic for the years 2015 and 2016 than previous forecasts for all indicators except single-family home starts.

The experts’ optimism stems, in part, from their predictions for healthy GDP growth, which they expect to rise by 3% this year and next, and by 2.8% in 2017. If realized, those would be the highest annual growth rates in nine years.

In addition, the U.S. economy has been experiencing its highest rate of job growth in 15 years. “For real estate, it’s really about jobs,” says William Maher, a director with LaSalle Investment Management, who analyzed the results of the survey for ULI.

The Consensus Forecast provides oultooks for specific construction segments:

• Institutional real estate assets are expected to provide total returns across all sectors of 11% in 2015, moderating to 10% in 2016 and 9% in 2017. By property type, returns should be strongest for industrial and office, followed by retail and apartments, in all three years.

• Vacancy rates are expected to decrease modestly for office and retail over all three forecast years. Industrial availability rates and hotel occupancy rate are forecasted to improve modestly in 2015 and 2016 and level off in 2017. Apartment vacancy rates are expected to begin rising slightly to 4.7% in 2015, 5% in 2016, and 5.3% in 2017. The 2017 forecast is just below the 20-year average vacancy rate.

• CRBE estimated that the availability rate for the industrial/warehouse sector declined to 10.3% at the end of 2014, coming in just below the 20-year average for the first time since 2007. ULI Consensus Forecast predicts availability rates will continue to decline in 2015 and 2016, with year-end vacancy rates at 9.8% and 9.6%, respectively, and remain steady in 2017 at 9.6%. Consequently, warehouse rental rate growth should continue, by 4% in 2015, 3.8% in 2016, and 3.1% in 2017, all above the 20-year average growth rate.

• The same pattern can be found in office vacancy rates, which declined for the fourth straight year, to 13.9% in 2014. That pattern is expected to continue through 2017, sparking further appreciation in office rental rates, which according the Consensus Forecast will increase by 4% in 2015 and 4.1% in 2016. Rental rate growth is expected to moderate slightly in 2017 to 3.5%.

• The Consensus foresees improvements in retail availability. And with rents increasing in 2014 for the first time in six years, the Consensus Forecast expects rental rates to sustain this growth, increasing by 2% in 2015, 3% in 2016, and 2.9% 2017.

ULI will release its next Consensus Forecast in October.

Related Stories

| Sep 3, 2014

New designation launched to streamline LEED review process

The LEED Proven Provider designation is designed to minimize the need for additional work during the project review process.

| Sep 2, 2014

Ranked: Top green building sector AEC firms [2014 Giants 300 Report]

AECOM, Gensler, and Turner top BD+C's rankings of the nation's largest green design and construction firms.

and Callison (guest rooms).")

| Aug 21, 2014

RTKL's parent company Arcadis acquires Callison

The acquisition of Callison, known predominantly for its leadership in retail and mixed-use design, builds on Arcadis’ strong global design and architecture position, currently provided by RTKL.

| Aug 19, 2014

Goettsch Partners unveils design for mega mixed-use development in Shenzhen [slideshow]

The overall design concept is of a complex of textured buildings that would differentiate from the surrounding blue-glass buildings of Shenzhen.

| Aug 18, 2014

From icon to breadbasket: Gehry building to be turned into Whole Foods

The Howard Hughes Corporation, in association with architecture firm Cho Benn Holback + Associates, plans to turn the building—at least the majority of it—into a Whole Foods.

| Aug 18, 2014

SPARK’s newly unveiled mixed-use development references China's flowing hillscape

Architecture firm SPARK recently finished a design for a new development in Shenzhen. The 770,700 square-foot mixed-use structure's design mimics the hilly landscape of the site's locale.

| Aug 11, 2014

The Endless City: Skyscraper concept connects all floors with dual ramps

Rather than superimposing one floor on top of another, London-based SURE Architecture proposes two endless ramps, rising gradually with a low gradient from the ground floor to the sky.

| Aug 4, 2014

Retail Giants: Grocery-anchored centers, trophy malls among hot retail developments [2014 Giants 300 Report]

Despite the rapid growth of online shopping, the 'bricks and mortar' retail sector is faring quite well, headed by power centers, grocery-anchored centers, and trophy malls, according BD+C's 2014 Giants 300 Report.

| Jul 28, 2014

Reconstruction market benefits from improving economy, new technology [2014 Giants 300 Report]

Following years of fairly lackluster demand for commercial property remodeling, reconstruction revenue is improving, according to the 2014 Giants 300 report.

| Jul 28, 2014

Reconstruction Sector Construction Firms [2014 Giants 300 Report]

Structure Tone, Turner, and Gilbane top Building Design+Construction's 2014 ranking of the largest reconstruction contractor and construction management firms in the U.S.