ConstructConnect, a provider of construction information and technology solutions in North America, recently announced the release of its Q4 2017 Forecast Quarterly Report. The Winter 2017-18 starts forecast includes year-over-year estimates for 2017 that have become more upbeat than a quarter ago. Groundbreakings on several mega projects late this year have provided exceptional lift to the industrial and engineering type-of-structure categories.

“Out to 2021, residential will be the main driver of total construction starts, recording year-over-year increases of nearly +6.0% or more,” explained Chief Economist Alex Carrick. “Non-residential building will disappoint, with gains of only about +2.0% each year. Engineering will be strong in 2018 and 2019, as energy initiatives and infrastructure work are promoted by Washington, but will then moderate in 2020-21.”

The forecast which combines ConstructConnect's proprietary data with macroeconomic factors and Oxford Economics econometric expertise, shows some of the more robust 2018 starts forecasts:

- Single-family residential, +8.8%

- Warehouses, +4.7%

- Nursing homes, +5.9%

- Educational facilities, +4.2%

- Roads, +5.9%

- Bridges, +10.2%

- Miscellaneous civil (power, oil and gas), +13.8%

2017 total starts are now expected to be +7.9% (versus an earlier calculated +4.5%). Residential has been upgraded to +10.1% and engineering/civil to +23.1%. Non-residential building has been left essentially flat at -0.5%.

For 2018, the new forecasts shave a bit off what was previously expected. Total starts are now projected to be +4.8%, a little slower than the +5.9% of a quarter ago. Residential will be +6.7% in 2018; non-res building, +1.9%; and heavy engineering/civil, +6.6%.

In residential construction, the multi-family market has had its turn and it will be the single-family market that will expand more rapidly moving forward, aided by family-formations among the millennial generation.

The forecast reports that educational facilities will grow faster than hospitals in 2018, but beginning in 2019 their positions will reverse. Some other non-residential building type-of-structure categories with bullish outlooks include: courthouses and prisons; warehouses; and nursing homes. Airports and sports stadiums will also be stepping into the construction spotlight.

The report noted a few ongoing economic trends:

- A synchronous world expansion is underway, with North America, Japan, China and Europe all experiencing GDP growth

- Based on demographics, housing starts have fallen short of potential for almost a decade

- Office space demand will increasingly come from firms engaged in high-tech

- Prices for many internationally traded commodities are on the mend

To learn more about ConstructConnect or get a free copy of the Forecast Quarterly Report, visit constructconnect.com.

Related Stories

Market Data | Jul 19, 2021

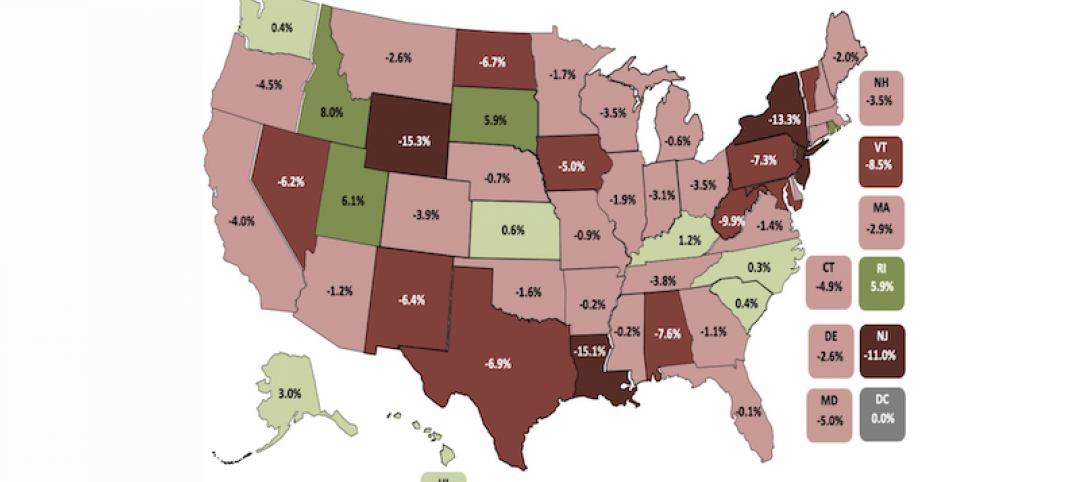

Construction employment trails pre-pandemic level in 39 states

Supply chain challenges, rising materials prices undermine demand.

Market Data | Jul 15, 2021

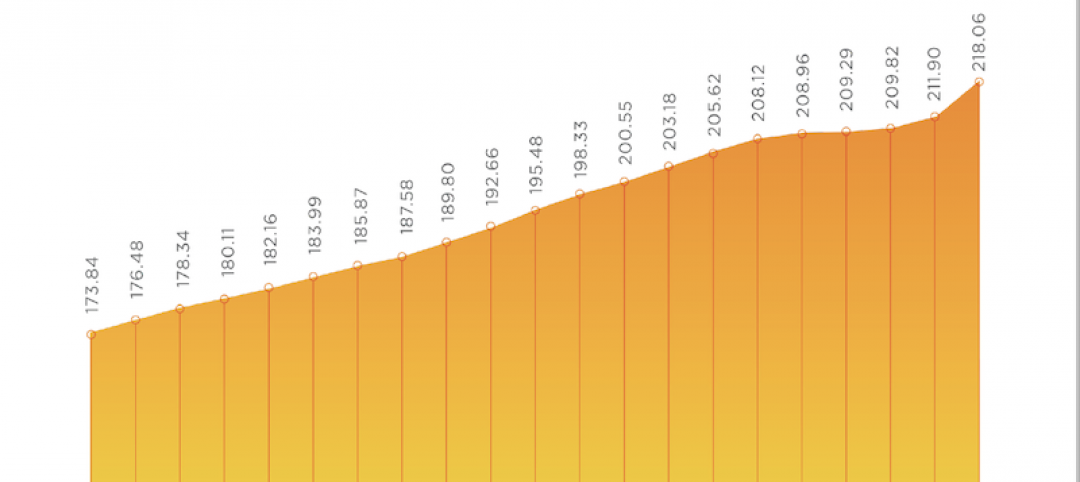

Producer prices for construction materials and services soar 26% over 12 months

Contractors cope with supply hitches, weak demand.

Market Data | Jul 13, 2021

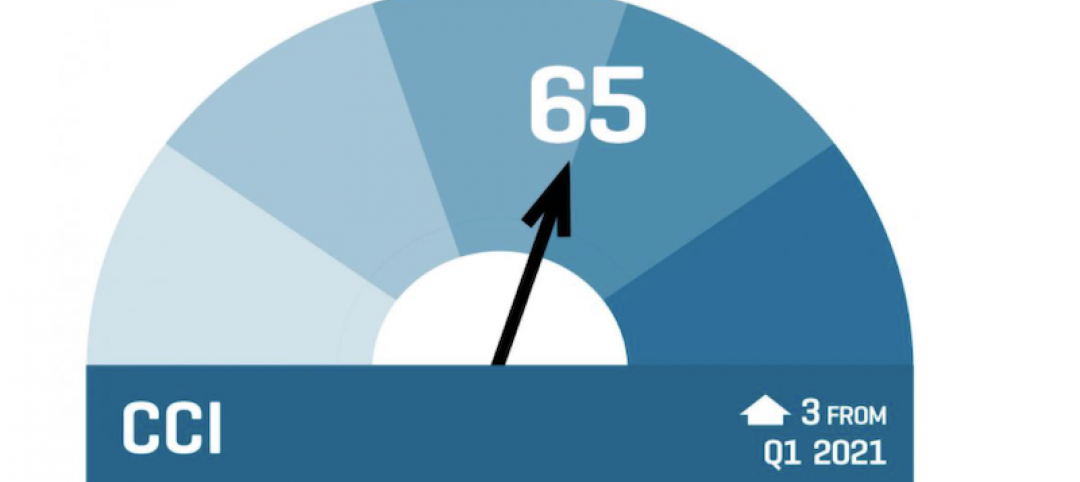

ABC’s Construction Backlog Indicator and Contractor Confidence Index rise in June

ABC’s Construction Confidence Index readings for sales, profit margins and staffing levels increased modestly in June.

Market Data | Jul 8, 2021

Encouraging construction cost trends are emerging

In its latest quarterly report, Rider Levett Bucknall states that contractors’ most critical choice will be selecting which building sectors to target.

Multifamily Housing | Jul 7, 2021

Make sure to get your multifamily amenities mix right

One of the hardest decisions multifamily developers and their design teams have to make is what mix of amenities they’re going to put into each project. A lot of squiggly factors go into that decision: the type of community, the geographic market, local recreation preferences, climate/weather conditions, physical parameters, and of course the budget. The permutations are mind-boggling.

Market Data | Jul 7, 2021

Construction employment declines by 7,000 in June

Nonresidential firms struggle to find workers and materials to complete projects.

Market Data | Jun 30, 2021

Construction employment in May trails pre-covid levels in 91 metro areas

Firms struggle to cope with materials, labor challenges.

Market Data | Jun 23, 2021

Construction employment declines in 40 states between April and May

Soaring material costs, supply-chain disruptions impede recovery.

Market Data | Jun 22, 2021

Architecture billings continue historic rebound

AIA’s Architecture Billings Index (ABI) score for May rose to 58.5 compared to 57.9 in April.

Market Data | Jun 17, 2021

Commercial construction contractors upbeat on outlook despite worsening material shortages, worker shortages

88% indicate difficulty in finding skilled workers; of those, 35% have turned down work because of it.