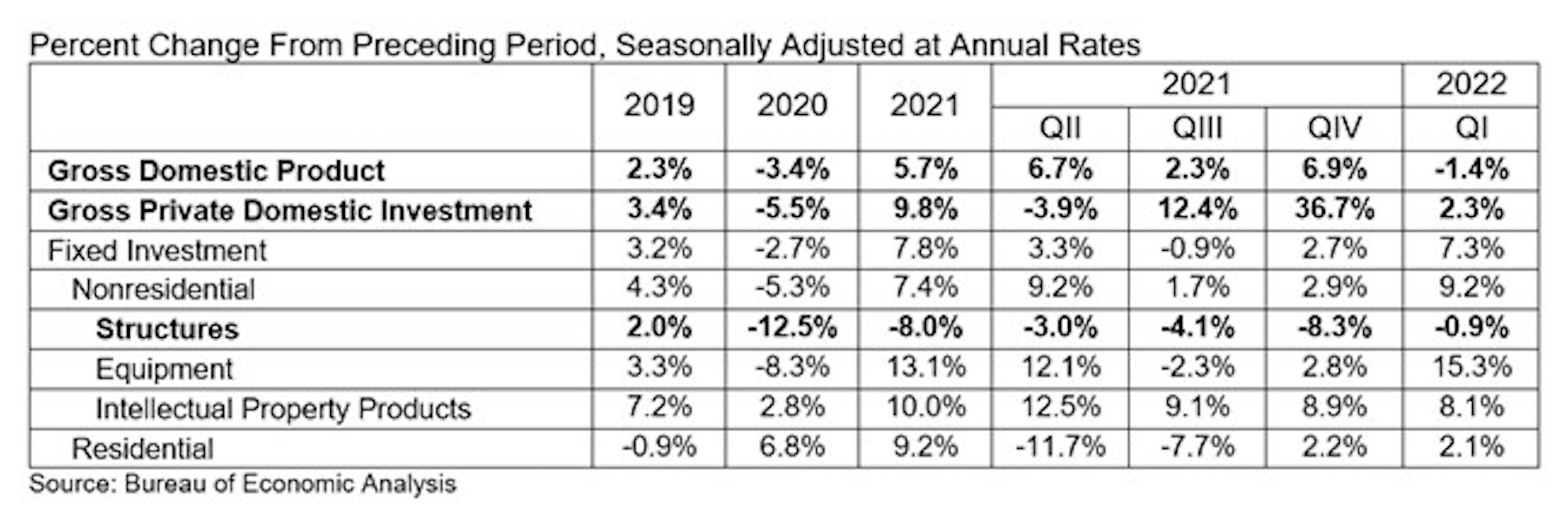

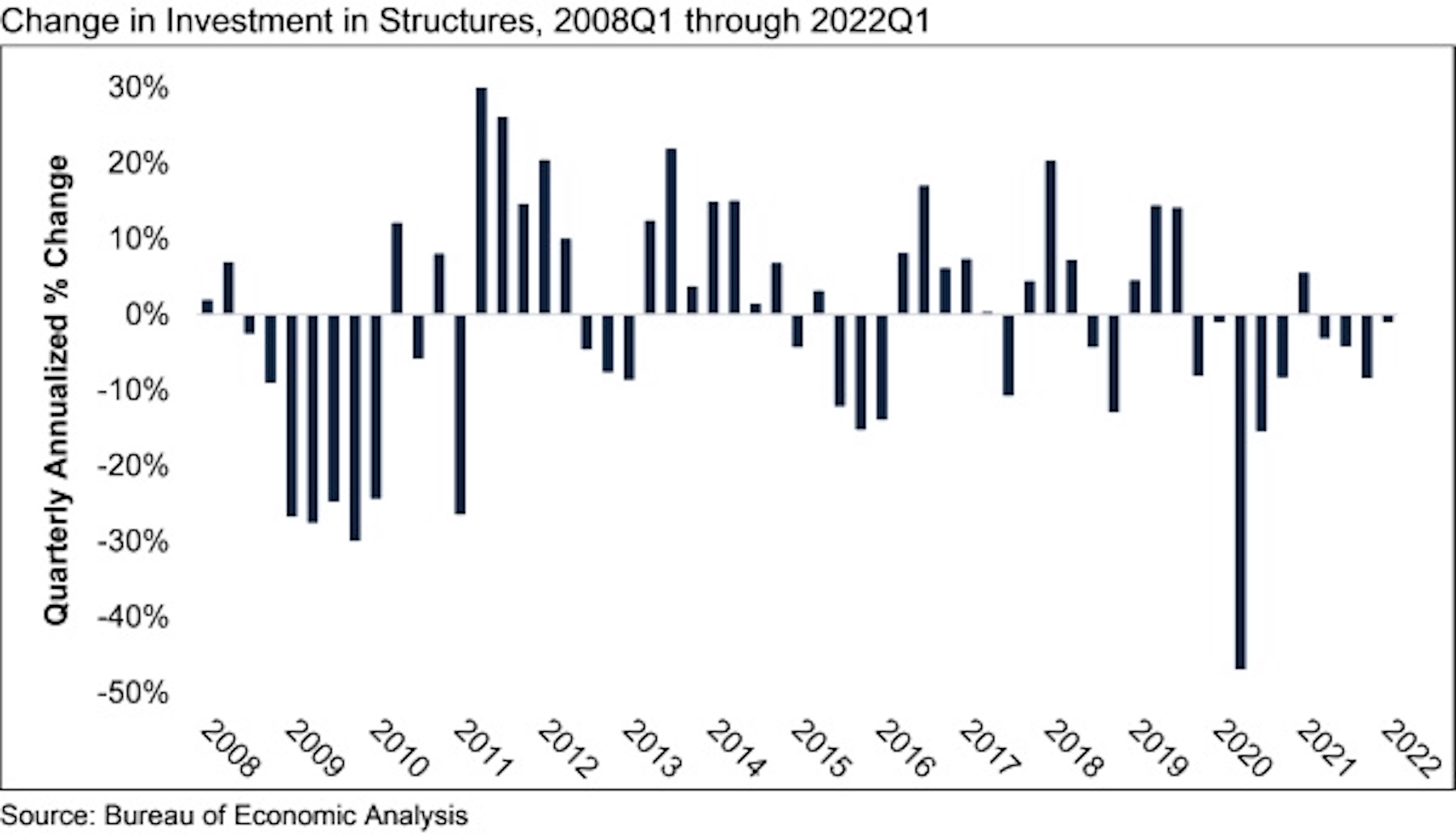

The U.S. economy contracted at a 1.4% annualized rate during the first quarter of 2022. Investment in nonresidential structures declined at an annual rate of 0.9% during the quarter and has contracted nine of the past 10 quarters, according to an Associated Builders and Contractors analysis of data released today by the U.S. Bureau of Economic Analysis.

“The economy’s woeful performance during 2022’s first quarter complicates matters,” said ABC Chief Economist Anirban Basu. “Conventional wisdom says the economy has enough momentum to contend with the tighter monetary policy the Federal Reserve is pursuing to countervail inflation. Today’s data indicate that the economy is weaker than thought, which means the Federal Reserve will have a very difficult time curbing inflation without driving the economy into recession in late 2022 or 2023.

“That said, the economy should manage to generate some positive momentum during the next two to three quarters,” said Basu. “Consumer demand for goods and services remains strong. The omicron variant affected the economy during the first quarter and that does not appear to be the case during the second. Global supply chains have been adjusting to the dislocations caused by the Russian-Ukraine war. Many state and local governments are flush with cash and continue to plan for a period of elevated infrastructure outlays.

“There is one other bit of good news,” said Basu. “The weakness exhibited by the economy during the first quarter may persuade monetary policymakers to raise interest rates less aggressively. This is a matter of significance for nonresidential contractors, who have become less confident in recent months, according to ABC’s Construction Confidence Indicator. Investment in structures continues to decline in America, in part due to weakness in office, lodging and shopping mall segments. Presumably, additional rapid increases in borrowing costs would further dampen new construction in these categories. It may be that the Federal Reserve will raise interest rates more gradually than they would have knowing that the U.S. economy is already rather fragile.”

Related Stories

Market Data | Nov 10, 2021

Construction input prices see largest monthly increase since June

Construction input prices are 21.1% higher than in October 2020.

Market Data | Nov 9, 2021

Continued increases in construction materials prices starting to drive up price of construction projects

Supply chain and labor woes continue.

Market Data | Nov 5, 2021

Construction firms add 44,000 jobs in October

Gain occurs even as firms struggle with supply chain challenges.

Market Data | Nov 3, 2021

One-fifth of metro areas lost construction jobs between September 2020 and 2021

Beaumont-Port Arthur, Texas and Sacramento--Roseville--Arden-Arcade Calif. top lists of gainers.

Market Data | Nov 2, 2021

Construction spending slumps in September

A drop in residential work projects adds to ongoing downturn in private and public nonresidential.

Hotel Facilities | Oct 28, 2021

Marriott leads with the largest U.S. hotel construction pipeline at Q3 2021 close

In the third quarter alone, Marriott opened 60 new hotels/7,882 rooms accounting for 30% of all new hotel rooms that opened in the U.S.

Hotel Facilities | Oct 28, 2021

At the end of Q3 2021, Dallas tops the U.S. hotel construction pipeline

The top 25 U.S. markets account for 33% of all pipeline projects and 37% of all rooms in the U.S. hotel construction pipeline.

Market Data | Oct 27, 2021

Only 14 states and D.C. added construction jobs since the pandemic began

Supply problems, lack of infrastructure bill undermine recovery.

Market Data | Oct 26, 2021

U.S. construction pipeline experiences highs and lows in the third quarter

Renovation and conversion pipeline activity remains steady at the end of Q3 ‘21, with conversion projects hitting a cyclical peak, and ending the quarter at 752 projects/79,024 rooms.

Market Data | Oct 19, 2021

Demand for design services continues to increase

The Architecture Billings Index (ABI) score for September was 56.6.