According to Lodging Econometrics’ (LE’s) Construction Pipeline Trend Report for the United States, the total U.S. construction pipeline stands at 4,967 projects/622,218 rooms at the end of Q1‘21. While this is a slight dip in the pipeline year-over-year (YOY), it’s not unexpected given the lockdown and travel restrictions over the past year. Further, the pipeline shows no signs of great decline compared to what occurred during the ’08 and ’09 recession. Actually, projects and rooms in the early planning stage are up significant YOY (stats on this below).

Although hotel development may still be tepid in Q1, continued government support and the extension of programs has aided many businesses to get back on their feet as more and more are working to re-staff and re-open.

To date, nearly half of the eligible population is at least partially vaccinated, leading to an ease in requirements regarding group gatherings and indoor activities. Clinical trials of vaccines for children (ages 12 to 15) have been highly effective and look very promising for another strong vaccine wave. Additionally, the CDC has announced that, so long as people continue to take COVID-19 precautions, fully vaccinated people are now safe to travel domestically. Americans are becoming more optimistic about summer travel and are making plans now. As a result, operating performance is expected to soar late this spring, summer, and fall.

At the end of Q1 ’21, projects currently under construction stand at 1,311 projects/179,304 rooms. Projects under construction continue to move towards opening. Through year-end 2020, the U.S. opened 841 projects accounting for 97,959 rooms. A total of 229 hotels/27,528 rooms opened in the first quarter of 2021. As delayed Q4 opens are coming online, LE is forecasting 691 projects/81,866 rooms to open by the end of 2021, representing a 2.0% increase in new hotel supply. For all of 2022, LE is forecasting 963 projects/111,235 rooms to open and a 2.0% supply increase.

Projects scheduled to start construction in the next 12 months total 1,866 projects/215,911 rooms. Of the 1,866 projects scheduled to begin in the next 12 months, 26.8% of these belong to extended-stay brands, a segment of the industry that developers have become increasingly interested in over the last few years. Projects in the early planning stage stand at 1,790 projects/227,003 rooms, up 10% by projects and 14% by rooms YOY.

Additionally, there were a total of 1,198 projects/190,475 rooms under renovation or conversion in the U.S. during the first quarter. This is a small decline after seeing a slight increase at the end of 2020.

Related Stories

Multifamily Housing | May 18, 2021

Multifamily housing sector sees near record proposal activity in early 2021

The multifamily sector led all housing submarkets, and was third among all 58 submarkets tracked by PSMJ in the first quarter of 2021.

Market Data | May 18, 2021

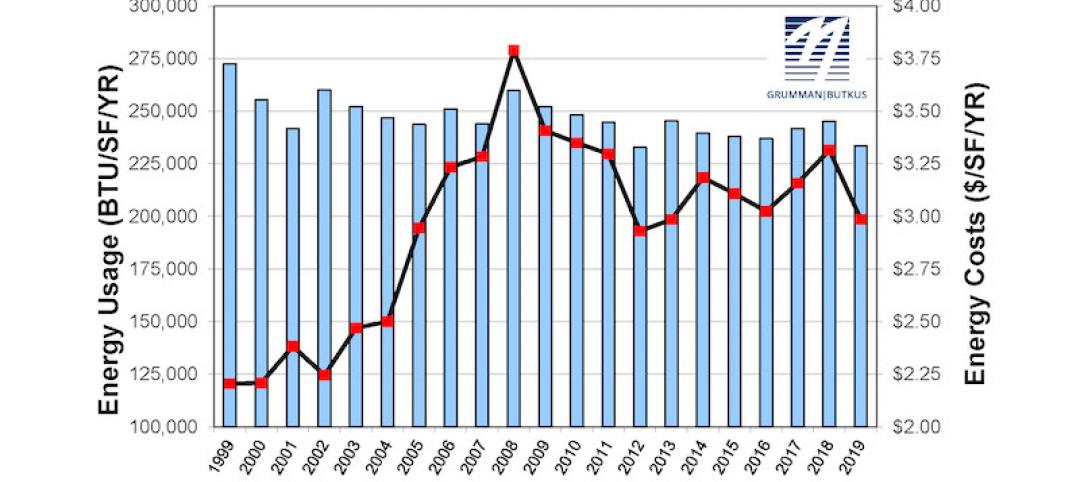

Grumman|Butkus Associates publishes 2020 edition of Hospital Benchmarking Survey

The report examines electricity, fossil fuel, water/sewer, and carbon footprint.

Market Data | May 13, 2021

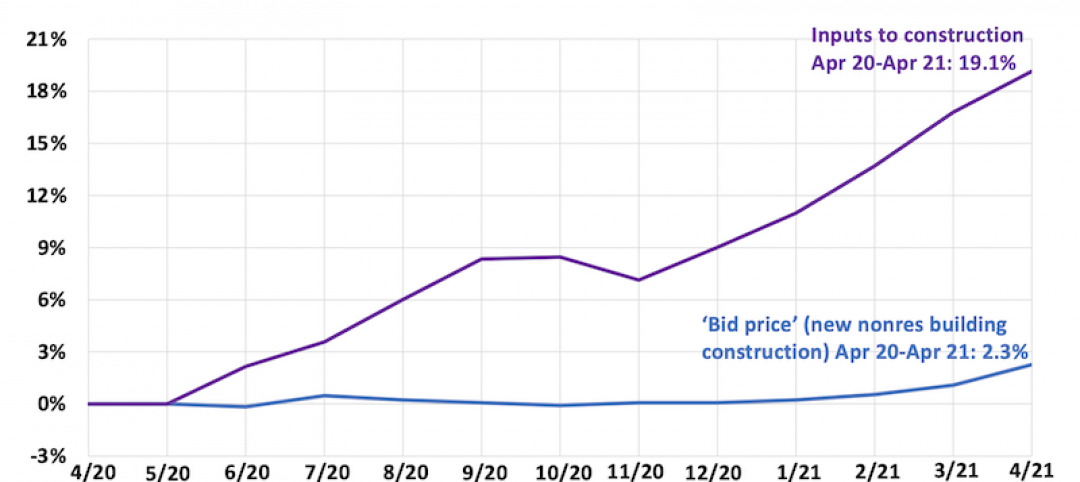

Proliferating materials price increases and supply chain disruptions squeeze contractors and threaten to undermine economic recovery

Producer price index data for April shows wide variety of materials with double-digit price increases.

Market Data | May 7, 2021

Construction employment stalls in April

Soaring costs, supply-chain challenges, and workforce shortages undermine industry's recovery.

Market Data | May 4, 2021

Nonresidential construction outlays drop in March for fourth-straight month

Weak demand, supply-chain woes make further declines likely.

Market Data | May 3, 2021

Nonresidential construction spending decreases 1.1% in March

Spending was down on a monthly basis in 11 of the 16 nonresidential subcategories.

Market Data | Apr 30, 2021

New York City market continues to lead the U.S. Construction Pipeline

New York City has the greatest number of projects under construction with 110 projects/19,457 rooms.

Market Data | Apr 28, 2021

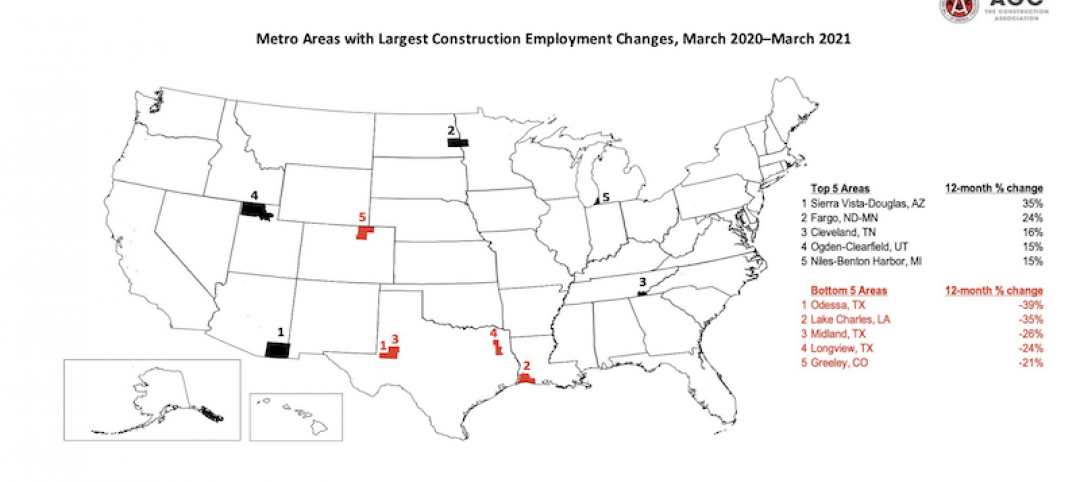

Construction employment declines in 203 metro areas from March 2020 to March 2021

The decline occurs despite homebuilding boom and improving economy.

Market Data | Apr 20, 2021

The pandemic moves subs and vendors closer to technology

Consigli’s latest market outlook identifies building products that are high risk for future price increases.

Market Data | Apr 20, 2021

Demand for design services continues to rapidly escalate

AIA’s ABI score for March rose to 55.6 compared to 53.3 in February.