At the end of the first quarter of 2020, analysts at Lodging Econometrics (LE) report that the total U.S. construction pipeline continued to expand year-over-year (YOY) to 5,731 projects/706,128 rooms, up 1% by projects and 3% by rooms. However, quarter-over-quarter, the pipeline has contracted slightly less than 1% by both project and room counts, down from 5,748 projects/708,898 rooms at the close of 2019.

Projects currently under construction stand at an all-time high of 1,819 projects/243,100 rooms. Projects scheduled to start construction in the next 12 months total 2,284 projects/264,286 rooms, while projects in the early planning stage stand at 1,628 projects/198,742 rooms. Projects in the early planning stage are up 8% by projects and 11% by rooms, YOY. Developers with projects under construction have generally extended their opening dates by two to four months. For projects scheduled to start construction in the next 12 months, on average, developers have adjusted their construction start and opening dates outwards by four to six months. Additionally, brands have been empathetic with developers by relaxing timelines as everyone adjusts to the COVID-19 interruptions. As a result, LE anticipates a stronger count of openings in the second half of 2020, compared to the first half.

In the first quarter of 2020, the U.S. opened 144 new hotels with 16,305 rooms. While the COVID-19 pandemic has slowed development, it has not completely stalled it. There were still 312 new projects with 36,464 rooms announced into the pipeline in the first quarter.

Many open or temporarily closed hotels have already begun or are in the planning stages of renovating and repositioning their assets while occupancy is low or non-existent. At the close of the first quarter, LE recorded 769 active renovation projects/163,030 rooms and 616 active conversion projects/69,258 rooms throughout the United States.

To date, the largest fiscal relief and stimulus efforts include the unprecedented $2 trillion CARES Act, the Paycheck Protection Program (PPP), and the Paycheck Protection Program Liquidity Facility (PPPLF), with a third phase of relief having been signed by the president last week. This third phase includes nearly $500 billion to further support the small-business loan program, as well as provide additional critical funding needed for hospitals and comprehensive testing. A phase four “CARES Act 2” package is already being discussed.

In order to support the economy and build liquidity, the Federal Reserve cut interest rates to almost zero; reduced bank reserve requirements to zero; rapidly purchased hundreds of billions of dollars in treasury bonds and mortgage-backed securities; bought corporate and municipal debt; and extended emergency credit to non-banks. The Federal Reserve has signaled that it will provide more support to the economy if warranted.

Although there are discussions about opening parts of the country that are beginning to stabilize; it will be measured with phased openings designed to effectively balance a highly desired economic ramp up while following prudent health and safety precautions.

*COVID-19 (coronavirus) did not have a full impact on first quarter 2020 U.S. results reported by LE. Only the last 30 days of the quarter were affected. LE’s market intelligence department has and will continue to gather the necessary global intelligence on the supply side of the lodging industry and make that information available to our subscribers. It is still early to predict the full impact of the outbreak on the lodging industry. We will have more information to report in the coming months.

Related Stories

Market Data | Oct 31, 2016

Nonresidential fixed investment expands again during solid third quarter

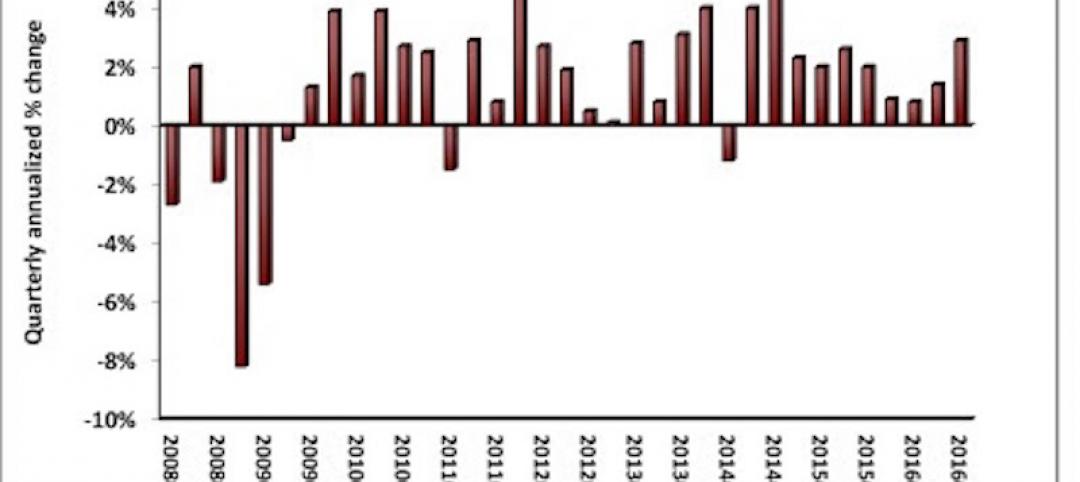

The acceleration in real GDP growth was driven by a combination of factors, including an upturn in exports, a smaller decrease in state and local government spending and an upturn in federal government spending, says ABC Chief Economist Anirban Basu.

Market Data | Oct 28, 2016

U.S. construction solid and stable in Q3 of 2016; Presidential election seen as influence on industry for 2017

Rider Levett Bucknall’s Third Quarter 2016 USA Construction Cost Report puts the complete spectrum of construction sectors and markets in perspective as it assesses the current state of the industry.

Industry Research | Oct 25, 2016

New HOK/CoreNet Global report explores impact of coworking on corporate real rstate

“Although coworking space makes up less than one percent of the world’s office space, it represents an important workforce trend and highlights the strong desire of today’s employees to have workplace choices, community and flexibility,” says Kay Sargent, Director of WorkPlace at HOK.

Market Data | Oct 24, 2016

New construction starts in 2017 to increase 5% to $713 billion

Dodge Outlook Report predicts moderate growth for most project types – single family housing, commercial and institutional building, and public works, while multifamily housing levels off and electric utilities/gas plants decline.

High-rise Construction | Oct 21, 2016

The world’s 100 tallest buildings: Which architects have designed the most?

Two firms stand well above the others when it comes to the number of tall buildings they have designed.

Market Data | Oct 19, 2016

Architecture Billings Index slips consecutive months for first time since 2012

“This recent backslide should act as a warning signal,” said AIA Chief Economist, Kermit Baker.

Market Data | Oct 11, 2016

Building design revenue topped $28 billion in 2015

Growing profitability at architecture firms has led to reinvestment and expansion

Market Data | Oct 4, 2016

Nonresidential spending slips in August

Public sector spending is declining faster than the private sector.

Industry Research | Oct 3, 2016

Structure Tone survey shows cost is still a major barrier to building green

Climate change, resilience and wellness are also growing concerns.

Industry Research | Sep 27, 2016

Sterling Risk Sentiment Index indicates risk exposure perception remains stable in construction industry

Nearly half (45%) of those polled say election year uncertainty has a negative effect on risk perception in the construction market.