At the end of the second quarter, analysts at Lodging Econometrics (LE) report that the total U.S. construction pipeline stands at 5,312 projects/634,501 rooms, up 7% from 2017’s 4,973 projects/598,371 rooms. The pipeline has been growing moderately and incrementally each quarter and should continue its upward growth trend as long as the economy remains strong. Pipeline totals are still significantly below the all-time high of 5,883 projects/785,547 rooms reached in 2008.

Projects scheduled to start construction in the next 12 months have seen minimal change year-over-year (YOY) with 2,291 projects/266,878 rooms. Projects currently under construction are at 1,594 projects/208,509 rooms, the highest recorded since 2007. This also marks the fourth consecutive quarter that the number of rooms under construction has been over 200,000 units.

Early planning with 1,427 projects/159,114 rooms, saw a 25% increase in projects and 18% increase in rooms YOY. This increase in early planning is typical late cycle activity where developers are anxious to move from the drawing board into the permitting phase prior to any economic slowdown. Many are larger projects that wait for peak operating performance in their markets before seeking financing.

Both the increase in projects under construction and those in the early planning stage are reflective of the urgency developers currently have before the economy softens and/or interest rates further accelerate.

The top five markets with the largest hotel construction pipelines are: New York City with 169 projects/29,365 rooms; Dallas with 156 projects/18, 908 rooms; Houston with 150 projects/16,321 rooms; Nashville with 123 projects/16,392 rooms; and Los Angeles with 121 projects/18,037 rooms.

The five top markets with the most projects currently under construction are New York City with 101 projects/17,108 rooms, Dallas with 47 projects/6,350 rooms, Nashville with 43 projects/7,005 rooms, Houston with 40 projects/4,738 rooms, and Atlanta with 28 projects/3,387 rooms.

In the second quarter, Nashville has the largest number of new projects announced into the pipeline with 13 projects/1,351 rooms, followed by Los Angeles with 12 projects/1,845 rooms, New York City with 11 projects/1,075 rooms, Houston with 11 projects/909 rooms, and Dallas with 10 projects/1,229 rooms. If all of the projects in their pipelines come to fruition, these leading markets will increase their current room supply by: Nashville 38.2%, Austin 29.3%, Fort Worth 28.5%, San Jose 25.3%, and New York City 25.2%.

Hotels forecast to open in 2018 are led by New York City with 45 projects/7,762 rooms, followed by Dallas with 33 projects/ 3,813 rooms, and then Houston with 27 projects/3,114 rooms. In 2019, New York is forecast to again top the list of new hotel openings with 52 projects/7,356 rooms while, at this time, Dallas is anticipated to take the lead in 2020 with 40 projects/4,943 rooms expected to open.

Related Stories

Market Data | Aug 12, 2021

Steep rise in producer prices for construction materials and services continues in July.

The producer price index for new nonresidential construction rose 4.4% over the past 12 months.

Market Data | Aug 6, 2021

Construction industry adds 11,000 jobs in July

Nonresidential sector trails overall recovery.

Market Data | Aug 2, 2021

Nonresidential construction spending falls again in June

The fall was driven by a big drop in funding for highway and street construction and other public work.

Market Data | Jul 29, 2021

Outlook for construction spending improves with the upturn in the economy

The strongest design sector performers for the remainder of this year are expected to be health care facilities.

Market Data | Jul 29, 2021

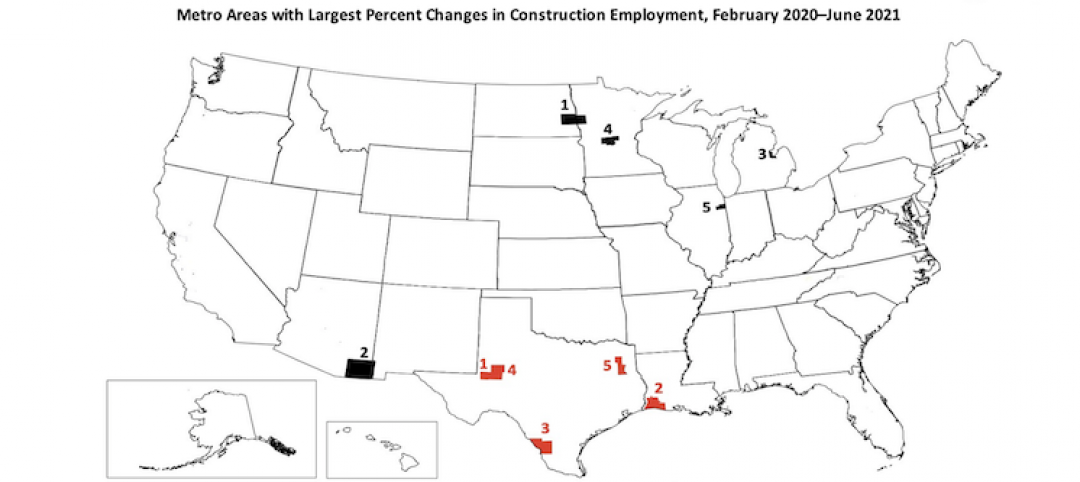

Construction employment lags or matches pre-pandemic level in 101 metro areas despite housing boom

Eighty metro areas had lower construction employment in June 2021 than February 2020.

Market Data | Jul 28, 2021

Marriott has the largest construction pipeline of U.S. franchise companies in Q2‘21

472 new hotels with 59,034 rooms opened across the United States during the first half of 2021.

Market Data | Jul 27, 2021

New York leads the U.S. hotel construction pipeline at the close of Q2‘21

Many hotel owners, developers, and management groups have used the operational downtime, caused by COVID-19’s impact on operating performance, as an opportunity to upgrade and renovate their hotels and/or redefine their hotels with a brand conversion.

Market Data | Jul 26, 2021

U.S. construction pipeline continues along the road to recovery

During the first and second quarters of 2021, the U.S. opened 472 new hotels with 59,034 rooms.

Market Data | Jul 21, 2021

Architecture Billings Index robust growth continues

AIA’s Architecture Billings Index (ABI) score for June remained at an elevated level of 57.1.

Market Data | Jul 20, 2021

Multifamily proposal activity maintains sizzling pace in Q2

Condos hit record high as all multifamily properties benefit from recovery.