At the end of 2018, analysts at Lodging Econometrics (LE) reported that the total U.S. construction pipeline continued to trend upward with 5,530 projects/669,456 rooms, both up a strong 7% year-over-year (YOY). However, pipeline totals continue to trail the all-time high of 5,883 projects/785,547 rooms reached in the second quarter of 2008.

Project counts in the early planning stage continue to rise reaching an all-time high of 1,723 projects/199,326 rooms, up 14% by projects and 12% by rooms YOY. Projects scheduled to start construction in the next 12 months stand at 2,153 projects/255,083 rooms. Projects currently under construction are at 1,654 projects/215,047 rooms, the highest counts since early 2008.

Also noteworthy at year-end, the upscale, upper-midscale, and midscale categories are at record-highs, for both rooms and projects. Luxury room counts and upper-upscale project counts are also at record levels.

In 2018, the U.S. had 947 new hotels/112,050 rooms open, a 2% growth in new supply, bringing the total U.S. census to 56,909 hotels/5,381,090 rooms. The LE forecast for new hotel openings in 2019 anticipates a 2.2% supply growth rate with 1,022 new hotels/116,357 rooms expected to open. The pace for new hotel openings has slowed slightly because of construction delays largely caused by shortages in skilled labor.

Lending at attractive rates is still accessible to developers, but lenders are growing more selective as we move deeper into the existing cycle.

The pipeline has completed its seventh consecutive year of growth. Moving forward the growth rate is expected to slow as the economies of most countries, including the United States, more firmly settle into the “new normal" marked by slow growth and low inflation.

While there are no visible signs of a recession on the horizon, the risks to the economy are not insignificant and include tariff conflicts, swings in the stock market, unforeseen geopolitical problems, any of which could send the economy lower.

Related Stories

Market Data | Jan 6, 2022

A new survey offers a snapshot of New York’s construction market

Anchin’s poll of 20 AEC clients finds a “growing optimism,” but also multiple pressure points.

Market Data | Jan 3, 2022

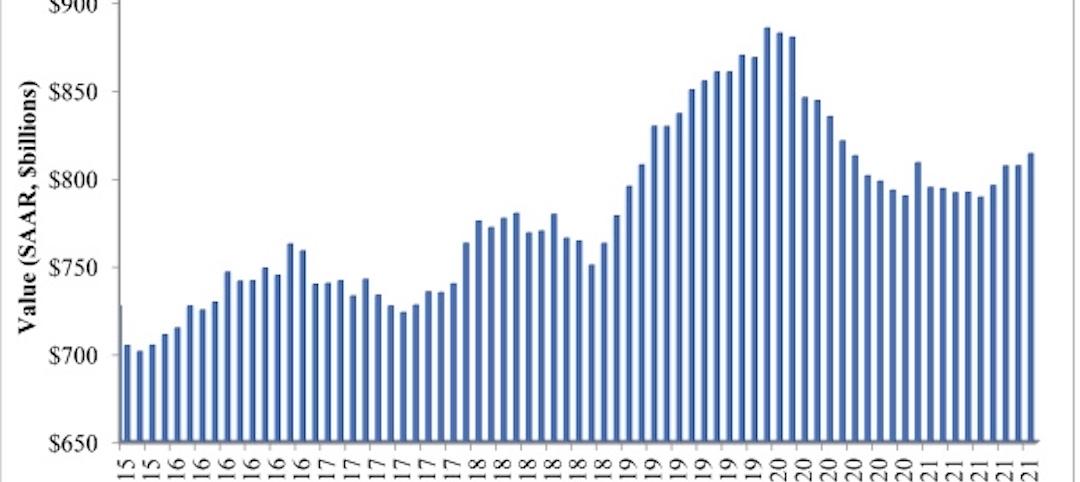

Construction spending in November increases from October and year ago

Construction spending in November totaled $1.63 trillion at a seasonally adjusted annual rate.

Market Data | Dec 22, 2021

Two out of three metro areas add construction jobs from November 2020 to November 2021

Construction employment increased in 237 or 66% of 358 metro areas over the last 12 months.

Market Data | Dec 17, 2021

Construction jobs exceed pre-pandemic level in 18 states and D.C.

Firms struggle to find qualified workers to keep up with demand.

Market Data | Dec 15, 2021

Widespread steep increases in materials costs in November outrun prices for construction projects

Construction officials say efforts to address supply chain challenges have been insufficient.

Market Data | Dec 15, 2021

Demand for design services continues to grow

Changing conditions could be on the horizon.

Market Data | Dec 5, 2021

Construction adds 31,000 jobs in November

Gains were in all segments, but the industry will need even more workers as demand accelerates.

Market Data | Dec 5, 2021

Construction spending rebounds in October

Growth in most public and private nonresidential types is offsetting the decline in residential work.

Market Data | Dec 5, 2021

Nonresidential construction spending increases nearly 1% in October

Spending was up on a monthly basis in 13 of the 16 nonresidential subcategories.

Market Data | Nov 30, 2021

Two-thirds of metro areas add construction jobs from October 2020 to October 2021

The pandemic and supply chain woes may limit gains.