Commercial and institutional construction spending is projected to be down 6.9 percent and 13 percent, respectively, in 2022, impacted by macroeconomic factors that include increasing demand for long-lead equipment, material shortages caused by supply-chain snags and the Russia-Ukraine war, and the instability of costs for fuel and labor.

That easing of demand has allowed key commodity prices to stabilize, and there is reason for optimism despite uncertainty about the health of the U.S economy that is only expected to expand by 1 percent next year.

This is the perspective of Linesight, a multinational construction consultant, which has released its Third Quarter Commodity Report for the United States. Patrick Ryan, Linesight’s Executive Vice President for the Americas, states that the “medium to long-term outlook remains positive, with [economic] growth expected in the coming years as inflation comes under control.”

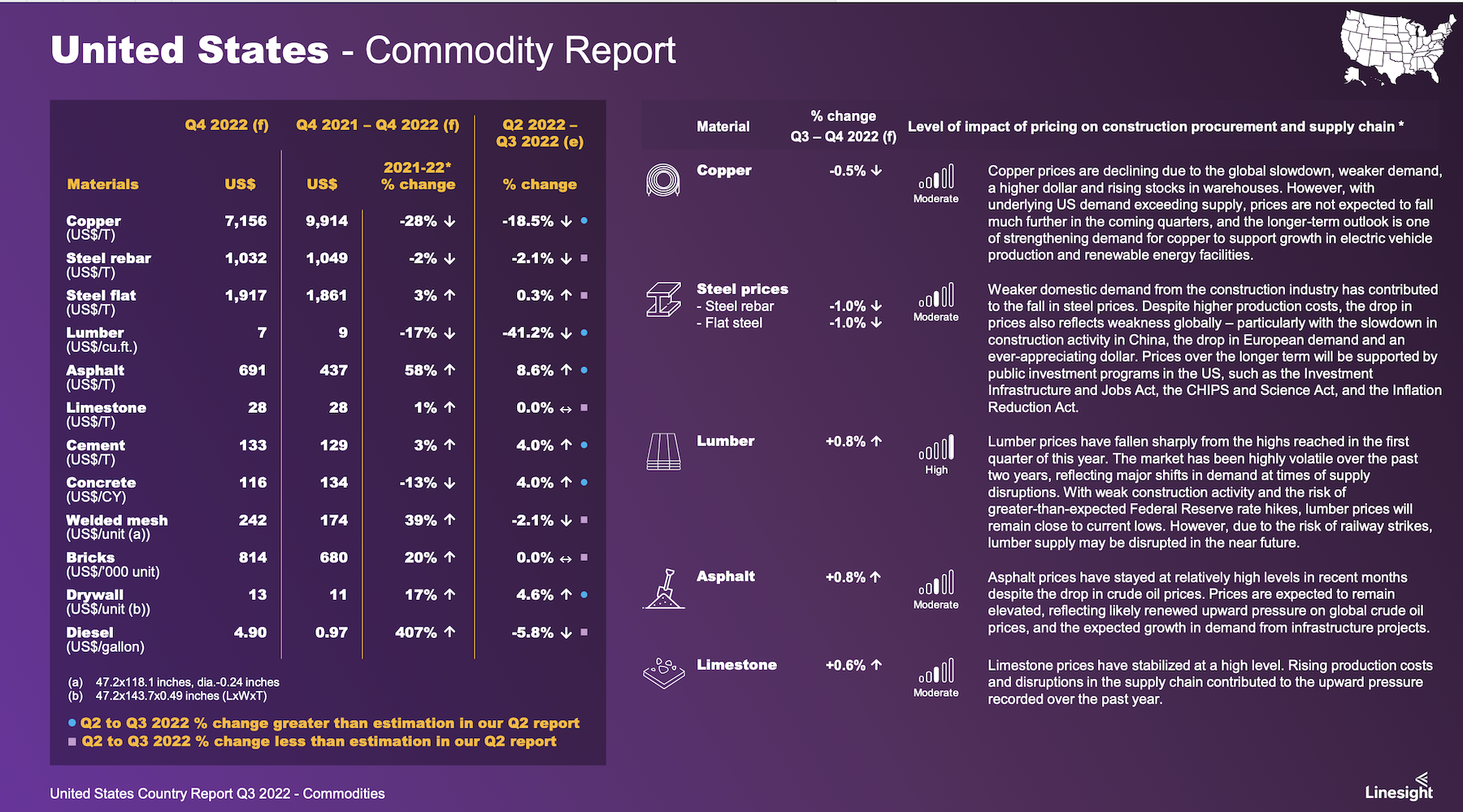

The Report focuses on five key commodities:

•Lumber, whose prices have been on a downward trend since the first quarter. Supply-side fragilities have eased, as post-flood mill inventory in British Columbia is rebuilding.

•Cement and aggregates, whose prices have been affected by oil price turbulence. Linesight sees the slowdown in residential construction as easing pressure on this commodity’s demand, although that could also be negated by commercial demand spurred by the Infrastructure Investment and Jobs Act of 2021.

•Concrete blocks and bricks, whose prices are waning along with residential construction demand that is tamped by rising mortgage interest rates.

•Rebar and structural steel, whose prices had flattened during the previous quarter, and whose weakening future demand, especially from China, anticipates falling prices. However, Linesight also cautions that high energy prices continue to drive up steel’s production costs.

•Copper, whose price declines of late have stabilized. Supply disruptions and the lack of investment in new mining operations continue to contribute to production shortfalls, and demand remains “resilient,” especially as the manufacture of electric vehicle batteries expands.

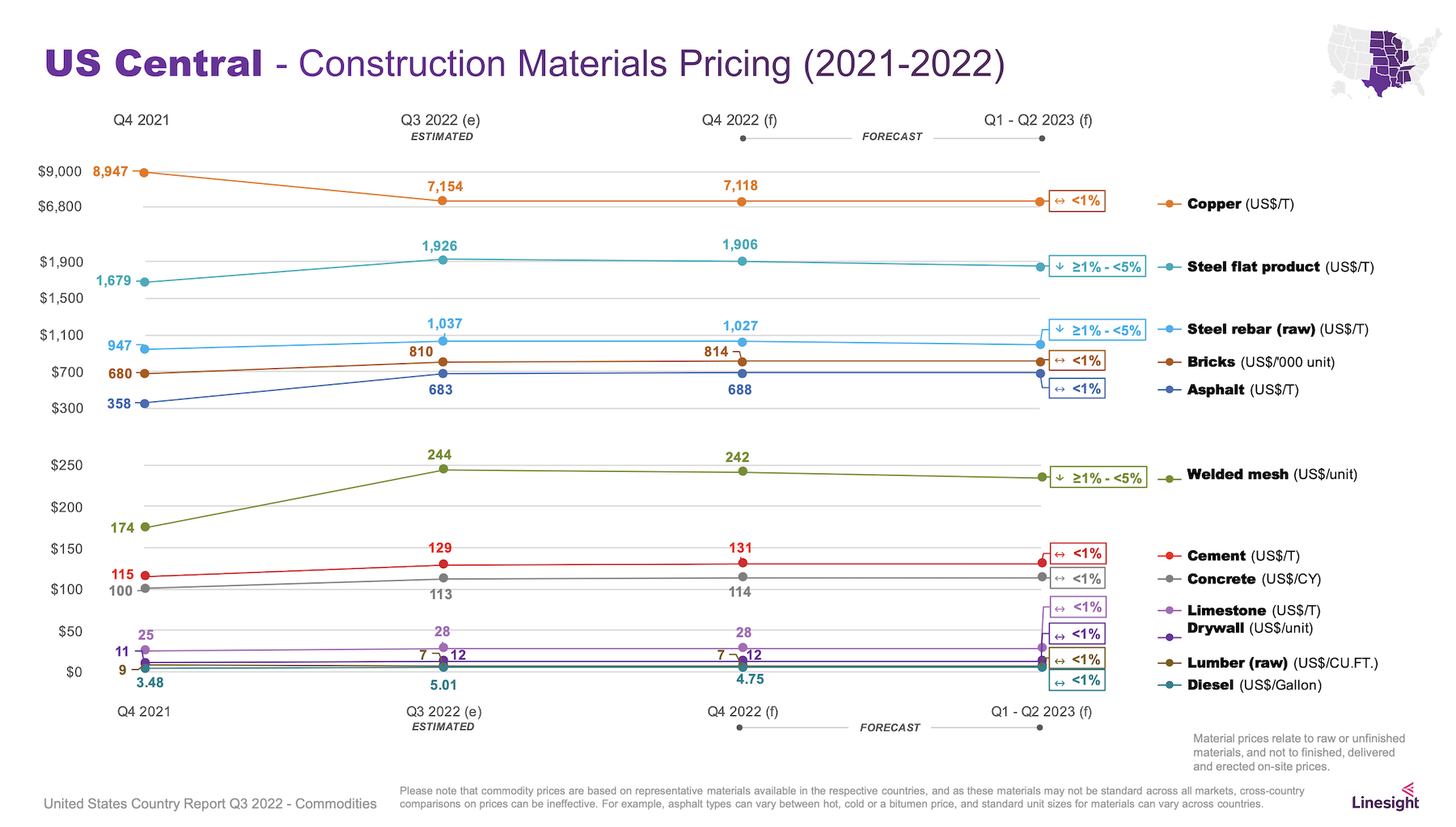

The Report prognosticates as well about pricing for asphalt, limestone, welded mesh, drywall, and diesel fuel. It also forecasts commodity prices by regions of the country, although the geographic variations are, for the most part, marginal.

Perhaps the most important issue right now affecting commodity prices, says Ryan, is mixed data on the economy. Despite two consecutive quarterly declines, “there are positive indicators being recorded to suggest economic resilience in some key areas,” such as the lowest unemployment rate in five decades, and the Federal Reserve’s aggressive actions to curb inflation.

Another bright spot is labor productivity in the U.S., which still outpaces Germany, the United Kingdom, Hong Kong, Taiwan, South Korea, and Japan.

Related Stories

Market Data | Jan 23, 2020

Construction contractor confidence surges into 2020, says ABC

Confidence among U.S. construction industry leaders increased in November 2019 with respect to sales, profit margins, and staffing, according to the Associated Builders and Contractors Construction Confidence Index.

Market Data | Jan 22, 2020

Architecture Billings Index ends year on positive note

AIA’s Architecture Billings Index (ABI) score of 52.5 for December reflects an increase in design services provided by U.S. architecture firms.

AEC Tech | Jan 16, 2020

EC firms with a clear ‘digital roadmap’ should excel in 2020

Deloitte, in new report, lays out a risk mitigation strategy that relies on tech.

Market Data | Jan 13, 2020

Construction employment increases by 20,000 in December and 151,000 in 2019

Survey finds optimism about 2020 along with even tighter labor supply as construction unemployment sets record December low.

Market Data | Jan 10, 2020

North America’s office market should enjoy continued expansion in 2020

Brokers and analysts at two major CRE firms observe that tenants are taking longer to make lease decisions.

Market Data | Dec 17, 2019

Architecture Billings Index continues to show modest growth

AIA’s Architecture Billings Index (ABI) score of 51.9 for November reflects an increase in design services provided by U.S. architecture firms.

Market Data | Dec 12, 2019

2019 sets new record for supertall building completion

Overall, the number of completed buildings of at least 200 meters in 2019 declined by 13.7%.

Market Data | Dec 4, 2019

Nonresidential construction spending falls in October

Private nonresidential spending fell 1.2% on a monthly basis and is down 4.3% from October 2018.

Market Data | Nov 25, 2019

Office construction lifts U.S. asking rental rate, but slowing absorption in Q3 raises concerns

12-month net absorption decelerates by one-third from 2018 total.

Market Data | Nov 22, 2019

Architecture Billings Index rebounds after two down months

The Architecture Billings Index (ABI) score in October is 52.0.