The institutional investment capital that’s been flowing into real estate globally is expected to increase as an already rebounding economy expands. But there’s also a growing consensus among real estate professionals that environmental, social, and governance (ESG) elements will factor more impactfully—and uncertainly—into future development. Broader housing affordability is one of those elements that could create diverse workforces and drive equitable outcomes.

These are some of the trends that arise from a survey of industry experts whose responses form the basis of “Emerging Trends in Real Estate 2022,” the 43rd edition of this series, which was released today. (To download the full report, click here.)

Researchers for the latest report’s co-sponsors, PwC and Urban Land Institute (ULI), interviewed 930 individuals and evaluated survey responses from another 1,200. Private property owners or commercial/multifamily real estate developers accounted for 35% of the respondents; real estate advisory, service, or asset managers 22%.

Among the AEC firms whose representatives were interviewed were BOKA Powell, Brasfield & Gorrie, CM Constructors, Gensler, Kimley Horn, Malasri Engineering, Swinerton, STG Design, Tenet Design, and Turner Construction.

The 100-page report lays out the challenges that lie ahead for the real estate sector to cope with changing consumer expectations and a “massive shift” in the functionality of homes, offices, retail, and healthcare spaces. “Property markets that were once predictable will likely remain in a bubble of uncertainty,” the reports states. It will also be “imperative” for businesses’ strategies to approach environmental, social, and governance issues holistically.

IS HOUSING AFFORDABILITY INTRACTABLE?

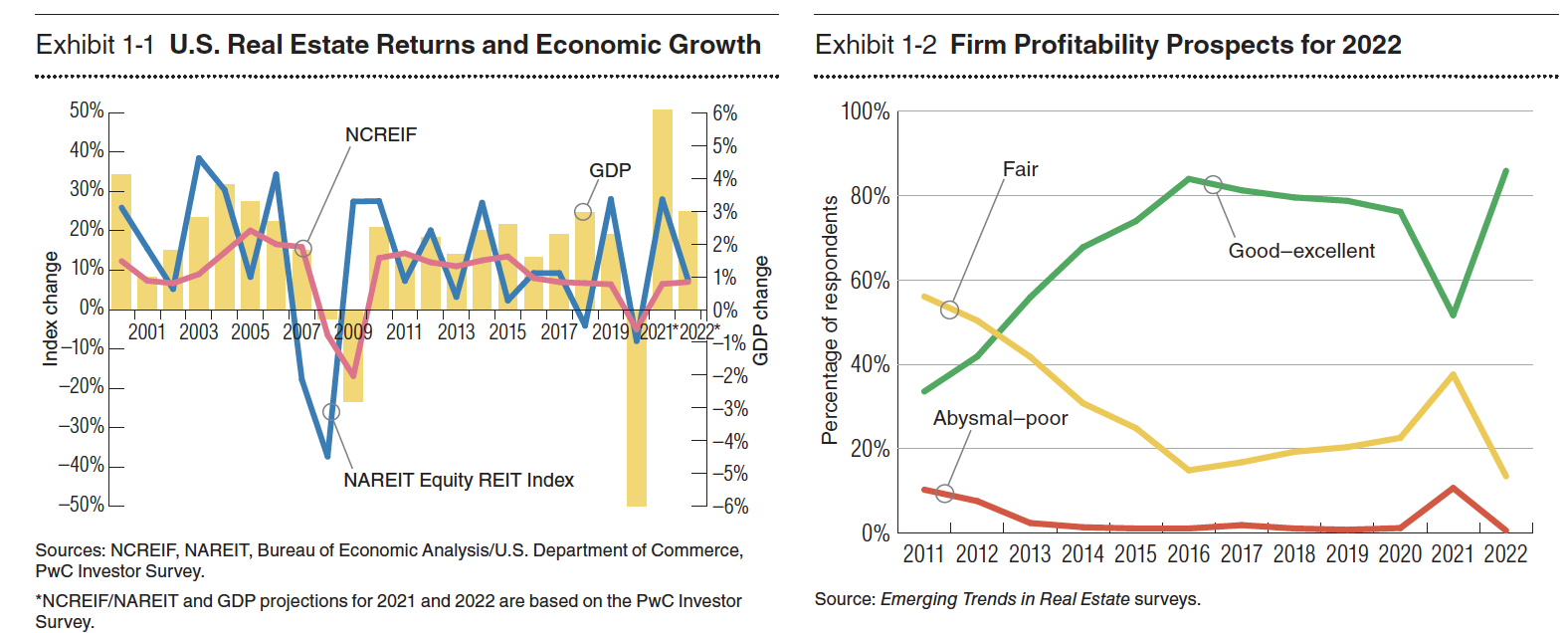

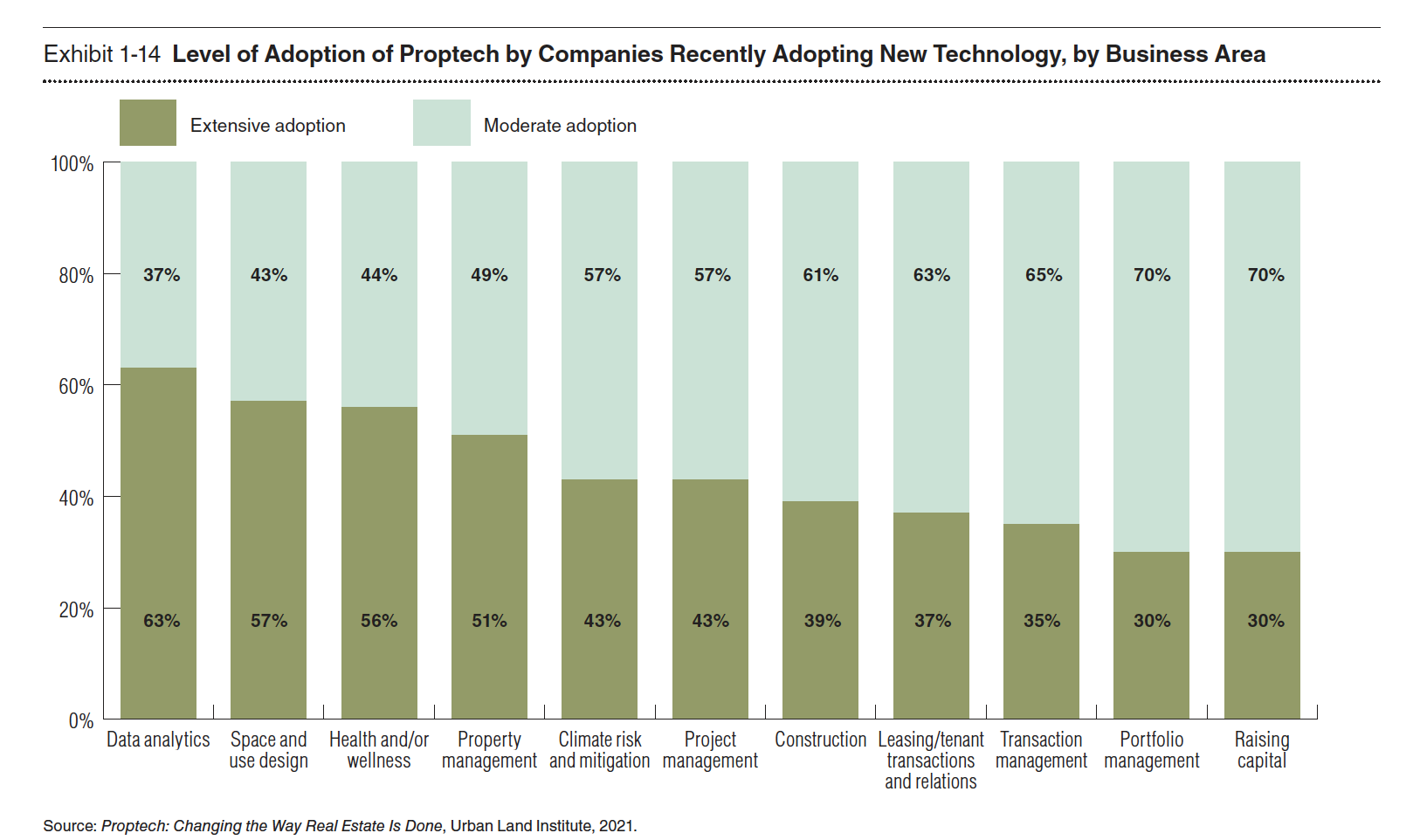

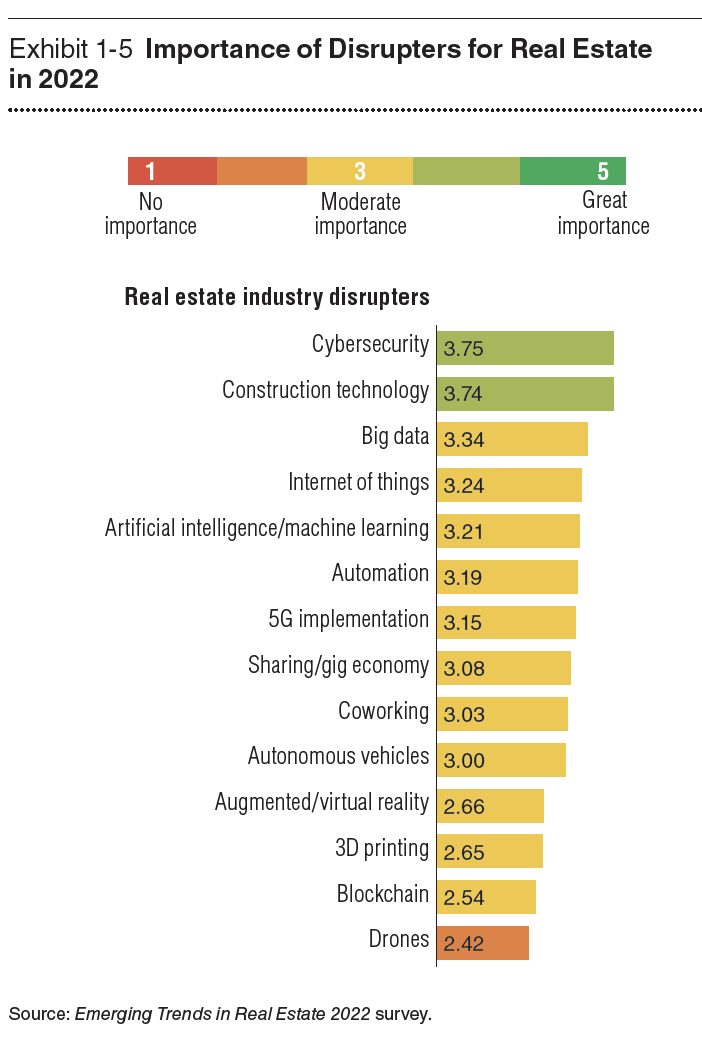

The report finds the real estate community optimistic about its future, and the main reason is “an abundance of investable capital, low interest rates, and continued demand for many product types,” says Byron Carlock, a Partner and U.S. Real Estate Practice Leader for PwC. The real estate industry is also finally getting into the 21st Century by adopting technology to assess investments and manage properties. But despite higher acceptance, property technology “still has significant areas of future growth,” the report states.

The report highlights several other trends that include a rebound from a COVID-19 induced “brief and muted real estate downturn” in real estate investment. Economic output is forecasted to grow “at the highest rate in decades” in 2021 and 2022. One area of concern, however, is housing affordability, which “worsened” during the pandemic and as the economy reopened. “Affordability will likely continue to deteriorate in the absence of significant private-sector and government intervention,” the report asserts.

Remarkably, 82% of respondents claimed that their companies consider ESG elements when making operational or investment decisions. However, the report also observes that investors “have been slow to incorporate environmental risks into underwriting.”

THE SUNBELT OFFERS FERTILE CRE PROSPECTS

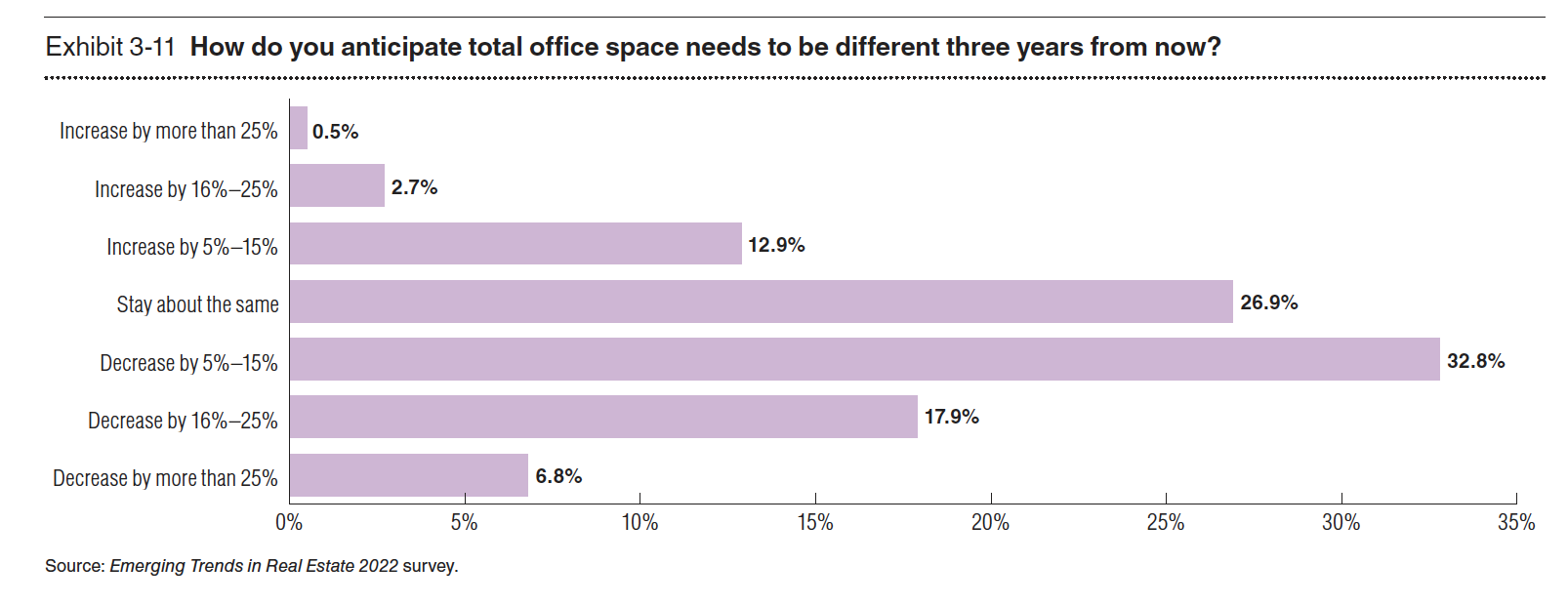

One of the question marks in the real estate sector revolves around the future value of office space. Nearly two-thirds of the report’s respondents believe that fewer than 75% of workers will return to their offices at least three days a week in 2022. In fact, industry leaders predict that the need for office space will decrease by 5-15 percent in the next three years. This trend is already leading to redesigns of offices for hybrid work patterns and flexible usage.

The office conundrum is compounded by what the report calls the Great Relocation, where highly paid office workers are moving away from their workplaces. The report’s authors think this phenomenon could create more of a suburban and Sun Belt future. “Sun Belt metropolitan areas account for the eight to-rated overall real estate prospects [and] occupy the top five places in the homebuilding prospects rating.”

Nashville was identified as the No. 1 market for real estate prospects, based on growth, homebuilding, affordability, and employment opportunity. It was followed by Raleigh-Durham, N.C., Phoenix, Austin, Texas, Tampa-St. Petersburg, Fla., Charlotte, Dallas-Fort Worth, Atlanta, Seattle, and Boston.

The report points out as well that investors and Real Estate Investment Trusts (REITs) are now more disposed to consider alternative sectors like student and senior housing, life sciences, and industrial. These sectors, the report explains, offer higher returns at lower prices. They are less volatile to business cycles, too.

Related Stories

Market Data | Mar 29, 2017

Contractor confidence ends 2016 down but still in positive territory

Although all three diffusion indices in the survey fell by more than five points they remain well above the threshold of 50, which signals that construction activity will continue to be one of the few significant drivers of economic growth.

Market Data | Mar 24, 2017

These are the most and least innovative states for 2017

Connecticut, Virginia, and Maryland are all in the top 10 most innovative states, but none of them were able to claim the number one spot.

Market Data | Mar 22, 2017

After a strong year, construction industry anxious about Washington’s proposed policy shifts

Impacts on labor and materials costs at issue, according to latest JLL report.

Market Data | Mar 22, 2017

Architecture Billings Index rebounds into positive territory

Business conditions projected to solidify moving into the spring and summer.

Market Data | Mar 15, 2017

ABC's Construction Backlog Indicator fell to end 2016

Contractors in each segment surveyed all saw lower backlog during the fourth quarter, with firms in the heavy industrial segment experiencing the largest drop.

Market Data | Feb 28, 2017

Leopardo’s 2017 Construction Economics Report shows year-over-year construction spending increase of 4.2%

The pace of growth was slower than in 2015, however.

Market Data | Feb 23, 2017

Entering 2017, architecture billings slip modestly

Despite minor slowdown in overall billings, commercial/ industrial and institutional sectors post strongest gains in over 12 months.

Market Data | Feb 16, 2017

How does your hospital stack up? Grumman/Butkus Associates 2016 Hospital Benchmarking Survey

Report examines electricity, fossil fuel, water/sewer, and carbon footprint.

Market Data | Feb 1, 2017

Nonresidential spending falters slightly to end 2016

Nonresidential spending decreased from $713.1 billion in November to $708.2 billion in December.

Market Data | Jan 31, 2017

AIA foresees nonres building spending increasing, but at a slower pace than in 2016

Expects another double-digit growth year for office construction, but a more modest uptick for health-related building.