Both Nonresidential and Residential Spending Retreat from January Levels amid Extreme Winter Weather; Association Posts Inflation Alert to Aid Understanding of Squeeze on Nonresidential Construction Firms

Construction spending slumped in February as unseasonably severe weather hammered the industry and a decline in new projects squeezed nonresidential contractors experiencing rising costs and delivery times, according to an analysis of new federal construction spending data by the Associated General Contractors of America. The association posted a Construction Inflation Alert to inform project owners and government officials about the threat to project completion dates and contractors’ financial health.

“The downturn in February reflects both an unfavorable change from mild January weather and an ongoing decline in new nonresidential projects,” said Ken Simonson, the association’s chief economist. “Unfortunately, it will take more than mild weather to help nonresidential contractors overcome the multiple challenges of falling demand for many project types, steeply rising costs, and lengthening or uncertain delivery times for key materials.”

Construction spending in February totaled $1.52 trillion at a seasonally adjusted annual rate, a decrease of 0.8% from the pace in January. Although the overall total was 5.3% higher than in February 2020, the year-over-year gain was limited to residential construction, Simonson noted. That segment slipped 0.2% for the month but jumped 21% year-over-year. Meanwhile, combined private and public nonresidential spending declined 1.3% from January and 6.1% over 12 months.

Private nonresidential construction spending fell 1.0% from January to February and 9.7% since February 2020, with year-over-year decreases in all 11 subsegments. The largest private nonresidential category, power construction, retreated 9.7% year-over-year and 0.4% from January to February. Among the other large private nonresidential project types, commercial construction—comprising retail, warehouse and farm structures—slumped 7.1% year-over-year and 1.2% for the month. Manufacturing construction tumbled 10.4% from a year earlier despite a pickup of 0.3% in February. Office construction decreased 5.0% year-over-year and 0.5% in February.

Public construction spending dipped 0.9% year-over-year and 1.7% for the month. Among the largest segments, highway and street construction declined 1.0% from a year earlier and 0.6% for the month, while educational construction decreased 2.3 percent year-over-year and 3.2 percent in February. Spending on transportation facilities declined 2.3 percent over 12 months and 2.5 percent in February.

Association officials said that rising materials prices and unreliable delivery schedules are making it hard for firms to remain profitable as they have difficulty passing raising prices for construction work. They said that proposed new infrastructure projects will help boost demand for many types of construction projects. But they urged Washington officials to also take steps to address supply-chain challenges, including by ending tariffs on key materials like lumber and steel.

“Contractors are having a hard time finding work, and when they do, they are getting squeezed by rapidly rising materials prices,” said Stephen E. Sandherr, the association’s chief executive officer. “New infrastructure investments will certainly help with demand, but the industry also needs Washington to help address supply-chain problems and rising costs.”

Related Stories

Market Data | Apr 11, 2023

Construction crane count reaches all-time high in Q1 2023

Toronto, Seattle, Los Angeles, and Denver top the list of U.S/Canadian cities with the greatest number of fixed cranes on construction sites, according to Rider Levett Bucknall's RLB Crane Index for North America for Q1 2023.

Contractors | Apr 11, 2023

The average U.S. contractor has 8.7 months worth of construction work in the pipeline, as of March 2023

Associated Builders and Contractors reported that its Construction Backlog Indicator declined to 8.7 months in March, according to an ABC member survey conducted March 20 to April 3. The reading is 0.4 months higher than in March 2022.

Market Data | Apr 6, 2023

JLL’s 2023 Construction Outlook foresees growth tempered by cost increases

The easing of supply chain snags for some product categories, and the dispensing with global COVID measures, have returned the North American construction sector to a sense of normal. However, that return is proving to be complicated, with the construction industry remaining exceptionally busy at a time when labor and materials cost inflation continues to put pricing pressure on projects, leading to caution in anticipation of a possible downturn. That’s the prognosis of JLL’s just-released 2023 U.S. and Canada Construction Outlook.

Market Data | Apr 4, 2023

Nonresidential construction spending up 0.4% in February 2023

National nonresidential construction spending increased 0.4% in February, according to an Associated Builders and Contractors analysis of data published by the U.S. Census Bureau. On a seasonally adjusted annualized basis, nonresidential spending totaled $982.2 billion for the month, up 16.8% from the previous year.

Multifamily Housing | Mar 24, 2023

Average size of new apartments dropped sharply in 2022

The average size of new apartments in 2022 dropped sharply in 2022, as tracked by RentCafe. Across the U.S., the average new apartment size was 887 sf, down 30 sf from 2021, which was the largest year-over-year decrease.

Multifamily Housing | Mar 14, 2023

Multifamily housing rent rates remain flat in February 2023

Multifamily housing asking rents remained the same for a second straight month in February 2023, at a national average rate of $1,702, according to the new National Multifamily Report from Yardi Matrix. As the economy continues to adjust in the post-pandemic period, year-over-year growth continued its ongoing decline.

Contractors | Mar 14, 2023

The average U.S. contractor has 9.2 months worth of construction work in the pipeline, as of February 2023

Associated Builders and Contractors reported today that its Construction Backlog Indicator increased to 9.2 months in February, according to an ABC member survey conducted Feb. 20 to March 6. The reading is 1.2 months higher than in February 2022.

Industry Research | Mar 9, 2023

Construction labor gap worsens amid more funding for new infrastructure, commercial projects

The U.S. construction industry needs to attract an estimated 546,000 additional workers on top of the normal pace of hiring in 2023 to meet demand for labor, according to a model developed by Associated Builders and Contractors. The construction industry averaged more than 390,000 job openings per month in 2022.

Market Data | Mar 7, 2023

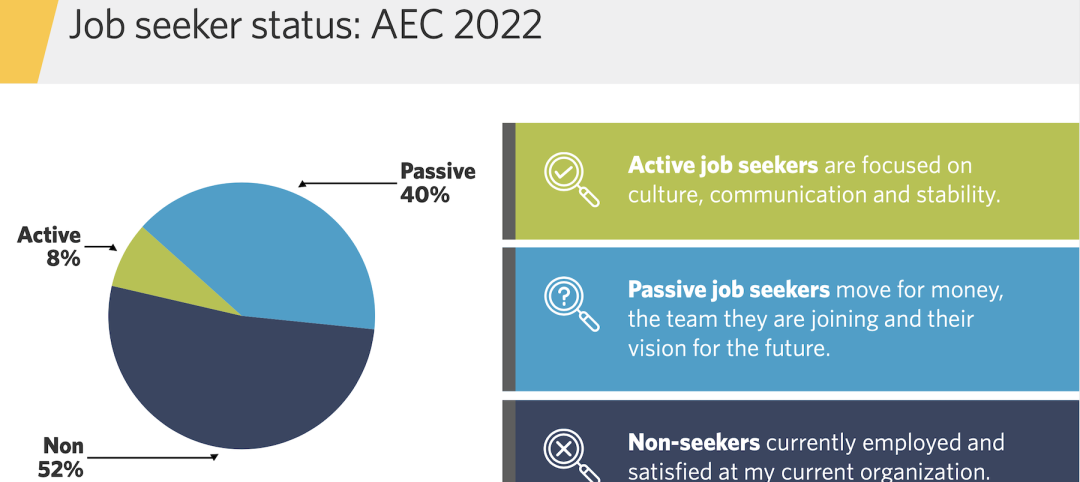

AEC employees are staying with firms that invest in their brand

Hinge Marketing’s latest survey explores workers’ reasons for leaving, and offers strategies to keep them in the fold.

Multifamily Housing | Feb 21, 2023

Multifamily housing investors favoring properties in the Sun Belt

Multifamily housing investors are gravitating toward Sun Belt markets with strong job and population growth, according to new research from Yardi Matrix. Despite a sharp second-half slowdown, last year’s nationwide $187 billion transaction volume was the second-highest annual total ever.