Despite rising demand, the construction industry is expected to see a serious falloff in building starts, according Jones Lang Lasalle’s Construction Trends and Midyear Update, which JLL released this morning.

The report takes a fresh look at the industry’s overall health, the current availability and pricing for labor and materials, and the direction that total construction costs may be headed.

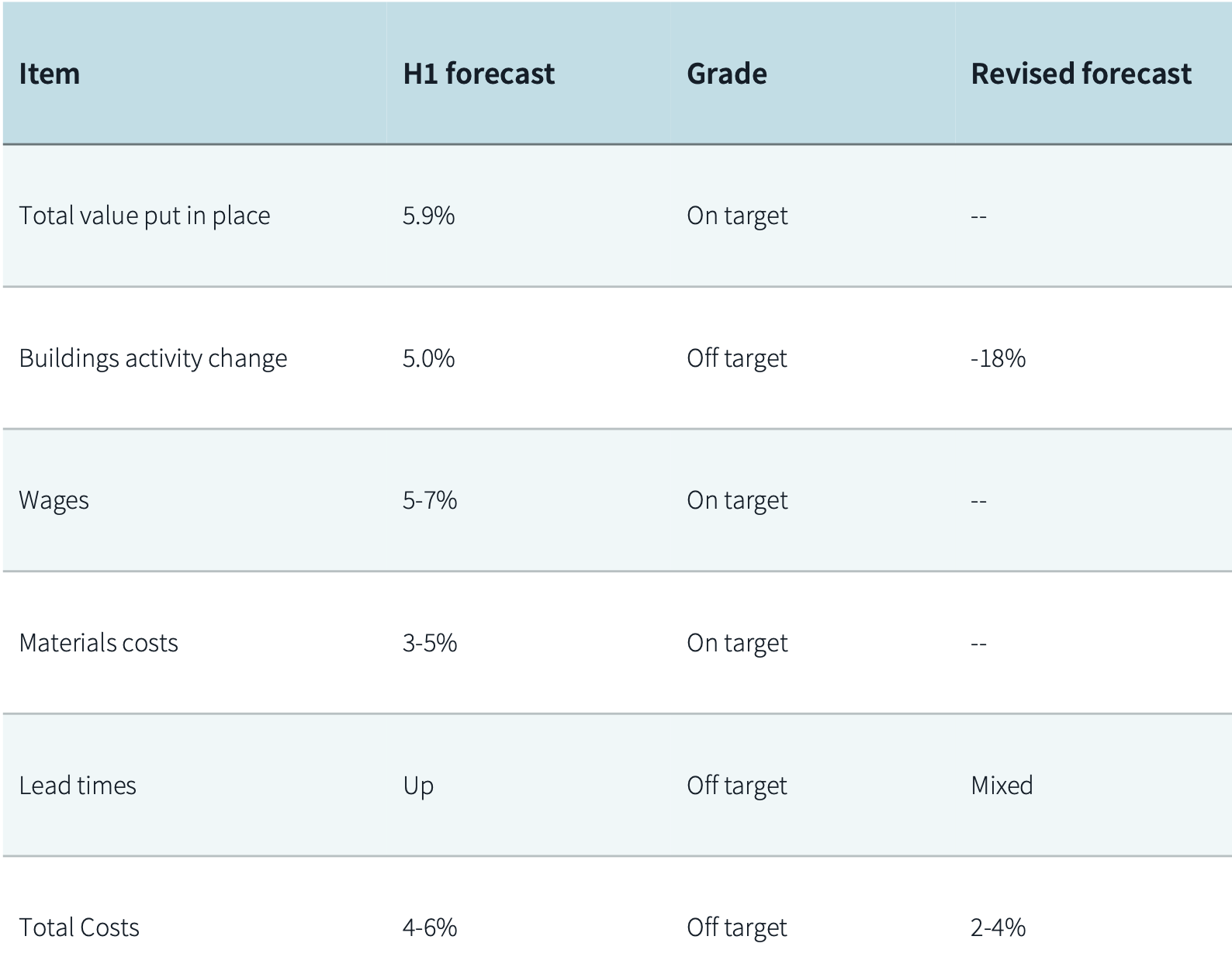

JLL still sees the construction sector in “uncharted economic territory,” as global threats remain unrealized “but full of disruptive potential” even as construction continues at breakneck speed to address post-pandemic built-environment needs. Consequently, JLL updated its projections for three of the seven barometers it tracks (see chart).

The outlook’s four key takeaways are:

•Industry Health: Financing constraints have driven a rapid decline in construction starts over the last quarter;

•Labor: Firms are prioritizng talent retention strategies;

•Materials: Supply chain issues have largely stabilized, and future cost increases should be manageable;

•Total Costs: Firms' responses to the impending slowdown have led to a drop in total costs during the third quarter, prompting JLL to revise its total cost growth forecast down to 2-4%, from 4-6% in the first half of the year.

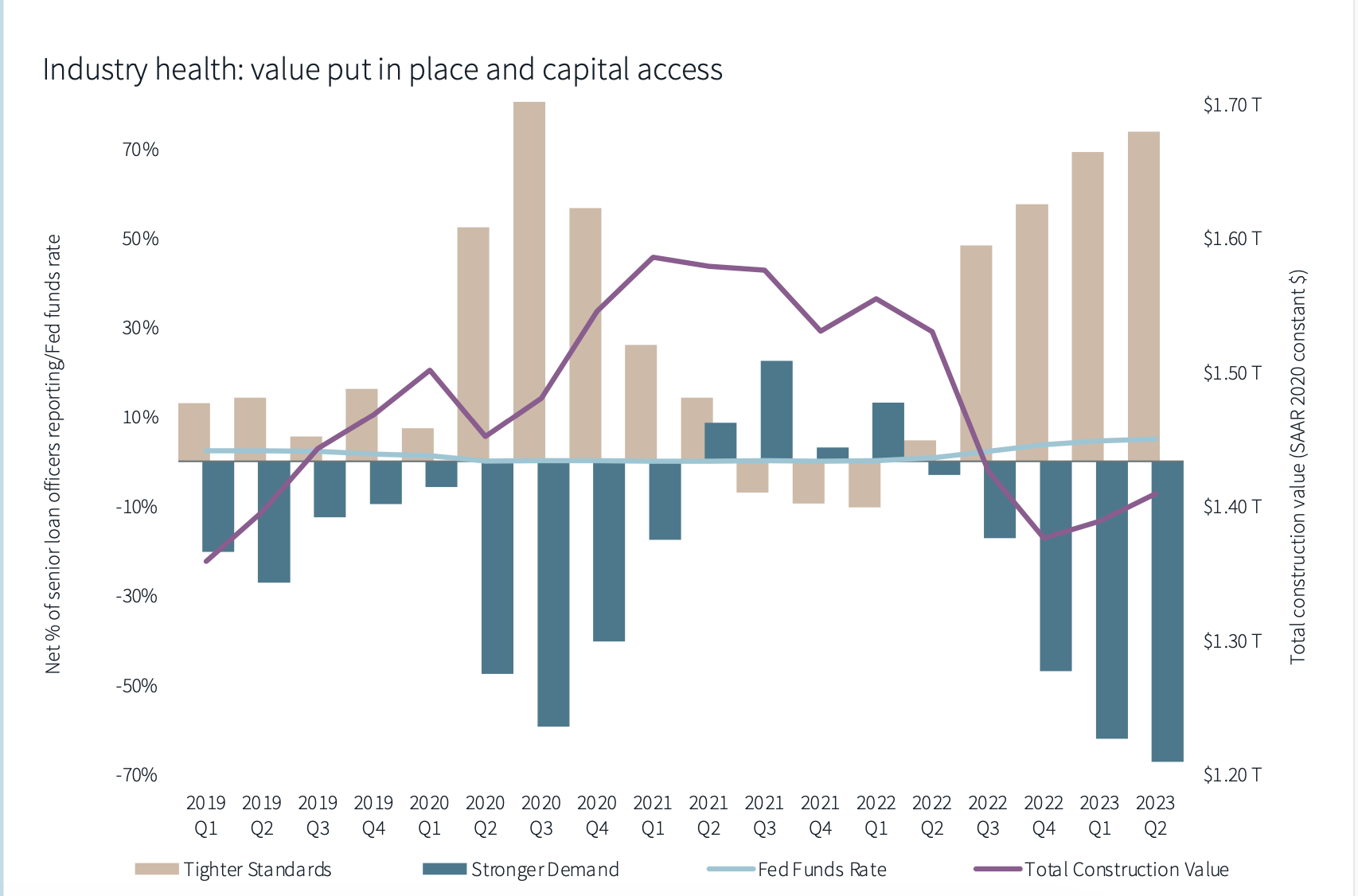

Interest rates are curtailing building starts

Based on midyear data, JLL’s forecast for construction value put in place aligns with its previous expectations. Overall, industry sentiment is strong, but construction is expected to cool depending on resolution or escalation of threats ranging from inflation to geopolitical turmoil. JLL’s revised forecast anticipates an 18% decline in building activity, compared with its 5% growth forecast for the first half of the year.

Rising interest rates are slowing construction starts. But demand for infrastructure and other non-building projects remains strong. JLL predicts interest rates will peak near the end of this year, and construction activity should rev up, “with specialization and complexity management playing vital roles.“

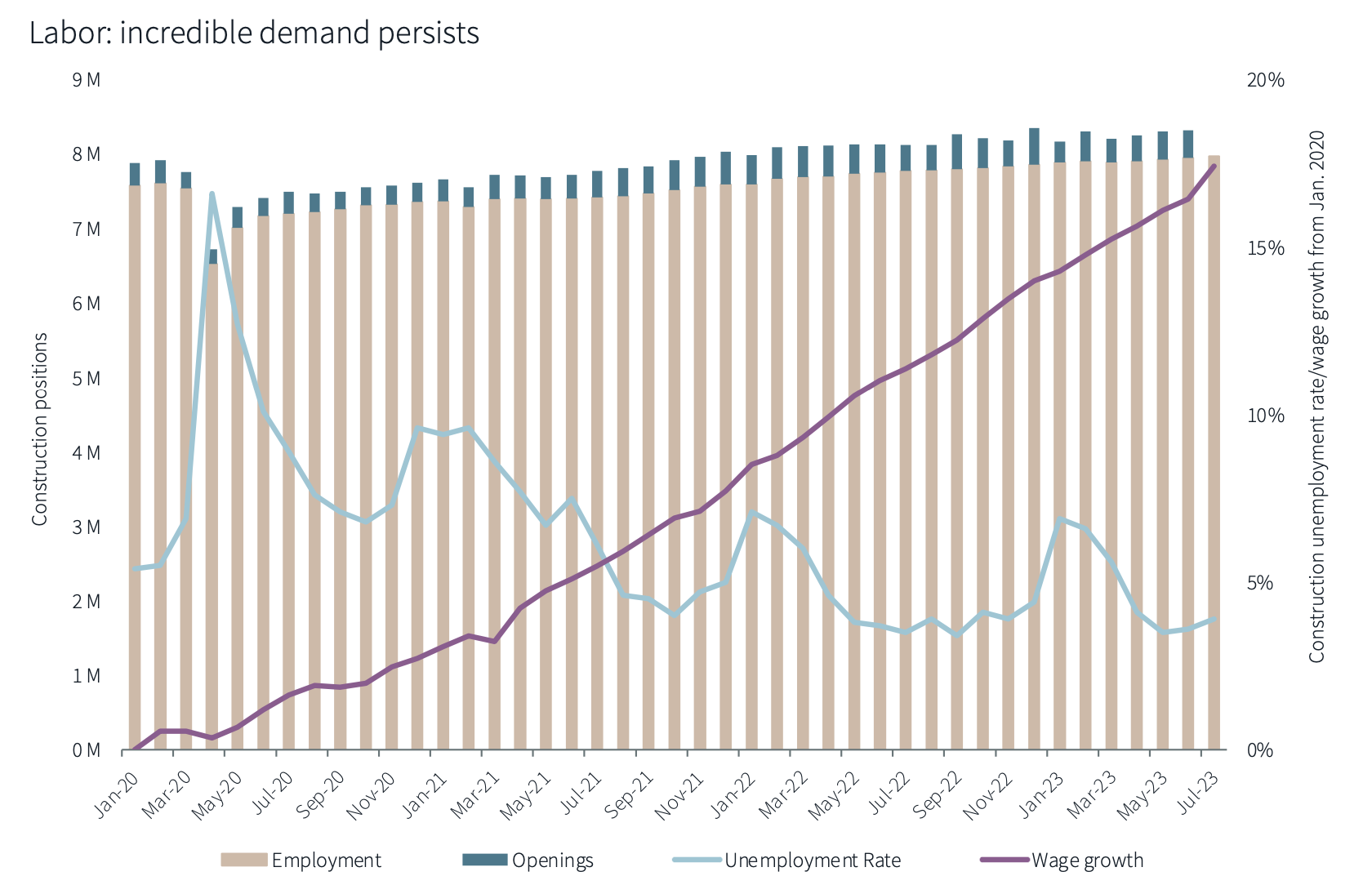

JLL continues to stand by its forecast of 5-7% growth in labor costs. Job openings remain high, and unemployment is unusually low. There is “persistent” wage competition for skilled workers. However, contractors remain confident about their ability to weather the expected downturn. JLL foresees minimal disruption in sectors buoyed by public sector spending; other sectors could see more of a dropoff, though. Construction activity per employee will remain above pre-pandemic levels for the foreseeable future.

Total costs are stabilizing

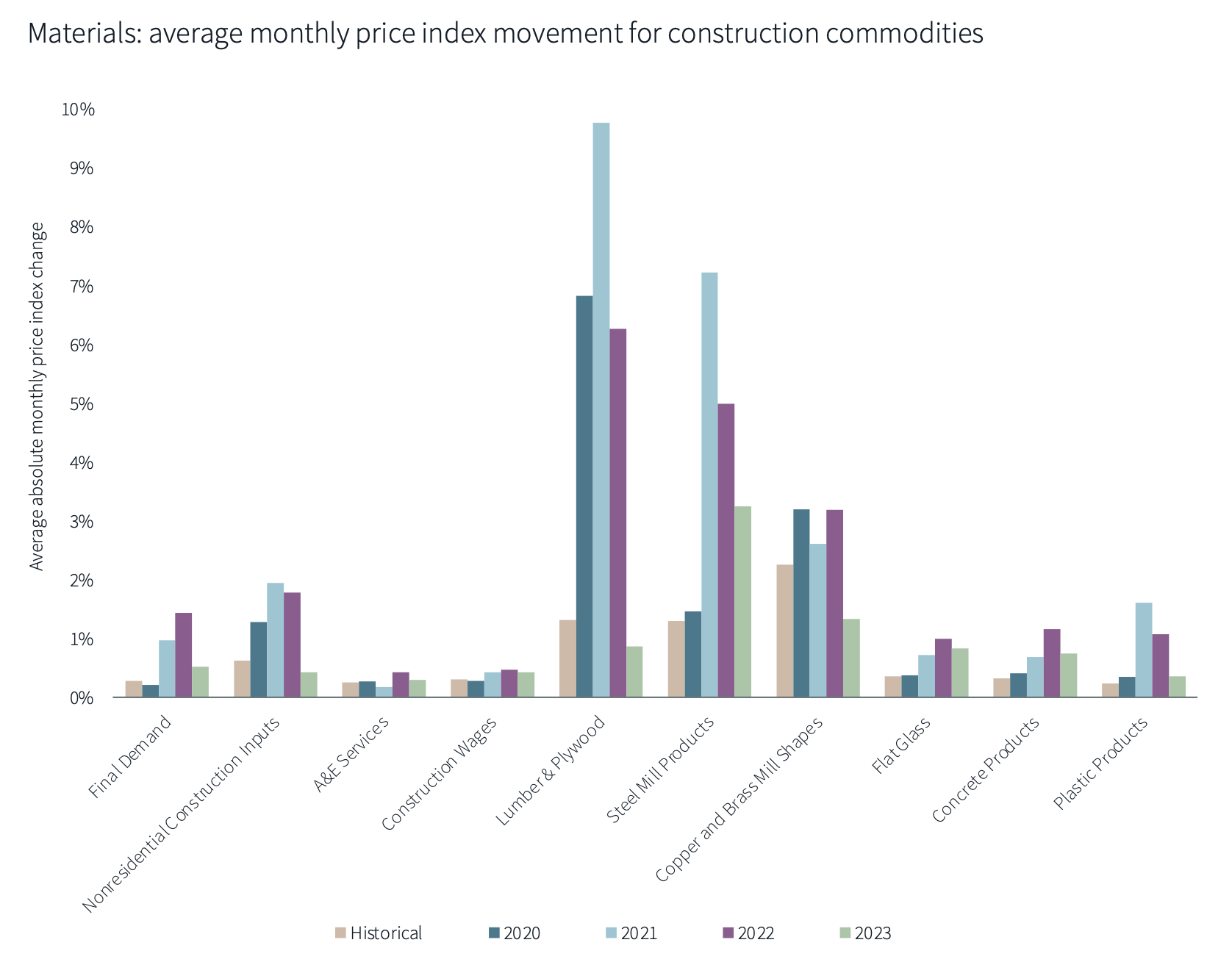

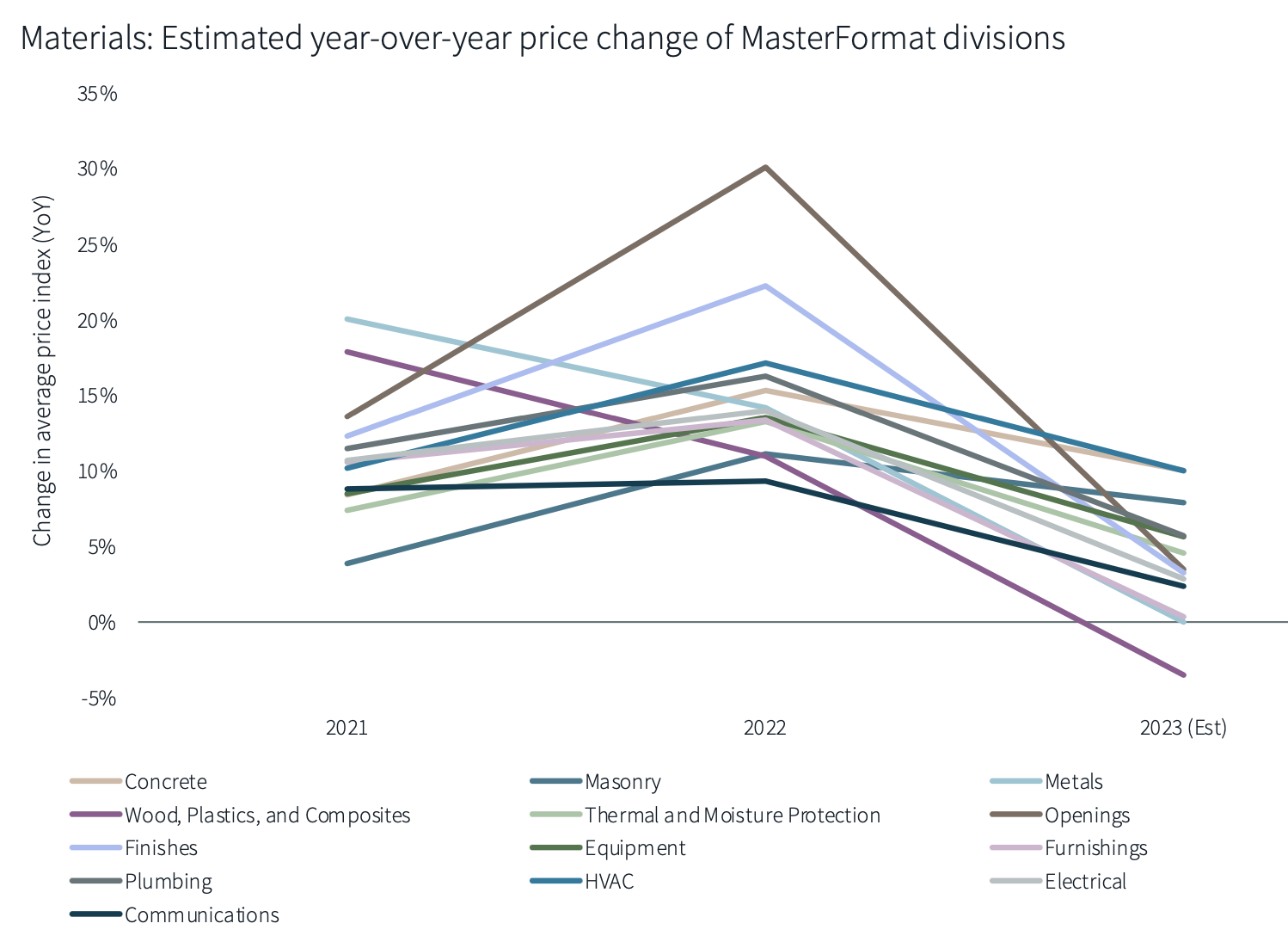

JLL also believes that its prediction of a 3-5% increase in materials costs remains on target. Commodities are exhibiting varying price fluctuations. Lead times were high in the first half of 2023, especially for MEP goods, making it harder for contractors to keep up with electrification and data center demand. Steel, concrete, glass, and plastic products’ price movements are also above historic levels. JLL expects materials costs to continue to rise at their current modest (single-digit) pace, having less impact on demand. But summer wildfires are likely to impact the supply of Canadian softwood.

Mixing these factors, JLL concludes that total construction costs have stabilized, having recorded the slowest period of growth (and the first declines) since the immediate aftermath of COVID-19 being declared a global emergency. Firms are navigating wage hikes, and expect sales and profit to grow modestly and stabilize, respectively. Labor retention is a priority to hold the line on costs. JLL adjusts its projection for total cost growth down to between 2-4%, from 4-6% in the first half.

Related Stories

Codes and Standards | Jul 22, 2022

Hurricane-resistant construction may be greatly undervalued

New research led by an MIT graduate student at the school’s Concrete Sustainability Hub suggests that the value of buildings constructed to resist wind damage in hurricanes may be significantly underestimated.

Market Data | Jul 21, 2022

Architecture Billings Index continues to stabilize but remains healthy

Architecture firms reported increasing demand for design services in June, according to a new report today from The American Institute of Architects (AIA).

Market Data | Jul 21, 2022

Despite deteriorating economic conditions, nonresidential construction spending projected to increase through 2023

Construction spending on buildings is projected to increase just over nine percent this year and another six percent in 2023, according to a new report from the American Institute of Architects (AIA).

Building Team | Jul 18, 2022

Understanding the growing design-build market

FMI’s new analysis of the design-build market forecast for the next fives years shows that this delivery method will continue to grow, despite challenges from the COVID-19 pandemic.

Market Data | Jul 1, 2022

Nonresidential construction spending slightly dips in May, says ABC

National nonresidential construction spending was down by 0.6% in May, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau.

Market Data | Jun 30, 2022

Yardi Matrix releases new national rent growth forecast

Rents in most American cities continue to rise slightly each month, but are not duplicating the rapid escalation rates exhibited in 2021.

Market Data | Jun 22, 2022

Architecture Billings Index slows but remains strong

Architecture firms reported increasing demand for design services in May, according to a new report today from The American Institute of Architects (AIA).

Building Team | Jun 17, 2022

Data analytics in design and construction: from confusion to clarity and the data-driven future

Data helps virtual design and construction (VDC) teams predict project risks and navigate change, which is especially vital in today’s fluctuating construction environment.

Market Data | Jun 15, 2022

ABC’s construction backlog rises in May; contractor confidence falters

Associated Builders and Contractors reports today that its Construction Backlog Indicator increased to nine months in May from 8.8 months in April, according to an ABC member survey conducted May 17 to June 3. The reading is up one month from May 2021.

Market Data | May 18, 2022

Architecture Billings Index moderates slightly, remains strong

For the fifteenth consecutive month architecture firms reported increasing demand for design services in April, according to a new report today from The American Institute of Architects (AIA).