Analysts at Lodging Econometrics (LE) state that Asia Pacific’s total construction pipeline, excluding China, hit a new all-time high at the close of 2019 with 1,926 projects/409,447 rooms. Project counts are up 7%, while room counts are up 8%, year-over-year (YOY).

Projects currently under construction stand at a record 991 projects with 224,354 rooms. Projects scheduled to start construction in the next 12 months and those in the early planning stage are also at all-time highs with 436 projects/85,417 rooms and 499 projects/99,676 rooms, respectively.

New projects announced into the pipeline have accelerated noticeably with 319 projects/55,165 rooms announced in the fourth quarter of 2019. This is the highest number of new projects announced since the second quarter of 2014 when 568 projects/98,738 rooms were announced.

The Asia Pacific region had 374 new hotels/69,527 rooms open in 2019. The LE forecast anticipates that 439 projects/84,188 rooms are expected to open in 2020. Should all these projects come online, this will be the highest count of new hotel openings that LE has ever recorded. Then in 2021, new hotel openings are forecast to slow to 371 projects/76,710 rooms.

Countries with the largest pipelines in Asia Pacific, excluding China, are led by Indonesia with 367 projects/60,354 rooms, which accounts for 19% of the projects in the total pipeline. Next is India with 265 projects/36,469 rooms, then Japan with 251 projects/49,869 rooms. These countries are followed by Australia, at an all-time high, with 192 projects/36,350 rooms and then Vietnam with 149 projects/59,857 rooms.

Cities in the Asia Pacific region, excluding China, with the largest construction pipelines are Jakarta, Indonesia with 86 projects/15,163 rooms, Seoul, South Korea with 68 projects/13,373 rooms and Tokyo, Japan with 61 projects/13,210 rooms. Kuala Lumpur, Malaysia follows with 50 projects/13,147 rooms and then Bangkok, Thailand with 43 projects/11,427 rooms.

The top franchise companies in Asia Pacific, excluding China, are Marriott International, at a new all-time high, with 273 projects/61,590 rooms, AccorHotels with 224 projects/46,502 rooms, and InterContinental Hotels Group (IHG) with 151 projects/32,701 rooms. Hilton Worldwide follows, also at record high counts, with 93 projects/20,762 rooms. Combined, these four companies account for 40% of the rooms in the total construction pipeline.

Top brands in Asia Pacific’s construction pipeline, excluding China, include Marriott International’s Fairfield Inn, at a record high, with 40 projects/6,563 rooms, and Courtyard with 37 projects/7,889 rooms; AccorHotels’ Ibis brands with 49 projects/9,305 rooms and Novotel with 43 projects/10,438 rooms; IHG’s Holiday Inn with 58 projects/12,457 rooms and Holiday Inn Express with 31 projects/6,281 rooms; Hilton Worldwide’s top brands are DoubleTree with 33 projects/6,514 rooms and full-service Hilton Hotel & Resorts, at an all-time high, with 30 projects/7,885 rooms.

*Please keep in mind that the COVID-19 (coronavirus) did not have an impact on fourth quarter 2019 totals reported by LE. As of the printing of this media release, countries in Asia Pacific that have been most affected by COVID-19, after China, are South Korea, Japan and Singapore. New confirmed cases continue to be added and it is still too early to predict the full impact of the outbreak on the hospitality and lodging industry. We will have more information to report in the coming months.

Related Stories

Market Data | Aug 2, 2017

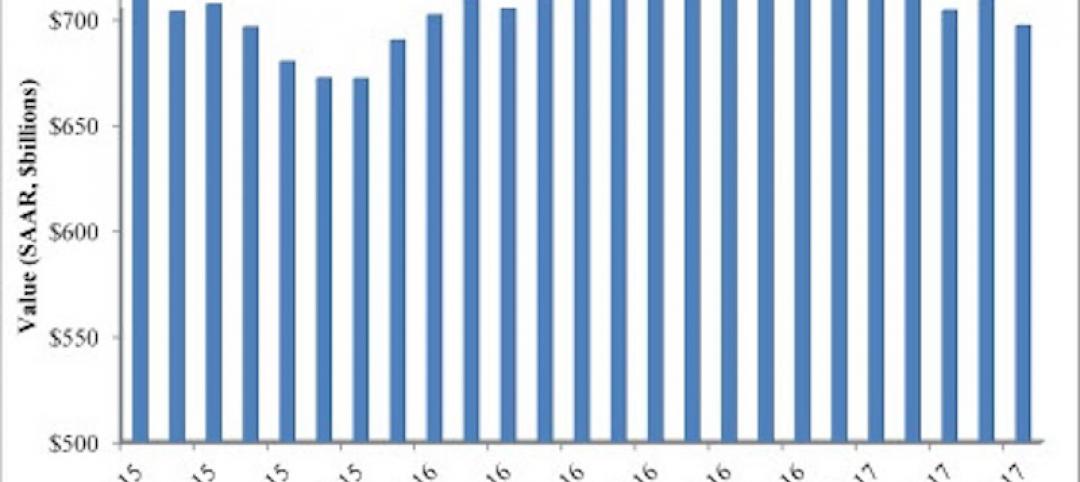

Nonresidential Construction Spending falls in June, driven by public sector

June’s weak construction spending report can be largely attributed to the public sector.

Market Data | Jul 31, 2017

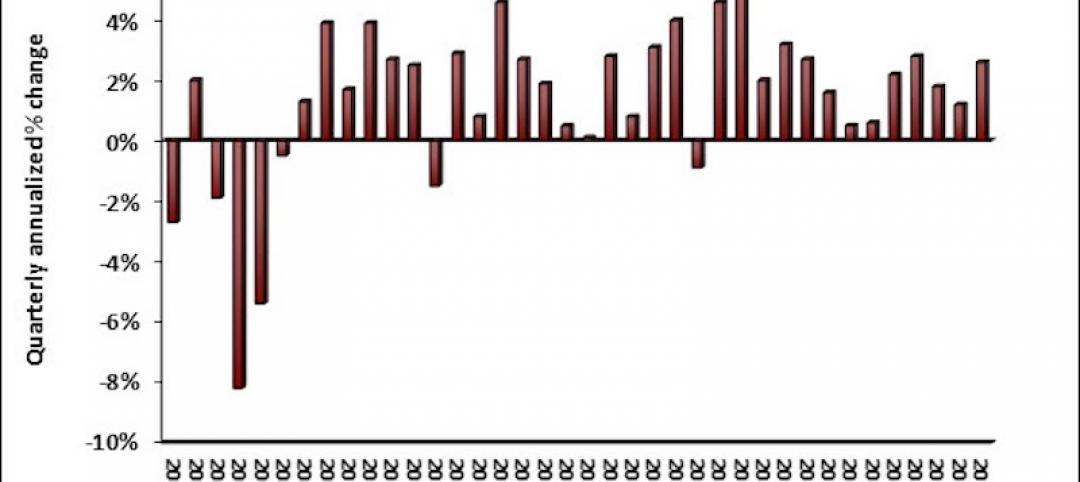

U.S. economic growth accelerates in second quarter; Nonresidential fixed investment maintains momentum

Nonresidential fixed investment, a category of GDP embodying nonresidential construction activity, expanded at a 5.2% seasonally adjusted annual rate.

Multifamily Housing | Jul 27, 2017

Apartment market index: Business conditions soften, but still solid

Despite some softness at the high end of the apartment market, demand for apartments will continue to be substantial for years to come, according to the National Multifamily Housing Council.

Market Data | Jul 25, 2017

What's your employer value proposition?

Hiring and retaining talent is one of the top challenges faced by most professional services firms.

Market Data | Jul 25, 2017

Moderating economic growth triggers construction forecast downgrade for 2017 and 2018

Prospects for the construction industry have weakened with developments over the first half of the year.

Industry Research | Jul 6, 2017

The four types of strategic real estate amenities

From swimming pools to pirate ships, amenities (even crazy ones) aren’t just perks, but assets to enhance performance.

Market Data | Jun 29, 2017

Silicon Valley, Long Island among the priciest places for office fitouts

Coming out on top as the most expensive market to build out an office is Silicon Valley, Calif., with an out-of-pocket cost of $199.22.

Market Data | Jun 26, 2017

Construction disputes were slightly less contentious last year

But poorly written and administered contracts are still problems, says latest Arcadis report.

Industry Research | Jun 26, 2017

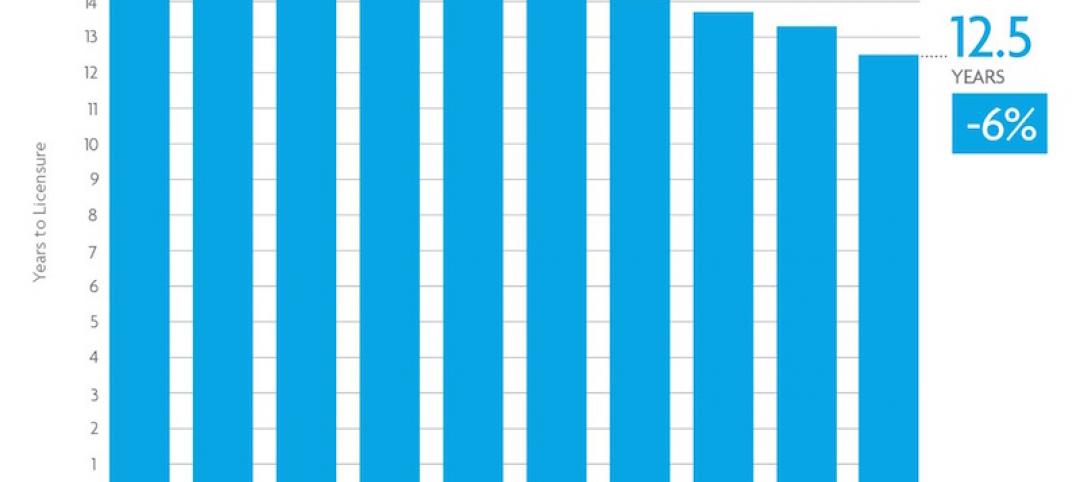

Time to earn an architecture license continues to drop

This trend is driven by candidates completing the experience and examination programs concurrently and more quickly.

Industry Research | Jun 22, 2017

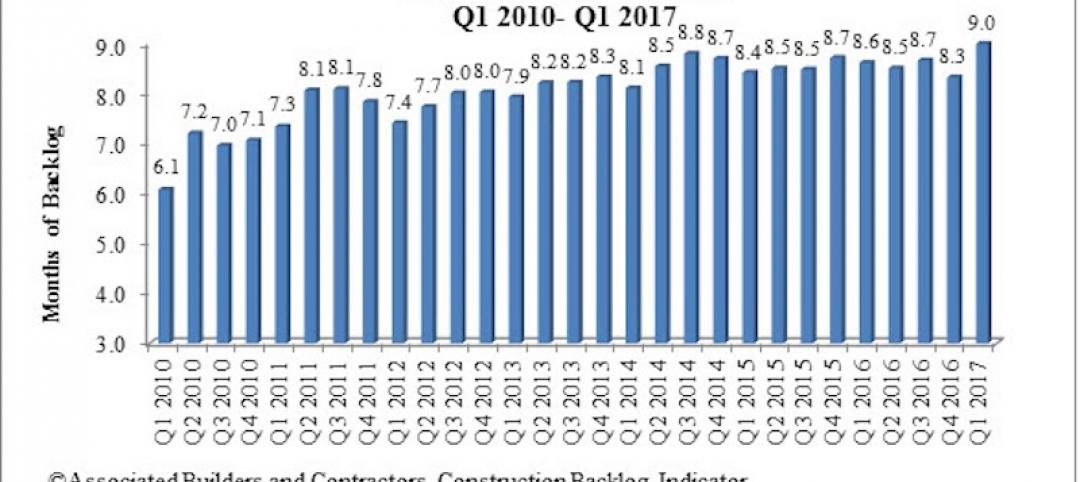

ABC's Construction Backlog Indicator rebounds in 2017

The first quarter showed gains in all categories.