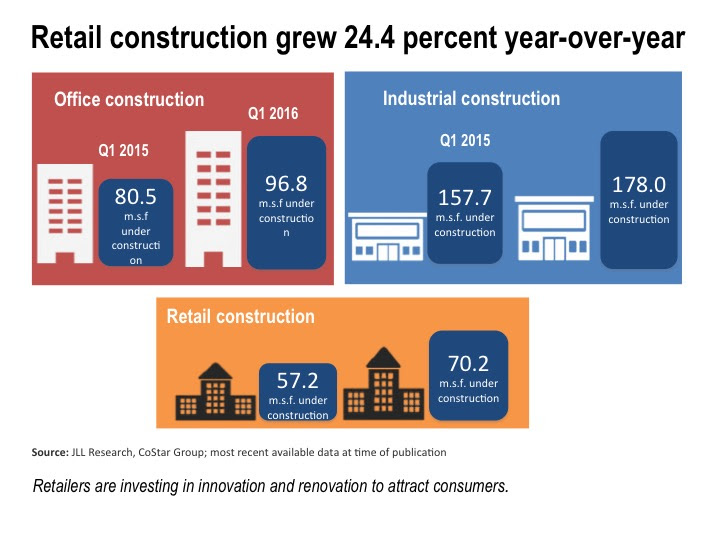

A strong retail sector has helped drive 2016 U.S. construction activity with retail construction projects up 24.4% year-over-year. Overshadowing the good news is a cloud of economic uncertainty that has companies laser-focused on lean budgeting and smart spending decisions.

According to JLL’s latest report on non-residential construction activity, U.S. construction employment grew 4.7% in the first quarter of 2016 over the first quarter of 2015, with many workers engaged on retail projects. Concerns about China’s steep economic deceleration, combined with a drop in U.S. gross domestic product (GDP) from 1.4% in the fourth quarter of 2015 to 0.5% in the first quarter of 2016, have made companies reluctant to invest.

The market for commercial construction remains active for now. The JLL report shows a strong first quarter with steady growth projected for second quarter. The office, industrial and retail sectors are very active as companies continue projects that broke ground a year or two ago. A hint of the economic clouds causing concern comes from a small decline in office construction starts.

“Developers and occupiers are proceeding with caution, but they continue to build and renovate,” explains Todd Burns, President, Project and Development Services, JLL Americas. “However, project sponsors today are thinking more strategically about development versus renovation. The best-managed companies have learned to keep their capital spend within about two% of the plan by starting with a realistic budget, leveraging data and analytical platforms, and putting the right skills together in a centralized project team.”

Key sectors to watch

Retail: Retail vacancies continue to decline, and retail has surged ahead of other property types in construction activity. Construction grew 24.4% year over year, from 57.2 million sf in first.

Industrial: Industrial facility deliveries grew year-over-year in Q1 2016, reflecting the continuing strength in demand for modern industrial properties—much of it from retailers and e-commerce companies striving to meet changing consumer demand and service requirements. Construction grew 12.9%, from 157.7 million sf in Q1 2015 to 178 million sf in Q1 2016.

Office: Office building construction grew by 20.2 year-over-year, from 80.5 million sf to 96.8 million sf—but starts declined by 33%, from 20.3 million to 13.6 million, reflecting economic concerns and hesitancy to launch new projects.

Retail innovation and renovation

Much of the retail construction growth in Q1 2016 has come from renovation, rather than new deliveries, as retailers are evolving to meet consumers’ ever-growing expectations for unified online and brick-and-mortar experiences.

“Retailers must innovate quickly to capture the untapped needs and expectations of consumers, who expect the same brand experience whether shopping online or in the brick-and-mortar store,” said Aaron Spiess, co-founder of Big Red Rooster, JLL’s brand experience company. “If retailers wait too long to translate latent customer expectations into new stores or renovation programs, they may find that customers have become entrenched with competing brands and are not going to return.”

Another incentive to renovate, notes Spiess, is a new federal tax break providing “safe harbor” for some remodeling expenses. Eligible retailers and restaurants can reduce 75% of qualifying expenses with the remaining 25% capitalized and depreciated over time.

Key markets to watch

Nashville: The Southeast saw an uptick in office, industrial and retail construction in the last year. Nashville, in particular, has seen rapid construction growth and low vacancy rates as employers take advantage of the city’s low-cost, well-educated workforce.

San Francisco: The Bay area is catching up to New York in of construction costs, driven by high demand and high labor costs. San Francisco is on pace to exceed New York as the U.S.’ most expensive construction market in 2016.

Dallas: As retailers followed population flows to Texas, Dallas has become one of the few markets that experienced retail development growth. Dallas was the most active retail market in Q1, up nearly 80% year over year.

Related Stories

Market Data | Jun 12, 2019

Construction input prices see slight increase in May

Among the 11 subcategories, six saw prices fall last month, with the largest decreases in natural gas.

Market Data | Jun 3, 2019

Nonresidential construction spending up 6.4% year over year in April

Among the 16 sectors tracked by the U.S. Census Bureau, nine experienced an increase in monthly spending, led by water supply and highway and street.

Market Data | Jun 3, 2019

4.1% annual growth in office asking rents above five-year compound annual growth rate

Market has experienced no change in office vacancy rates in three quarters.

Market Data | May 30, 2019

Construction employment increases in 250 out of 358 metros from April 2018 to April 2019

Demand for work is outpacing the supply of workers.

Market Data | May 24, 2019

Construction contractors confidence remains high in March

More than 70% of contractors expect to increase staffing levels over the next six months.

Market Data | May 22, 2019

Slight rebound for architecture billings in April

AIA’s ABI score for April showed a small increase in design services at 50.5 in April.

Market Data | May 9, 2019

The U.S. hotel construction pipeline continues to grow in the first quarter as the economy shows surprising strength

Projects currently under construction stand at 1,709 projects/227,924 rooms.

Market Data | May 9, 2019

Construction input prices continue to rise

Nonresidential input prices rose 0.9% compared to March and are up 2.8% on an annual basis.

Market Data | May 7, 2019

Construction costs in major metros continued to climb last year

Latest Rider Levett Bucknall report estimates rise at more than double the rate of 2018 Growth Domestic Product.

Market Data | Apr 29, 2019

U.S. economic growth crosses 3% threshold to begin the year

Growth was fueled by myriad factors, including personal consumption expenditures, private inventory investment, surprisingly rapid growth in exports, state and local government spending and intellectual property.