Construction costs are expected to increase by around 6 percent in 2021, and grow by another 4 to 7 percent in 2021, according to JLL’s Construction Cost Outlook for the second half of this year.

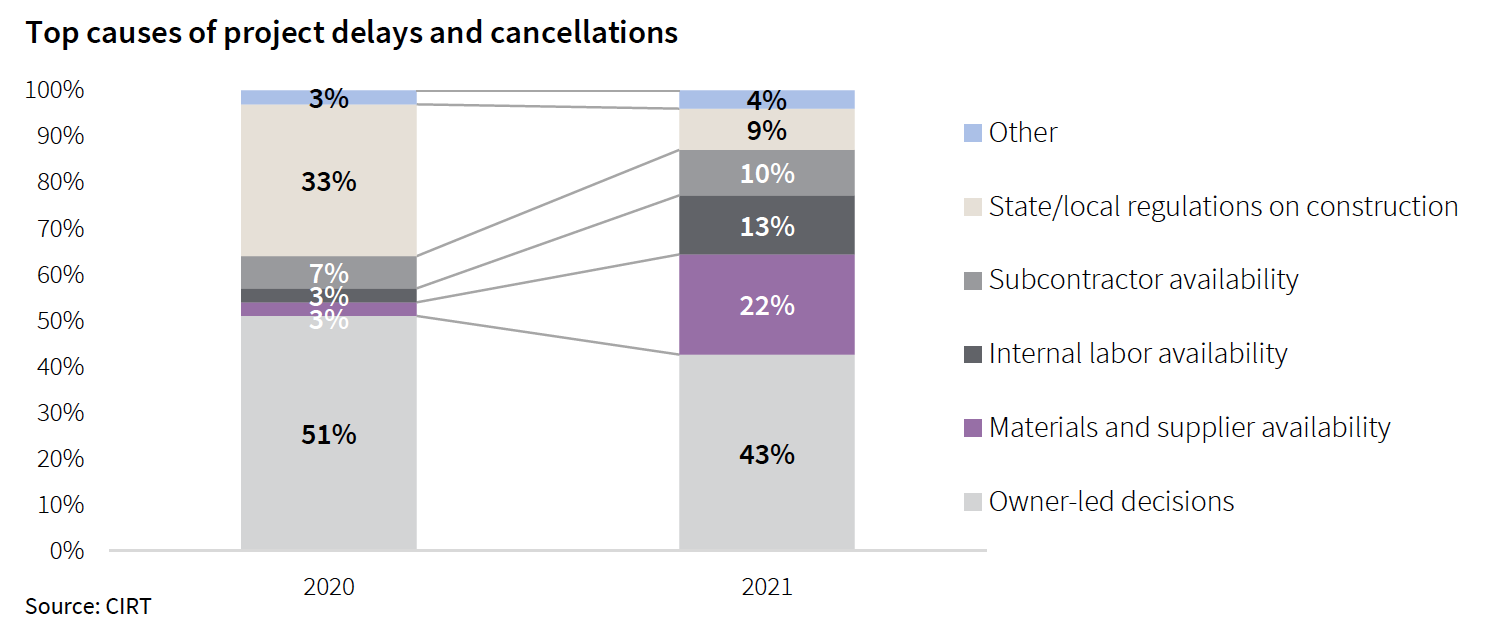

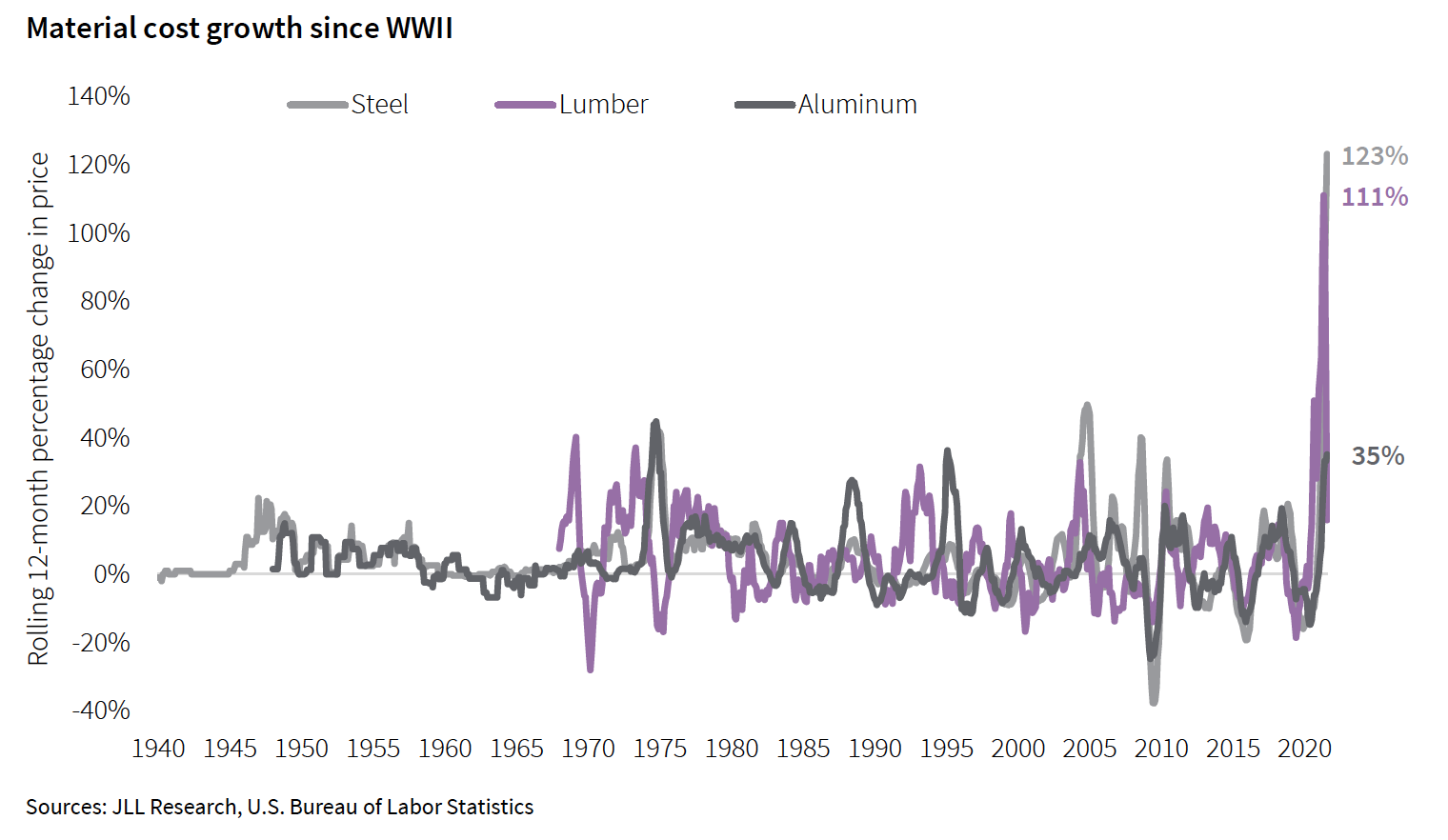

The Outlook tracks what has been “unprecedented” volatility in materials prices, which for the 12 months through August 2021 soared by 23 percent. Over that same period, labor costs rose by 4.46 percent, bringing total construction costs up by 4.51 percent. “The lack of available labor has led to more project delays so far in 2021 than a lack of materials, and conditions are expected to worsen over the coming year,” states Henry Esposito, JLL’s Construction Research Lead and the Outlook’s author.

Construction cost gains are occurring at a time when nonresidential construction spending was down by 9.5 percent for the 12 months through July 2021. JLL does not expect a “true” rebound in that spending until the Spring or Summer of next year. And don’t count on any immediate jolt from the federal infrastructure bill that, even if it passes, won’t impact construction spending or costs for two to six years out.

Construction recovery also faces two big immediate challenges:

Supply chain delays and record-high cost increases continue to put pressure on project execution and profitability. And the delta variant and future waves of the pandemic have the potential to slow economic growth, weakening the construction rebound “and calling into question some of the rosier predictions for 2022.” The Outlook states.

SHORTAGES AND DELAYS WILL CONTINUE THROUGH ‘22

As demand for new projects continues to grow and contractor backlogs fill, there will be less incentive to bid aggressively, and contractors will aim to pass through cost increases to owners as soon as the market can bear it. This combination of factors leads JLL to extend its forecasts for 4.5 to 7.5 percent final cost growth for nonresidential construction in calendar year 2021 and to predict a similar 4 to 7 percent cost growth range for 2022.

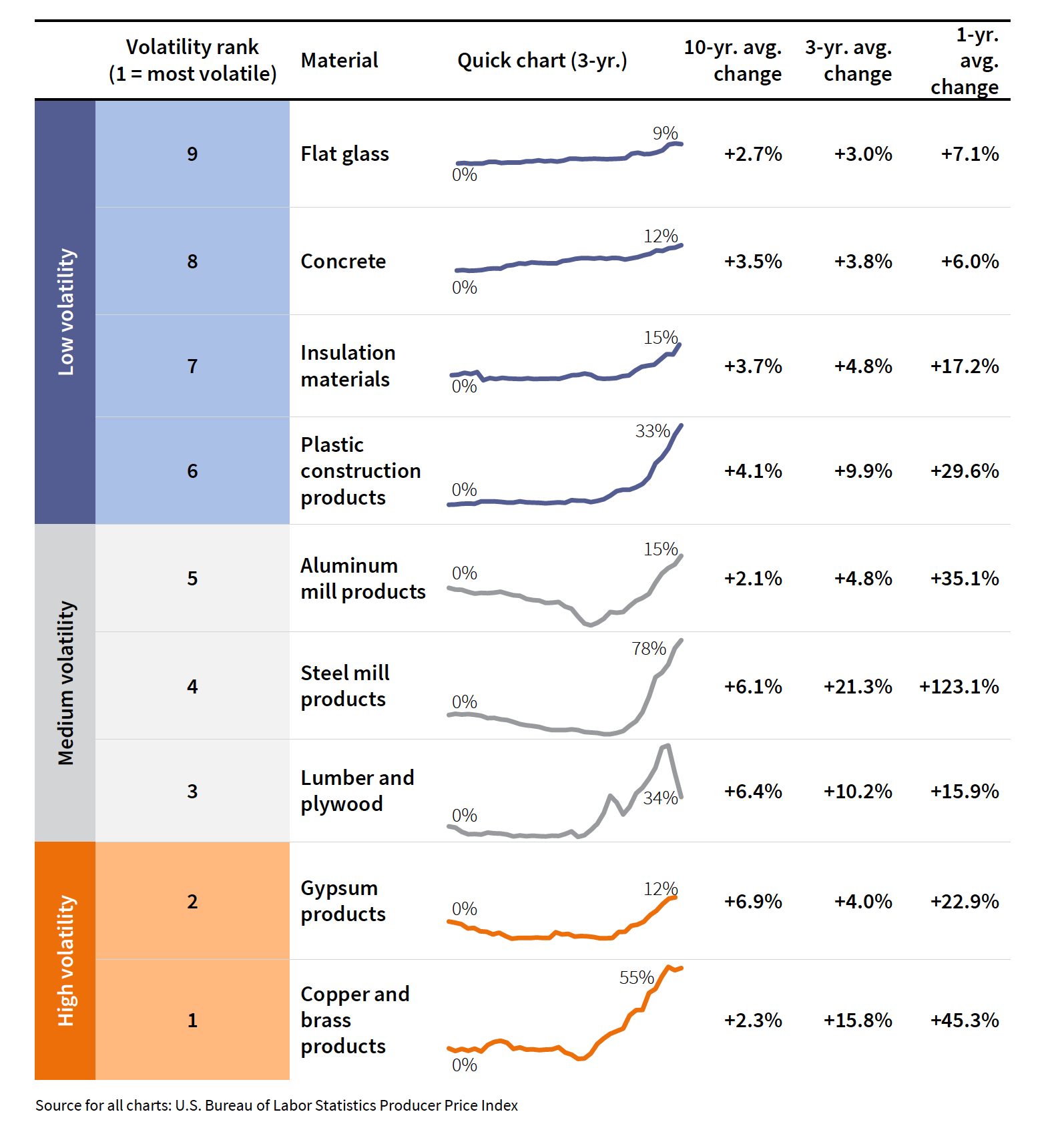

Some materials costs will ease, but the average increase will land somewhere between 5 and 11 percent. Aside from costs, the most pressing issues for most construction materials right now are lead times and delays. “Hopes for major relief during 2021 have been largely dashed, with hope for a return to normal now pushed out into 2022,” says JLL. The most pressing development might be the recent coup d’état in Guinea, which is one the world’s largest exporters of bauxite, the ore needed to produce aluminum.

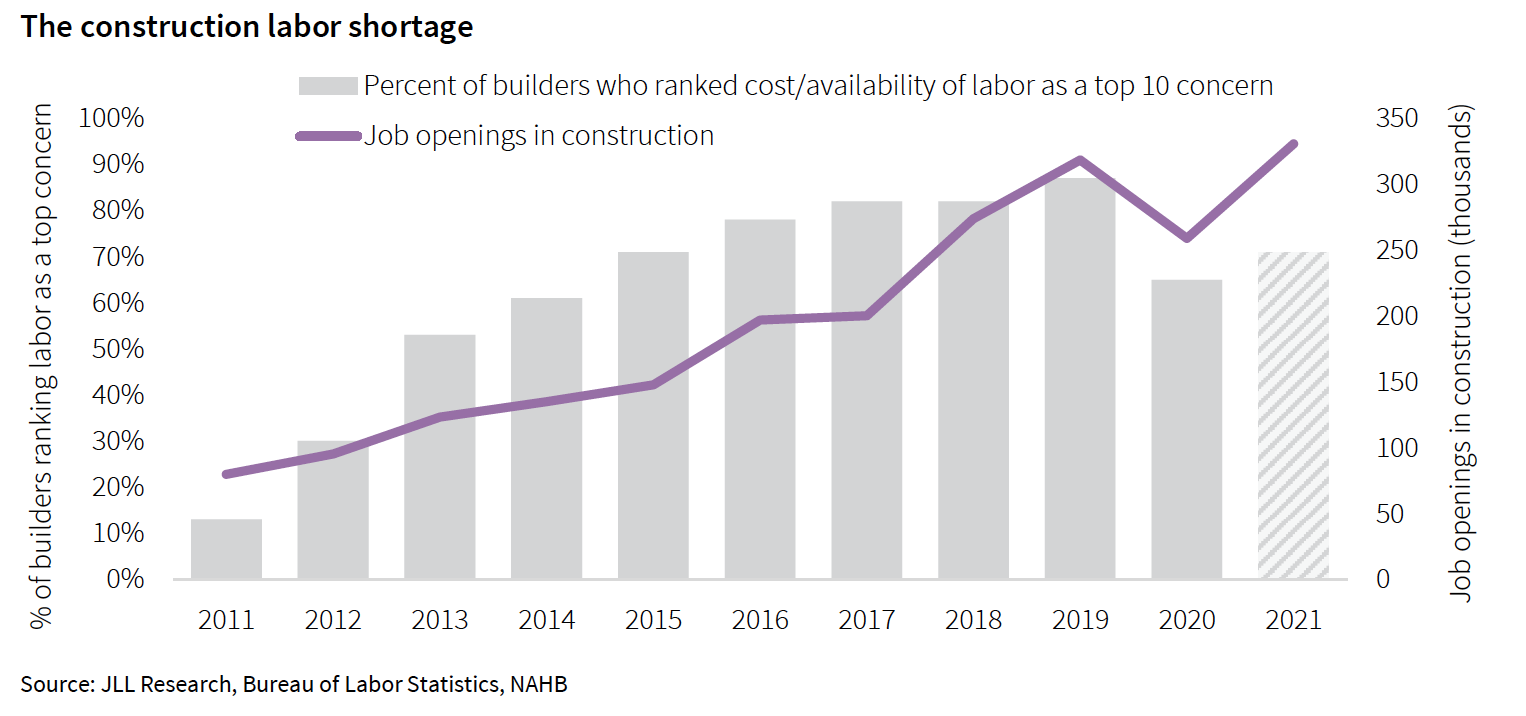

The industry’s labor shortage isn’t abating, either. From 2015 to 2019, the number of open and unfilled jobs in construction across the country doubled to 300,000. And while construction was one of the fastest sectors to recover from the pandemic, its workforce numbers still fall far short of demand, which is why JLL expects labor costs to grow in the 3 to 6 percent range. Construction also has the lowest vaccination rate, and the highest vaccine hesitancy rate, of any major industry, so jobsite workers remain more vulnerable to airborne infection that might sideline them.

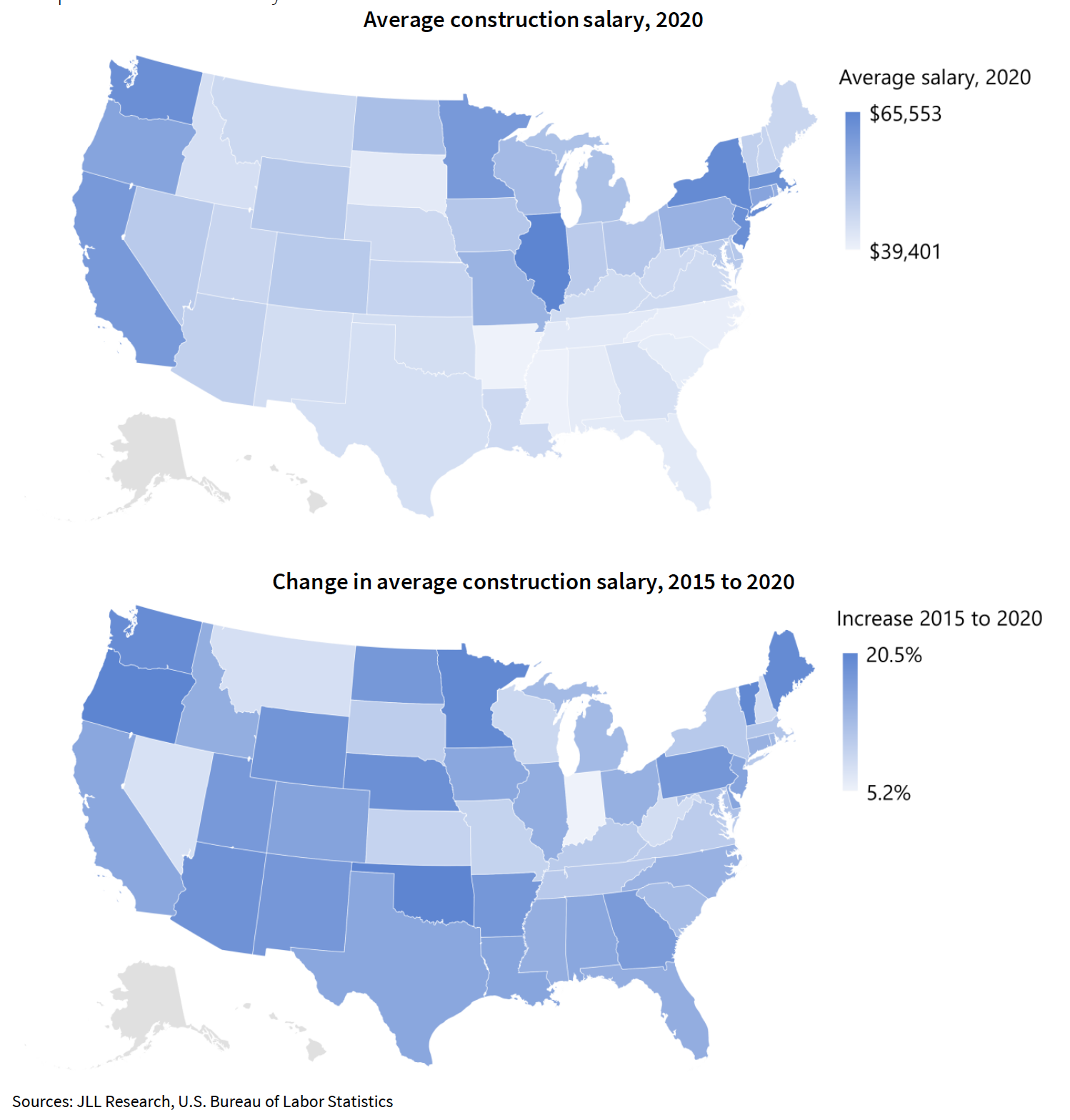

JLL shows that high-wage states are clustered in the Northeast corridor and the West Coast. The Midwest is also a high-cost region, with Illinois standing out as the top state, while the entire Southeast is the cheapest area of the country to hire workers. Wage growth across the country, on the other hand, is more evenly distributed, and some of the top states in total wages—such as Illinois, New York, and California—are only in the middle of the distribution pack.

Related Stories

Market Data | Feb 5, 2020

Construction employment increases in 211 out of 358 metro areas from December 2018 to 2019

Dallas-Plano-Irving, Texas and Kansas City have largest gains; New York City and Fairbanks, Alaska lag the most as labor shortages likely kept firms in many areas from adding even more workers.

Market Data | Feb 4, 2020

Construction spending dips in December as nonresidential losses offset housing pickup

Homebuilding strengthens but infrastructure and other nonresidential spending fades in recent months, reversing pattern in early 2019.

Market Data | Feb 4, 2020

IMEG Corp. acquires Clark Engineering

Founded in 1938 in Minneapolis, Clark Engineering has an extensive history of public and private project experience.

Market Data | Jan 30, 2020

U.S. economy expands 2.1% in 4th quarter

Investment in structures contracts.

Market Data | Jan 30, 2020

US construction & real estate industry sees a drop of 30.4% in deal activity in December 2019

A total of 48 deals worth $505.11m were announced in December 2019.

Market Data | Jan 29, 2020

Navigant research report finds global wind capacity value is expected to increase tenfold over the next decade

Wind power is being developed in more countries as well as offshore and onshore.

Market Data | Jan 28, 2020

What eight leading economists predict for nonresidential construction in 2020 and 2021

Public safety, education, and healthcare highlight a market that is entering growth-slowdown mode, but no downturn is projected, according to AIA's latest Consensus Construction Forecast panel.

Market Data | Jan 28, 2020

Los Angeles has the largest hotel construction pipeline in the United States

Los Angeles will have a growth rate of 2.5% with 19 new hotels/2,589 rooms opening.

Market Data | Jan 27, 2020

U.S. hotel construction pipeline finishes 2019 trending upward

Projects under construction continue to rise reaching an all-time high of 1,768 projects.

Market Data | Jan 24, 2020

U.S. Green Building Council releases the top 10 states for LEED

Colorado leads the nation, showing how LEED green buildings support climate action and a better quality of life.