Construction costs are expected to increase by around 6 percent in 2021, and grow by another 4 to 7 percent in 2021, according to JLL’s Construction Cost Outlook for the second half of this year.

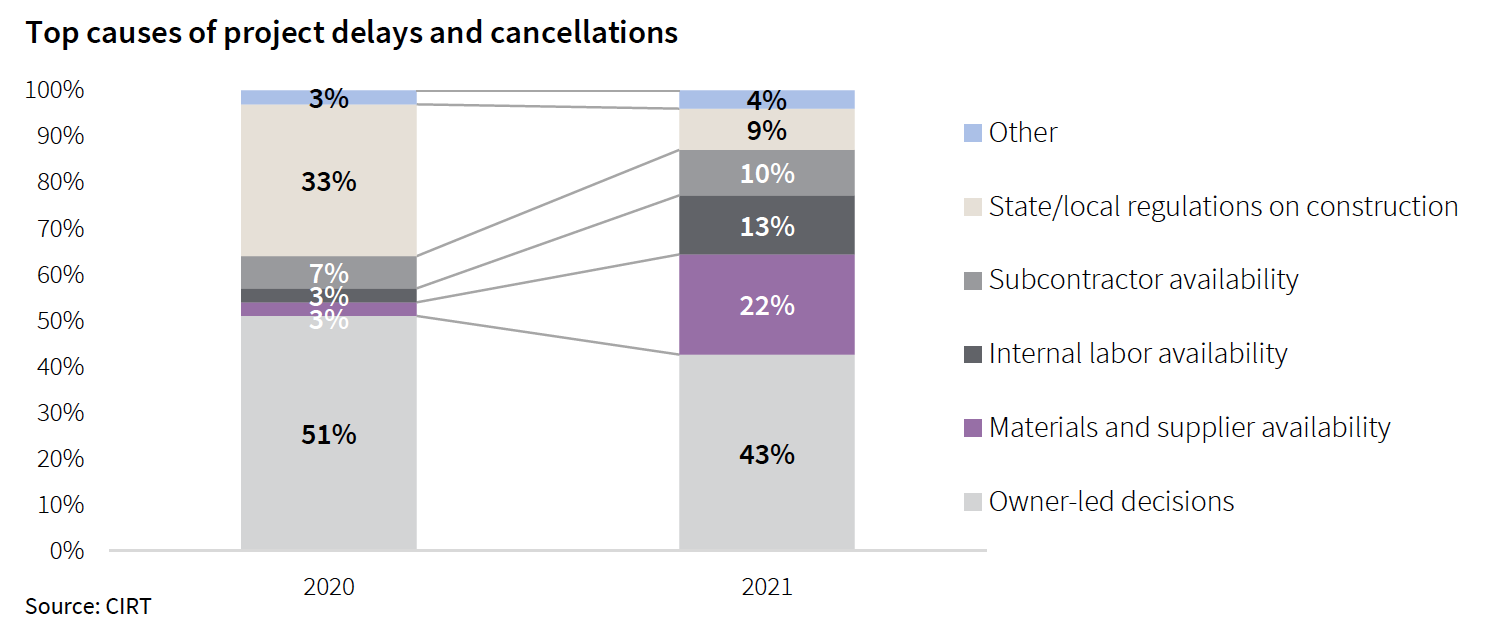

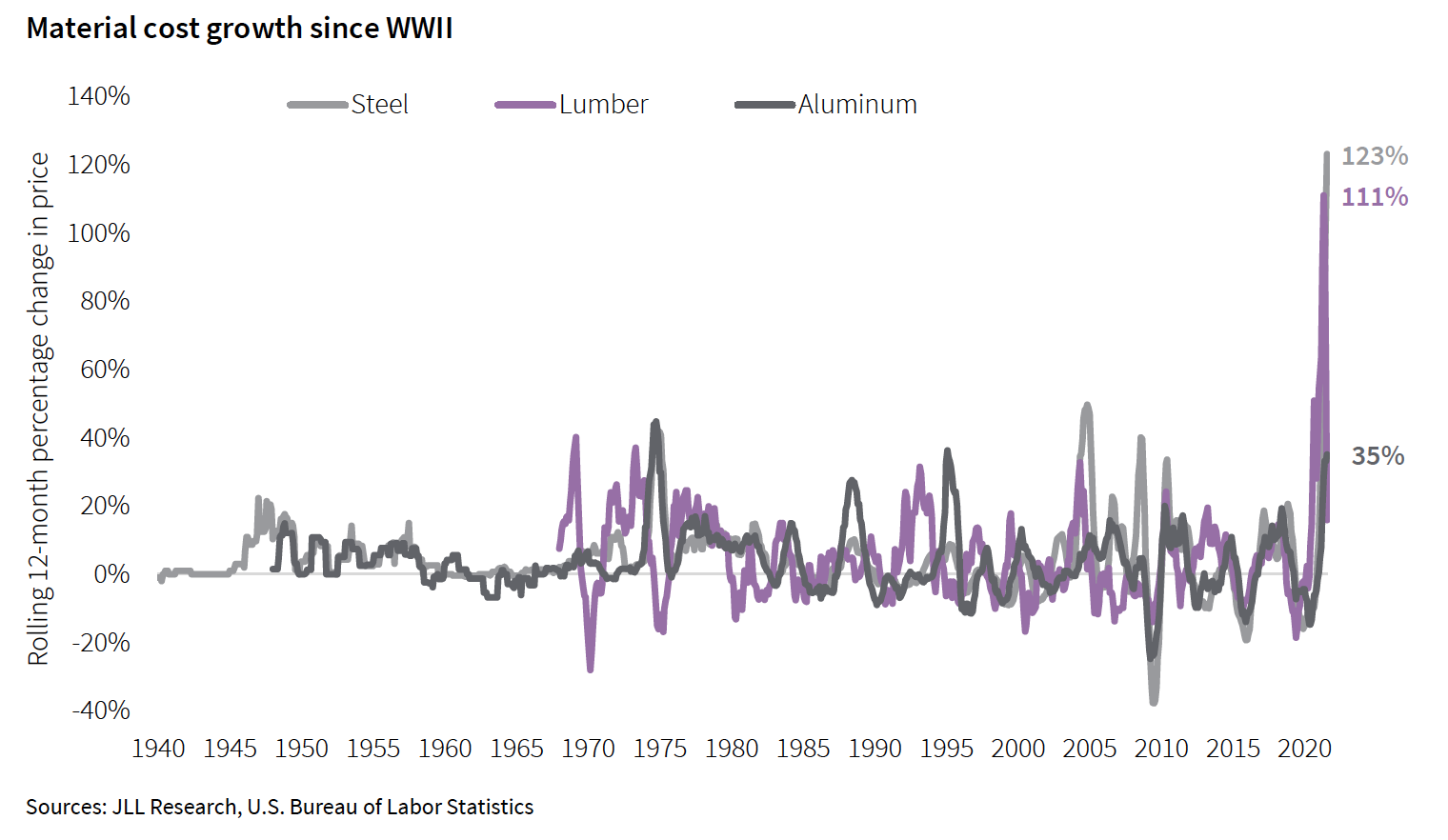

The Outlook tracks what has been “unprecedented” volatility in materials prices, which for the 12 months through August 2021 soared by 23 percent. Over that same period, labor costs rose by 4.46 percent, bringing total construction costs up by 4.51 percent. “The lack of available labor has led to more project delays so far in 2021 than a lack of materials, and conditions are expected to worsen over the coming year,” states Henry Esposito, JLL’s Construction Research Lead and the Outlook’s author.

Construction cost gains are occurring at a time when nonresidential construction spending was down by 9.5 percent for the 12 months through July 2021. JLL does not expect a “true” rebound in that spending until the Spring or Summer of next year. And don’t count on any immediate jolt from the federal infrastructure bill that, even if it passes, won’t impact construction spending or costs for two to six years out.

Construction recovery also faces two big immediate challenges:

Supply chain delays and record-high cost increases continue to put pressure on project execution and profitability. And the delta variant and future waves of the pandemic have the potential to slow economic growth, weakening the construction rebound “and calling into question some of the rosier predictions for 2022.” The Outlook states.

SHORTAGES AND DELAYS WILL CONTINUE THROUGH ‘22

As demand for new projects continues to grow and contractor backlogs fill, there will be less incentive to bid aggressively, and contractors will aim to pass through cost increases to owners as soon as the market can bear it. This combination of factors leads JLL to extend its forecasts for 4.5 to 7.5 percent final cost growth for nonresidential construction in calendar year 2021 and to predict a similar 4 to 7 percent cost growth range for 2022.

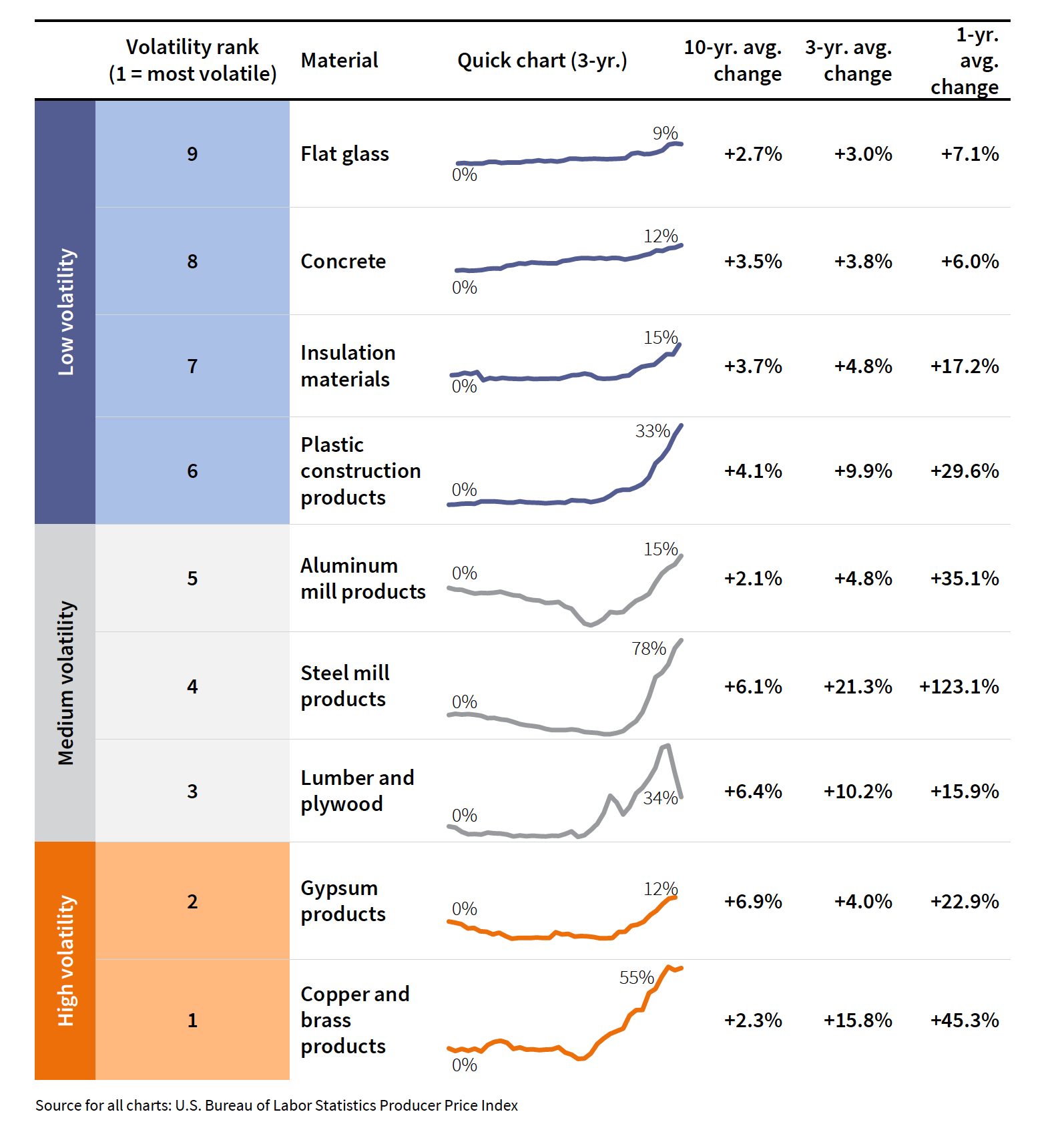

Some materials costs will ease, but the average increase will land somewhere between 5 and 11 percent. Aside from costs, the most pressing issues for most construction materials right now are lead times and delays. “Hopes for major relief during 2021 have been largely dashed, with hope for a return to normal now pushed out into 2022,” says JLL. The most pressing development might be the recent coup d’état in Guinea, which is one the world’s largest exporters of bauxite, the ore needed to produce aluminum.

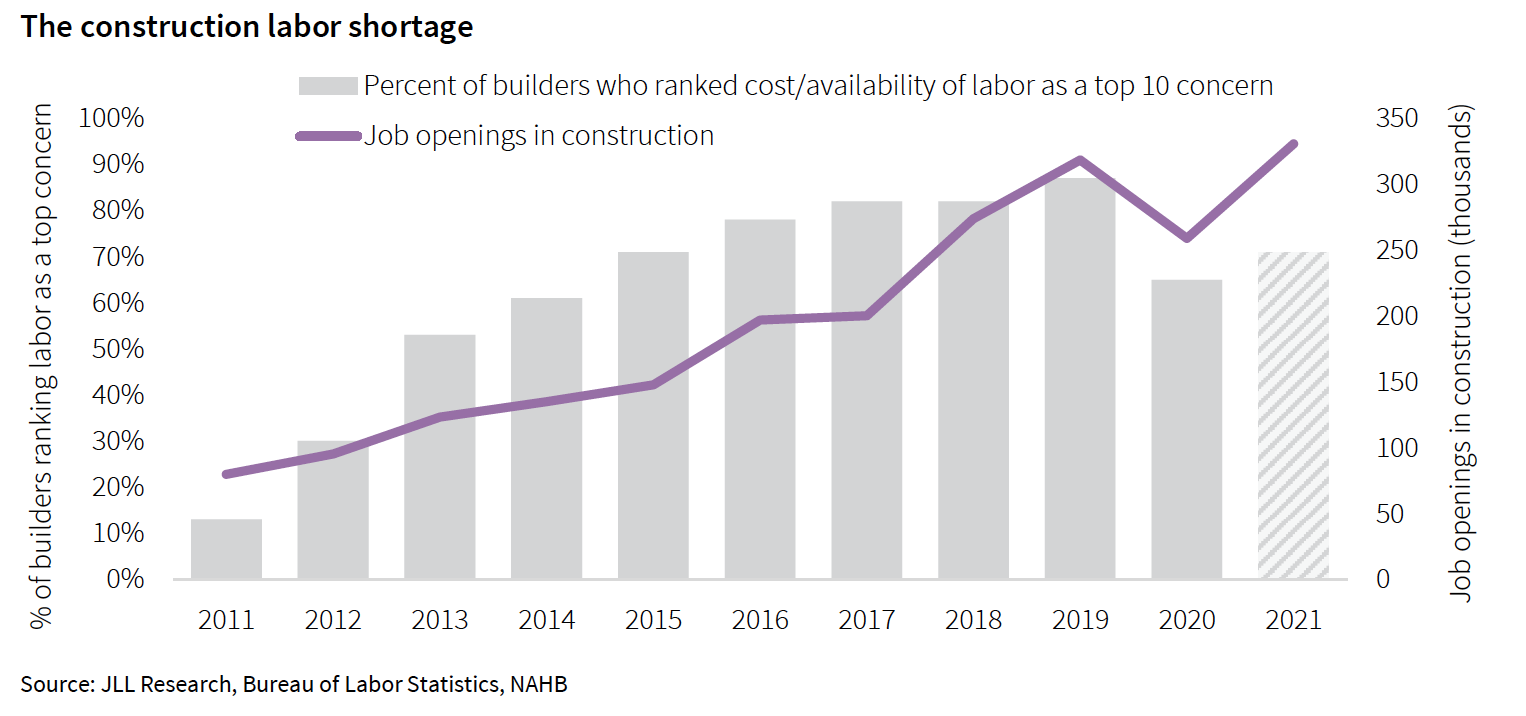

The industry’s labor shortage isn’t abating, either. From 2015 to 2019, the number of open and unfilled jobs in construction across the country doubled to 300,000. And while construction was one of the fastest sectors to recover from the pandemic, its workforce numbers still fall far short of demand, which is why JLL expects labor costs to grow in the 3 to 6 percent range. Construction also has the lowest vaccination rate, and the highest vaccine hesitancy rate, of any major industry, so jobsite workers remain more vulnerable to airborne infection that might sideline them.

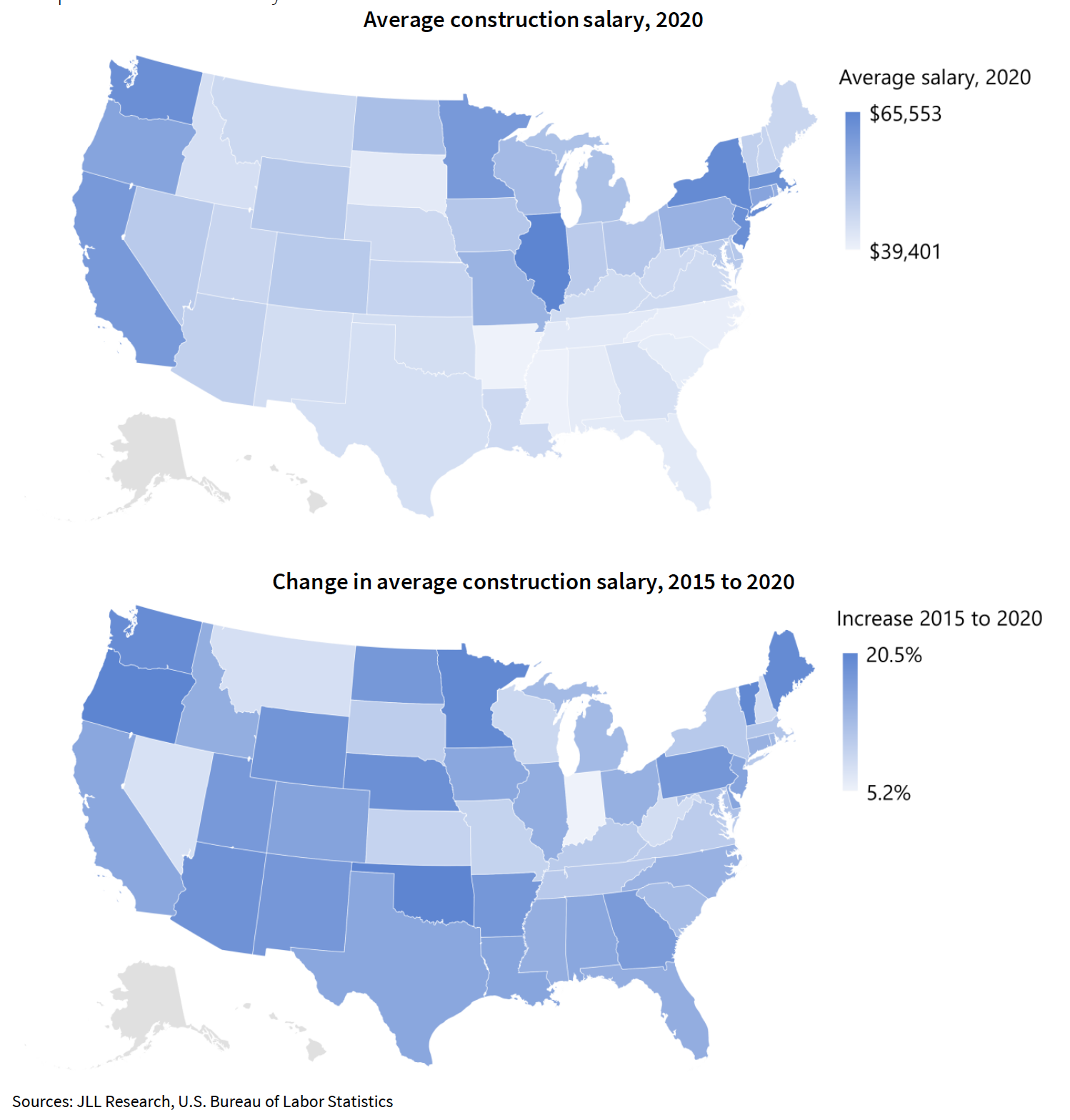

JLL shows that high-wage states are clustered in the Northeast corridor and the West Coast. The Midwest is also a high-cost region, with Illinois standing out as the top state, while the entire Southeast is the cheapest area of the country to hire workers. Wage growth across the country, on the other hand, is more evenly distributed, and some of the top states in total wages—such as Illinois, New York, and California—are only in the middle of the distribution pack.

Related Stories

Market Data | Oct 31, 2016

Nonresidential fixed investment expands again during solid third quarter

The acceleration in real GDP growth was driven by a combination of factors, including an upturn in exports, a smaller decrease in state and local government spending and an upturn in federal government spending, says ABC Chief Economist Anirban Basu.

Market Data | Oct 28, 2016

U.S. construction solid and stable in Q3 of 2016; Presidential election seen as influence on industry for 2017

Rider Levett Bucknall’s Third Quarter 2016 USA Construction Cost Report puts the complete spectrum of construction sectors and markets in perspective as it assesses the current state of the industry.

Industry Research | Oct 25, 2016

New HOK/CoreNet Global report explores impact of coworking on corporate real rstate

“Although coworking space makes up less than one percent of the world’s office space, it represents an important workforce trend and highlights the strong desire of today’s employees to have workplace choices, community and flexibility,” says Kay Sargent, Director of WorkPlace at HOK.

Market Data | Oct 24, 2016

New construction starts in 2017 to increase 5% to $713 billion

Dodge Outlook Report predicts moderate growth for most project types – single family housing, commercial and institutional building, and public works, while multifamily housing levels off and electric utilities/gas plants decline.

High-rise Construction | Oct 21, 2016

The world’s 100 tallest buildings: Which architects have designed the most?

Two firms stand well above the others when it comes to the number of tall buildings they have designed.

Market Data | Oct 19, 2016

Architecture Billings Index slips consecutive months for first time since 2012

“This recent backslide should act as a warning signal,” said AIA Chief Economist, Kermit Baker.

Market Data | Oct 11, 2016

Building design revenue topped $28 billion in 2015

Growing profitability at architecture firms has led to reinvestment and expansion

Market Data | Oct 4, 2016

Nonresidential spending slips in August

Public sector spending is declining faster than the private sector.

Industry Research | Oct 3, 2016

Structure Tone survey shows cost is still a major barrier to building green

Climate change, resilience and wellness are also growing concerns.

Industry Research | Sep 27, 2016

Sterling Risk Sentiment Index indicates risk exposure perception remains stable in construction industry

Nearly half (45%) of those polled say election year uncertainty has a negative effect on risk perception in the construction market.