Cap rates for real estate across most asset sectors is expected to remain stable in the second half of 2015, following a first half during which the U.S. commercial real estate market continued to perform well and attract substantial investor interest.

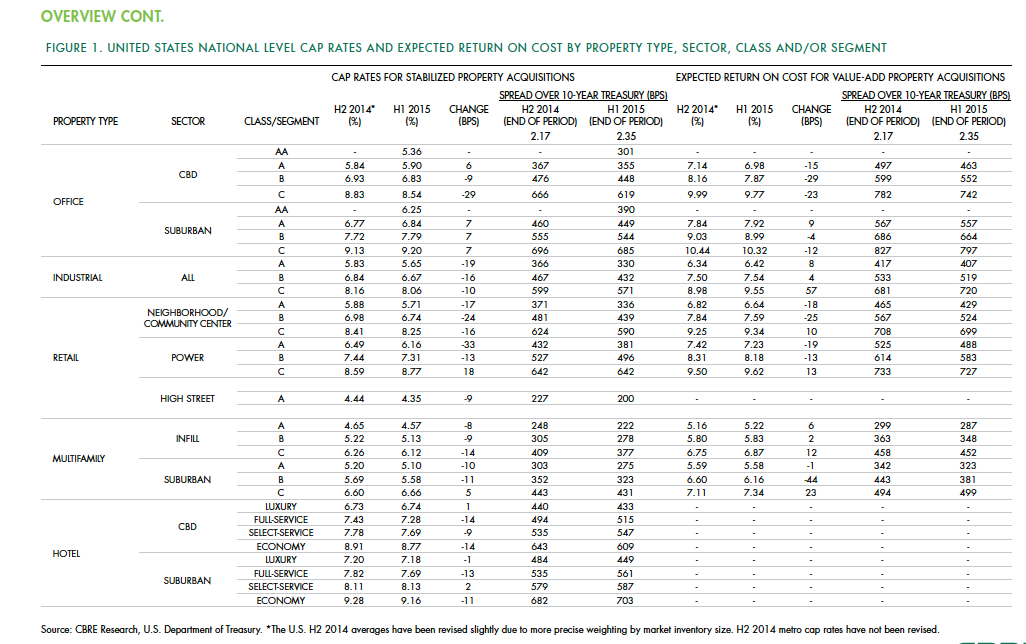

According to the CBRE North America Cap Rate Survey, which tracks activity in 46 major U.S. markets and 10 markets in Canada during the first six months of the year, national cap rates for industrial facilities in the U.S. experienced “very modest” cap-rate declines of 10 to 19 basis points. CBRE estimates that cap rates for stabilized Class A industrial assets was 5.65%.

Class A infill multifamily cap rates were 4.57% in the first half of the year, the second-lowest of all product types. The retail sector had the most significant national cap rate compression, followed by hotels. CBRE suggests that retail and hotels were the sectors that took the longest to recover from the past recession, “therefore, it is not surprising that the cap rate declines are greater in these sectors than those more mature in the real estate cycle.”

Central Business District Class B and C office cap rates were slightly off in the first half, but not Class A offices, “one example of investors moving out of on the risk curve,” CBRE notes. And despite sales volume gains, suburban office cap rates rose, on average, by 7 basis points.

Details from this report, as well as CBRE’s near-term predictions, include the following:

• Interest rates, a big demand driver in the commercial real estate space, are expected to rise modestly. The 10-year Treasury is projected to increase to 2.61% in the second half of 2015, and to 3.19% in 2016. However, “the near-term outlook of higher interest rates is not necessarily going to translate into higher cap rates if the rates come from stronger economic growth, as expected, as opposed to an unexpected shock to the economic system,” CBRE writes.

• CRBE doesn’t expect any cap rate movement in the second half of 2015 for office assets in the majority of markets, and only modest declines in those asset classes that do change. Jacksonville and Cincinnati are expected to experience the largest cap rate declines in Class A acquisitions.

• Transaction activity in the U.S. industrial sector during the first half of 2015 rose 70% to $37 billion. CBRE expects the full-year gain over 2014 to be 40% or greater. Cap rates in this sector are expected to fall modestly in more than one-third of the markets surveyed. Larger declines of 25 basis points or more are expected in Class B and C stabilized properties in Philadelphia and St. Louis. On the other hand, 58% of the market surveyed should experience no change to stabilized industrial cap rates.

• Retail investment in the first half of 2015 rose 12% to $45.6 billion. The “mall and other” category in this sector grew by 14%. CBRE expects investment to accelerate modestly through the remainder of the year. As far as cap rates are concerned, Class B experienced the largest average decline of 24 basis points. And four markets—San Jose, San Francisco, Los Angeles, and Orange County, Calif.—all had Class A caps under 5%.

• In the first six months of 2015, sales of multifamily properties jumped 38% to 63.2 billion. One-third of that capital went to mid- and high-rise projects. For Class A infill assets, San Francisco had the lowest cap rate, at 3.75%. Of the 44 markets surveyed in this sector, 33 had cap rates of 5% or less. CRBE is predicting no cap rate change for acquisitions of stabilized infill multifamily assets in the second half of the year for more than 80% of the markets surveyed. But cap compression should occur in Nashville, Washington D.C., Baltimore, Indianapolis, and Detroit.

• Investment in U.S. hotels, at $26.9 billion, was 67% higher than in the first half of 2014. The vast majority of hotel investors are domestic, especially outside of major cities. CBRE suggests, though, that hotel pricing, as measured by cap rates, has peaked for high-end products in top-tier markets. “But it’s too early to definitively make that call,” it writes. CRBE expects cap rates for acquisitions of stabilized hotel properties to remain “broadly stable” in the second half of 2015, with 62% of markets tracked experiencing no change. Any noticeable compression is likely to occur in Tier I metros like Las Vegas and Orlando, and Tier III markets such as Tampa, Jacksonville, Austin, and Pittsburgh.

Related Stories

Mixed-Use | Sep 20, 2023

Tampa Bay Rays, Hines finalize deal for a stadium-anchored multiuse district in St. Petersburg, Fla.

The Tampa Bay Rays Major League Baseball team announced that it has reached an agreement with St. Petersburg and Pinellas County on a $6.5 billion, 86-acre mixed-use development that will include a new 30,000-seat ballpark and an array of office, housing, hotel, retail, and restaurant space totaling 8 million sf.

Giants 400 | Sep 18, 2023

Top 90 Office Building Engineering Firms for 2023

Jacobs, WSP, Alfa Tech, and AECOM head BD+C's ranking of the nation's largest office building sector engineering and engineering/architecture (EA) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report. Note: This ranking includes revenue for all office building work, including core and shell projects and workplace/interior fitouts.

Giants 400 | Sep 18, 2023

Top 120 Office Building Construction Firms for 2023

Turner Construction, STO Building Group, AECOM, and DPR Construction top BD+C's ranking of the nation's largest office building sector contractors and construction management (CM) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report. Note: This ranking includes revenue for all office building work, including core and shell projects and workplace/interior fitouts.

Giants 400 | Sep 18, 2023

Top 200 Office Building Architecture Firms for 2023

Gensler, Stantec, HOK, and Interior Architects top BD+C's ranking of the nation's largest office building sector architecture and architecture/engineering (AE) firms for 2023, as reported in Building Design+Construction's 2023 Giants 400 Report. Note: This ranking includes revenue for all office building work, including core and shell projects and workplace/interior fitouts.

Adaptive Reuse | Sep 15, 2023

Salt Lake City’s Frank E. Moss U.S. Courthouse will transform into a modern workplace for federal agencies

In downtown Salt Lake City, the Frank E. Moss U.S. Courthouse is being transformed into a modern workplace for about a dozen federal agencies. By providing offices for agencies previously housed elsewhere, the adaptive reuse project is expected to realize an annual savings for the federal government of up to $6 million in lease costs.

Office Buildings | Sep 14, 2023

New York office revamp by Kohn Pedersen Fox features new façade raising occupant comfort, reducing energy use

The modernization of a mid-century Midtown Manhattan office tower features a new façade intended to improve occupant comfort and reduce energy consumption. The building, at 666 Fifth Avenue, was originally designed by Carson & Lundin. First opened in November 1957 when it was considered cutting-edge, the original façade of the 500-foot-tall modernist skyscraper was highly inefficient by today’s energy efficiency standards.

Designers | Sep 5, 2023

Optimizing interior design for human health

Page Southerland Page demonstrates how interior design influences our mood, mental health, and physical comfort.

Office Buildings | Aug 31, 2023

About 11% of U.S. office buildings could be suitable for green office-to-residential conversions

A National Bureau of Economic Research working paper from researchers at New York University and Columbia Business School indicates that about 11% of U.S. office buildings may be suitable for conversion to green multifamily properties.

Adaptive Reuse | Aug 31, 2023

New York City creates team to accelerate office-to-residential conversions

New York City has a new Office Conversion Accelerator Team that provides a single point of contact within city government to help speed adaptive reuse projects. Projects that create 50 or more housing units from office buildings are eligible for this new program.

Office Buildings | Aug 25, 2023

A new white paper explores the pros and cons of office building conversions

Produced by SGA and Colliers, the paper charts considerations for 14 building types.