Cap rates for real estate across most asset sectors is expected to remain stable in the second half of 2015, following a first half during which the U.S. commercial real estate market continued to perform well and attract substantial investor interest.

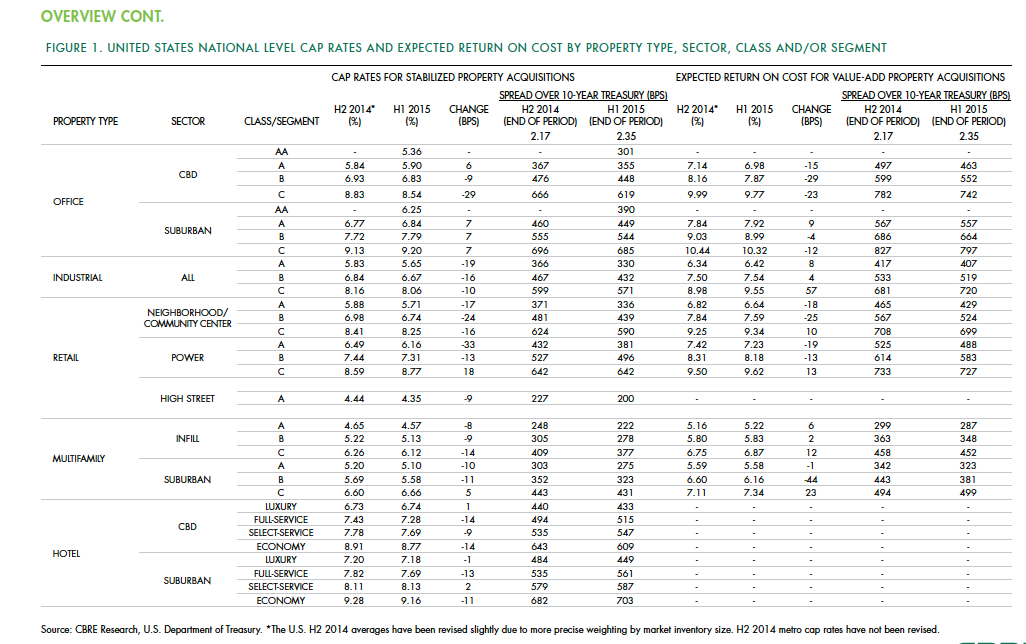

According to the CBRE North America Cap Rate Survey, which tracks activity in 46 major U.S. markets and 10 markets in Canada during the first six months of the year, national cap rates for industrial facilities in the U.S. experienced “very modest” cap-rate declines of 10 to 19 basis points. CBRE estimates that cap rates for stabilized Class A industrial assets was 5.65%.

Class A infill multifamily cap rates were 4.57% in the first half of the year, the second-lowest of all product types. The retail sector had the most significant national cap rate compression, followed by hotels. CBRE suggests that retail and hotels were the sectors that took the longest to recover from the past recession, “therefore, it is not surprising that the cap rate declines are greater in these sectors than those more mature in the real estate cycle.”

Central Business District Class B and C office cap rates were slightly off in the first half, but not Class A offices, “one example of investors moving out of on the risk curve,” CBRE notes. And despite sales volume gains, suburban office cap rates rose, on average, by 7 basis points.

Details from this report, as well as CBRE’s near-term predictions, include the following:

• Interest rates, a big demand driver in the commercial real estate space, are expected to rise modestly. The 10-year Treasury is projected to increase to 2.61% in the second half of 2015, and to 3.19% in 2016. However, “the near-term outlook of higher interest rates is not necessarily going to translate into higher cap rates if the rates come from stronger economic growth, as expected, as opposed to an unexpected shock to the economic system,” CBRE writes.

• CRBE doesn’t expect any cap rate movement in the second half of 2015 for office assets in the majority of markets, and only modest declines in those asset classes that do change. Jacksonville and Cincinnati are expected to experience the largest cap rate declines in Class A acquisitions.

• Transaction activity in the U.S. industrial sector during the first half of 2015 rose 70% to $37 billion. CBRE expects the full-year gain over 2014 to be 40% or greater. Cap rates in this sector are expected to fall modestly in more than one-third of the markets surveyed. Larger declines of 25 basis points or more are expected in Class B and C stabilized properties in Philadelphia and St. Louis. On the other hand, 58% of the market surveyed should experience no change to stabilized industrial cap rates.

• Retail investment in the first half of 2015 rose 12% to $45.6 billion. The “mall and other” category in this sector grew by 14%. CBRE expects investment to accelerate modestly through the remainder of the year. As far as cap rates are concerned, Class B experienced the largest average decline of 24 basis points. And four markets—San Jose, San Francisco, Los Angeles, and Orange County, Calif.—all had Class A caps under 5%.

• In the first six months of 2015, sales of multifamily properties jumped 38% to 63.2 billion. One-third of that capital went to mid- and high-rise projects. For Class A infill assets, San Francisco had the lowest cap rate, at 3.75%. Of the 44 markets surveyed in this sector, 33 had cap rates of 5% or less. CRBE is predicting no cap rate change for acquisitions of stabilized infill multifamily assets in the second half of the year for more than 80% of the markets surveyed. But cap compression should occur in Nashville, Washington D.C., Baltimore, Indianapolis, and Detroit.

• Investment in U.S. hotels, at $26.9 billion, was 67% higher than in the first half of 2014. The vast majority of hotel investors are domestic, especially outside of major cities. CBRE suggests, though, that hotel pricing, as measured by cap rates, has peaked for high-end products in top-tier markets. “But it’s too early to definitively make that call,” it writes. CRBE expects cap rates for acquisitions of stabilized hotel properties to remain “broadly stable” in the second half of 2015, with 62% of markets tracked experiencing no change. Any noticeable compression is likely to occur in Tier I metros like Las Vegas and Orlando, and Tier III markets such as Tampa, Jacksonville, Austin, and Pittsburgh.

Related Stories

Fire and Life Safety | Jan 9, 2023

Why lithium-ion batteries pose fire safety concerns for buildings

Lithium-ion batteries have become the dominant technology in phones, laptops, scooters, electric bikes, electric vehicles, and large-scale battery energy storage facilities. Here’s what you need to know about the fire safety concerns they pose for building owners and occupants.

Cladding and Facade Systems | Dec 20, 2022

Acoustic design considerations at the building envelope

Acentech's Ben Markham identifies the primary concerns with acoustic performance at the building envelope and offers proven solutions for mitigating acoustic issues.

Sponsored | Resiliency | Dec 14, 2022

Flood protection: What building owners need to know to protect their properties

This course from Walter P Moore examines numerous flood protection approaches and building owner needs before delving into the flood protection process. Determining the flood resilience of a property can provide a good understanding of risk associated costs.

HVAC | Dec 13, 2022

Energy Management Institute launches online tool to connect building owners with HVAC contractors

The National Energy Management Institute Inc. (NEMI) along with the Biden administration’s Better Air in Buildings website have rolled out a resource to help building owners and managers, school districts, and other officials find HVAC contractors.

Adaptive Reuse | Dec 9, 2022

What's old is new: Why you should consider adaptive reuse

While new construction allows for incredible levels of customization, there’s no denying that new buildings can have adverse impacts on the climate, budgets, schedules and even the cultural and historic fabrics of communities.

High-rise Construction | Dec 7, 2022

SOM reveals its design for Singapore’s tallest skyscraper

Skidmore, Owings & Merrill (SOM) has revealed its design for 8 Shenton Way—a mixed-use tower that will stand 63 stories and 305 meters (1,000 feet) high, becoming Singapore’s tallest skyscraper. The design team also plans to make the building one of Asia’s most sustainable skyscrapers. The tower incorporates post-pandemic design features.

Office Buildings | Dec 7, 2022

Software giant SAP opens engineering academy for its global engineering workforce

Software giant SAP has opened its new SAP Academy for Engineering on the company’s San Ramon, Calif. campus. Designed by HGA, the Engineering Academy will provide professional development opportunities for SAP’s global engineering workforce. At the Engineering Academy, cohorts from SAP offices across the globe will come together for intensive, six-month training programs.

Office Buildings | Dec 6, 2022

‘Chicago’s healthiest office tower’ achieves LEED Gold, WELL Platinum, and WiredScore Platinum

Goettsch Partners (GP) recently completed 320 South Canal, billed as “Chicago’s healthiest office tower,” according to the architecture firm. Located across the street from Chicago Union Station and close to major expressways, the 51-story tower totals 1,740,000 sf. It includes a conference center, fitness center, restaurant, to-go market, branch bank, and a cocktail lounge in an adjacent structure, as well as parking for 324 cars/electric vehicles and 114 bicycles.

Mixed-Use | Dec 6, 2022

Houston developer plans to convert Kevin Roche-designed ConocoPhillips HQ to mixed-use destination

Houston-based Midway, a real estate investment, development, and management firm, plans to redevelop the former ConocoPhillips corporate headquarters site into a mixed-use destination called Watermark District at Woodcreek.

Office Buildings | Dec 5, 2022

How to foster collaboration and inspiration for a workplace culture that does not exist (yet)

A building might not be able to “hack” innovation, but it can create the right conditions to foster connection and innovation, write GBBN's Chad Burke and Zachary Zettler.