Cap rates for real estate across most asset sectors is expected to remain stable in the second half of 2015, following a first half during which the U.S. commercial real estate market continued to perform well and attract substantial investor interest.

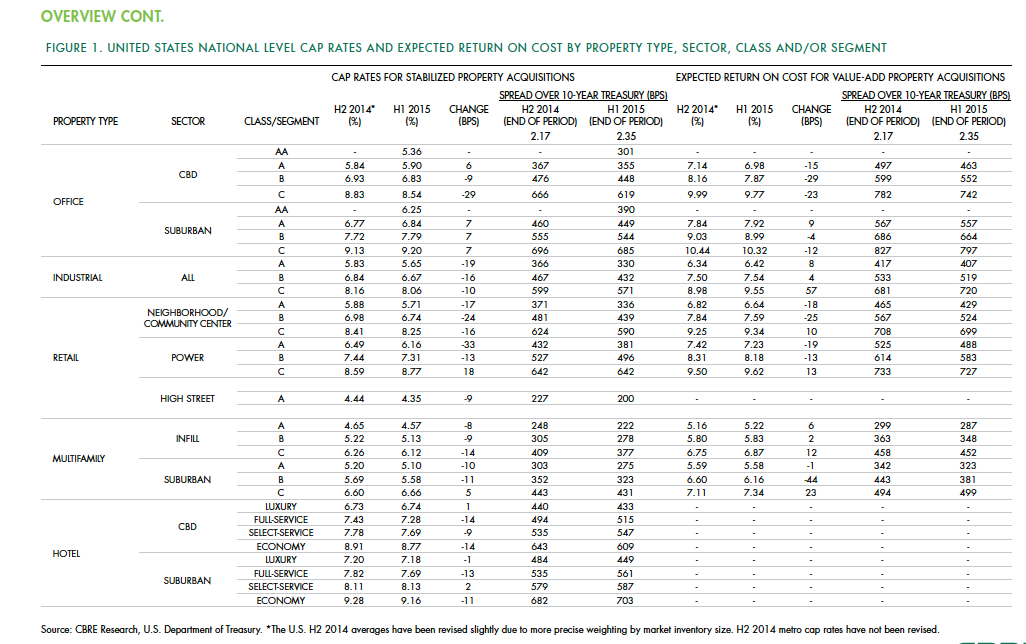

According to the CBRE North America Cap Rate Survey, which tracks activity in 46 major U.S. markets and 10 markets in Canada during the first six months of the year, national cap rates for industrial facilities in the U.S. experienced “very modest” cap-rate declines of 10 to 19 basis points. CBRE estimates that cap rates for stabilized Class A industrial assets was 5.65%.

Class A infill multifamily cap rates were 4.57% in the first half of the year, the second-lowest of all product types. The retail sector had the most significant national cap rate compression, followed by hotels. CBRE suggests that retail and hotels were the sectors that took the longest to recover from the past recession, “therefore, it is not surprising that the cap rate declines are greater in these sectors than those more mature in the real estate cycle.”

Central Business District Class B and C office cap rates were slightly off in the first half, but not Class A offices, “one example of investors moving out of on the risk curve,” CBRE notes. And despite sales volume gains, suburban office cap rates rose, on average, by 7 basis points.

Details from this report, as well as CBRE’s near-term predictions, include the following:

• Interest rates, a big demand driver in the commercial real estate space, are expected to rise modestly. The 10-year Treasury is projected to increase to 2.61% in the second half of 2015, and to 3.19% in 2016. However, “the near-term outlook of higher interest rates is not necessarily going to translate into higher cap rates if the rates come from stronger economic growth, as expected, as opposed to an unexpected shock to the economic system,” CBRE writes.

• CRBE doesn’t expect any cap rate movement in the second half of 2015 for office assets in the majority of markets, and only modest declines in those asset classes that do change. Jacksonville and Cincinnati are expected to experience the largest cap rate declines in Class A acquisitions.

• Transaction activity in the U.S. industrial sector during the first half of 2015 rose 70% to $37 billion. CBRE expects the full-year gain over 2014 to be 40% or greater. Cap rates in this sector are expected to fall modestly in more than one-third of the markets surveyed. Larger declines of 25 basis points or more are expected in Class B and C stabilized properties in Philadelphia and St. Louis. On the other hand, 58% of the market surveyed should experience no change to stabilized industrial cap rates.

• Retail investment in the first half of 2015 rose 12% to $45.6 billion. The “mall and other” category in this sector grew by 14%. CBRE expects investment to accelerate modestly through the remainder of the year. As far as cap rates are concerned, Class B experienced the largest average decline of 24 basis points. And four markets—San Jose, San Francisco, Los Angeles, and Orange County, Calif.—all had Class A caps under 5%.

• In the first six months of 2015, sales of multifamily properties jumped 38% to 63.2 billion. One-third of that capital went to mid- and high-rise projects. For Class A infill assets, San Francisco had the lowest cap rate, at 3.75%. Of the 44 markets surveyed in this sector, 33 had cap rates of 5% or less. CRBE is predicting no cap rate change for acquisitions of stabilized infill multifamily assets in the second half of the year for more than 80% of the markets surveyed. But cap compression should occur in Nashville, Washington D.C., Baltimore, Indianapolis, and Detroit.

• Investment in U.S. hotels, at $26.9 billion, was 67% higher than in the first half of 2014. The vast majority of hotel investors are domestic, especially outside of major cities. CBRE suggests, though, that hotel pricing, as measured by cap rates, has peaked for high-end products in top-tier markets. “But it’s too early to definitively make that call,” it writes. CRBE expects cap rates for acquisitions of stabilized hotel properties to remain “broadly stable” in the second half of 2015, with 62% of markets tracked experiencing no change. Any noticeable compression is likely to occur in Tier I metros like Las Vegas and Orlando, and Tier III markets such as Tampa, Jacksonville, Austin, and Pittsburgh.

Related Stories

Office Buildings | Jul 19, 2022

Austin adaptive reuse project transforms warehouse site into indoor-outdoor creative office building

Fifth and Tillery, an adaptive reuse project, has revitalized a post-industrial site in East Austin, Texas.

Office Buildings | Jul 12, 2022

Miami office tower nears completion, topping off at 55 stories

In Miami, construction of OKO Group and Cain International’s 830 Brickell office tower is nearing completion.

AEC Business Innovation | Jun 15, 2022

Cognitive health takes center stage in the AEC industry

Two prominent architecture firms are looking to build on the industry’s knowledge base on design’s impact on building occupant health and performance with new research efforts.

Sustainable Design and Construction | Jun 14, 2022

For its new office, a farm in California considers four sustainable design options, driven by data

The architect used cove.tool’s performance measurement software to make its case.

Office Buildings | Jun 13, 2022

San Antonio’s electric utility HQ to transform into a modern office building

In San Antonio, Tex., the former headquarters of CPS Energy, the city’s electric utility, is slated to transform into 100,000 square feet of office and retail space on San Antonio’s famed River Walk.

Office Buildings | Jun 8, 2022

Former L.A. Times newsroom/printing plant remade into office campus

Phase 1 of The Press, an adaptive reuse project that is converting an old Los Angeles Times facility into a modern office campus, was recently completed in Costa Mesa, Calif.

Office Buildings | May 19, 2022

JLL releases its 2022 Office Fit Out Guide

JLL’s 2022 Office Fit Out Guide report provides benchmark costs to build out a range of office types across major markets in the United States and Canada.

Headquarters | May 10, 2022

JPMorgan Chase’s new all-electric headquarters to have net-zero operational emissions

JPMorgan Chase’s recently unveiled plans for its new global headquarters building in New York City that is rife with impressive sustainability credentials.

Building Team | May 6, 2022

Atlanta’s largest adaptive reuse project features cross laminated timber

Global real estate investment and management firm Jamestown recently started construction on more than 700,000 sf of new live, work, and shop space at Ponce City Market.

Office Buildings | Apr 28, 2022

A 48-story office tower to rise over boomtown Austin

In downtown Austin, Texas, a planned 48-story office tower, The Republic, recently secured its first major tenant—allowing for the groundbreaking by midyear.