Cap rates for real estate across most asset sectors is expected to remain stable in the second half of 2015, following a first half during which the U.S. commercial real estate market continued to perform well and attract substantial investor interest.

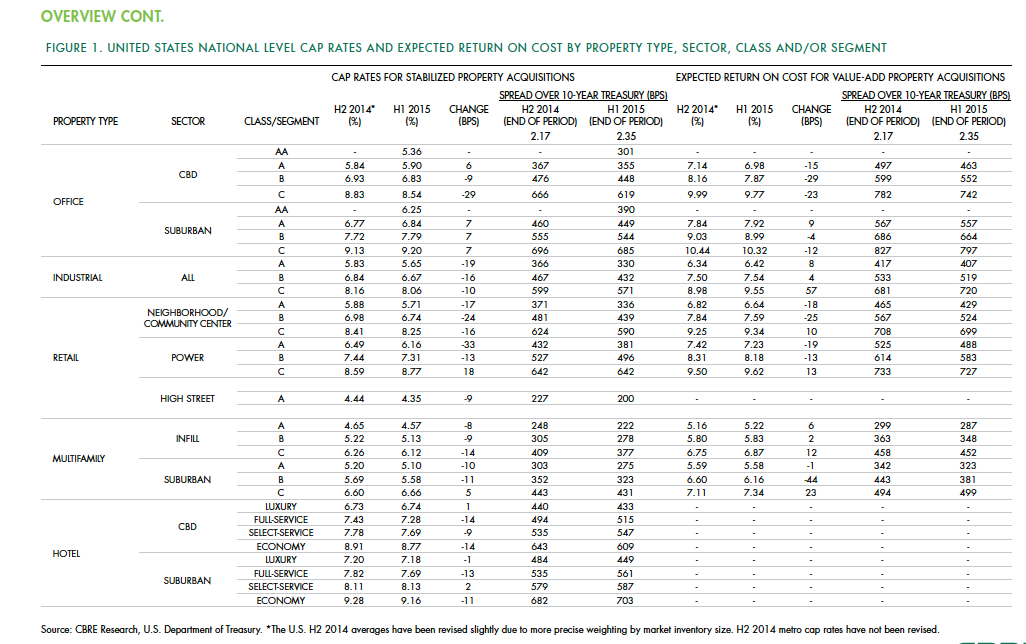

According to the CBRE North America Cap Rate Survey, which tracks activity in 46 major U.S. markets and 10 markets in Canada during the first six months of the year, national cap rates for industrial facilities in the U.S. experienced “very modest” cap-rate declines of 10 to 19 basis points. CBRE estimates that cap rates for stabilized Class A industrial assets was 5.65%.

Class A infill multifamily cap rates were 4.57% in the first half of the year, the second-lowest of all product types. The retail sector had the most significant national cap rate compression, followed by hotels. CBRE suggests that retail and hotels were the sectors that took the longest to recover from the past recession, “therefore, it is not surprising that the cap rate declines are greater in these sectors than those more mature in the real estate cycle.”

Central Business District Class B and C office cap rates were slightly off in the first half, but not Class A offices, “one example of investors moving out of on the risk curve,” CBRE notes. And despite sales volume gains, suburban office cap rates rose, on average, by 7 basis points.

Details from this report, as well as CBRE’s near-term predictions, include the following:

• Interest rates, a big demand driver in the commercial real estate space, are expected to rise modestly. The 10-year Treasury is projected to increase to 2.61% in the second half of 2015, and to 3.19% in 2016. However, “the near-term outlook of higher interest rates is not necessarily going to translate into higher cap rates if the rates come from stronger economic growth, as expected, as opposed to an unexpected shock to the economic system,” CBRE writes.

• CRBE doesn’t expect any cap rate movement in the second half of 2015 for office assets in the majority of markets, and only modest declines in those asset classes that do change. Jacksonville and Cincinnati are expected to experience the largest cap rate declines in Class A acquisitions.

• Transaction activity in the U.S. industrial sector during the first half of 2015 rose 70% to $37 billion. CBRE expects the full-year gain over 2014 to be 40% or greater. Cap rates in this sector are expected to fall modestly in more than one-third of the markets surveyed. Larger declines of 25 basis points or more are expected in Class B and C stabilized properties in Philadelphia and St. Louis. On the other hand, 58% of the market surveyed should experience no change to stabilized industrial cap rates.

• Retail investment in the first half of 2015 rose 12% to $45.6 billion. The “mall and other” category in this sector grew by 14%. CBRE expects investment to accelerate modestly through the remainder of the year. As far as cap rates are concerned, Class B experienced the largest average decline of 24 basis points. And four markets—San Jose, San Francisco, Los Angeles, and Orange County, Calif.—all had Class A caps under 5%.

• In the first six months of 2015, sales of multifamily properties jumped 38% to 63.2 billion. One-third of that capital went to mid- and high-rise projects. For Class A infill assets, San Francisco had the lowest cap rate, at 3.75%. Of the 44 markets surveyed in this sector, 33 had cap rates of 5% or less. CRBE is predicting no cap rate change for acquisitions of stabilized infill multifamily assets in the second half of the year for more than 80% of the markets surveyed. But cap compression should occur in Nashville, Washington D.C., Baltimore, Indianapolis, and Detroit.

• Investment in U.S. hotels, at $26.9 billion, was 67% higher than in the first half of 2014. The vast majority of hotel investors are domestic, especially outside of major cities. CBRE suggests, though, that hotel pricing, as measured by cap rates, has peaked for high-end products in top-tier markets. “But it’s too early to definitively make that call,” it writes. CRBE expects cap rates for acquisitions of stabilized hotel properties to remain “broadly stable” in the second half of 2015, with 62% of markets tracked experiencing no change. Any noticeable compression is likely to occur in Tier I metros like Las Vegas and Orlando, and Tier III markets such as Tampa, Jacksonville, Austin, and Pittsburgh.

Related Stories

Contractors | Apr 10, 2023

What makes prefabrication work? Factors every construction project should consider

There are many factors requiring careful consideration when determining whether a project is a good fit for prefabrication. JE Dunn’s Brian Burkett breaks down the most important considerations.

Mixed-Use | Apr 7, 2023

New Nashville mixed-use high-rise features curved, stepped massing and wellness focus

Construction recently started on 5 City Blvd, a new 15-story office and mixed-use building in Nashville, Tenn. Located on a uniquely shaped site, the 730,000-sf structure features curved, stepped massing and amenities with a focus on wellness.

Architects | Apr 6, 2023

New tool from Perkins&Will will make public health data more accessible to designers and architects

Called PRECEDE, the dashboard is an open-source tool developed by Perkins&Will that draws on federal data to identify and assess community health priorities within the U.S. by location. The firm was recently awarded a $30,000 ASID Foundation Grant to enhance the tool.

Architects | Apr 6, 2023

Design for belonging: An introduction to inclusive design

The foundation of modern, formalized inclusive design can be traced back to the Americans with Disabilities Act (ADA) in 1990. The movement has developed beyond the simple rules outlined by ADA regulations resulting in features like mothers’ rooms, prayer rooms, and inclusive restrooms.

Sustainability | Apr 4, 2023

NIBS report: Decarbonizing the U.S. building sector will require massive, coordinated effort

Decarbonizing the building sector will require a massive, strategic, and coordinated effort by the public and private sectors, according to a report by the National Institute of Building Sciences (NIBS).

Legislation | Mar 24, 2023

New York lawmakers set sights on unsafe lithium-ion batteries used in electric bikes and scooters

Lawmakers in New York City and statewide have moved to quell the growing number of fires caused by lithium-ion batteries used in electric bikes and scooters.

Government Buildings | Mar 24, 2023

19 federal buildings named GSA Design Awards winners

After a six-year hiatus, the U.S. General Services Administration late last year resumed its esteemed GSA Design Awards program. In all, 19 federal building projects nationwide were honored with 2022 GSA Design Awards, eight with Honor Awards and 11 with Citations.

Mass Timber | Mar 19, 2023

A 100% mass timber construction project is under way in North Carolina

An office building 100% made from mass timber has started construction within the Live Oak Bank campus in Wilmington, N.C. The 67,000-sf structure, a joint building venture between the GCs Swinerton and Wilmington-headquartered Monteith Construction, is scheduled for completion in early 2024.

Urban Planning | Mar 16, 2023

Three interconnected solutions for 'saving' urban centers

Gensler Co-CEO Andy Cohen explores how the global pandemic affected city life, and gives three solutions for revitalizing these urban centers.

Sponsored | Cladding and Facade Systems | Mar 15, 2023

Metal cladding trends and innovations

Metal cladding is on a growth trajectory globally. This is reflected in rising demand for rainscreen cladding and architectural metal coatings. This course covers the latest trends and innovations in the metal cladding market.