Cap rates for real estate across most asset sectors is expected to remain stable in the second half of 2015, following a first half during which the U.S. commercial real estate market continued to perform well and attract substantial investor interest.

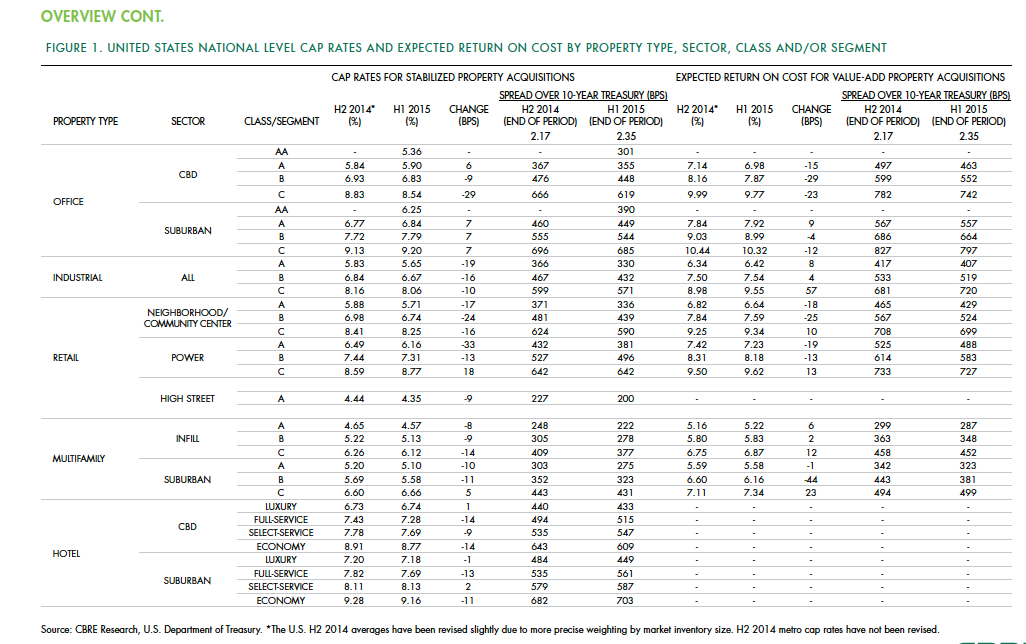

According to the CBRE North America Cap Rate Survey, which tracks activity in 46 major U.S. markets and 10 markets in Canada during the first six months of the year, national cap rates for industrial facilities in the U.S. experienced “very modest” cap-rate declines of 10 to 19 basis points. CBRE estimates that cap rates for stabilized Class A industrial assets was 5.65%.

Class A infill multifamily cap rates were 4.57% in the first half of the year, the second-lowest of all product types. The retail sector had the most significant national cap rate compression, followed by hotels. CBRE suggests that retail and hotels were the sectors that took the longest to recover from the past recession, “therefore, it is not surprising that the cap rate declines are greater in these sectors than those more mature in the real estate cycle.”

Central Business District Class B and C office cap rates were slightly off in the first half, but not Class A offices, “one example of investors moving out of on the risk curve,” CBRE notes. And despite sales volume gains, suburban office cap rates rose, on average, by 7 basis points.

Details from this report, as well as CBRE’s near-term predictions, include the following:

• Interest rates, a big demand driver in the commercial real estate space, are expected to rise modestly. The 10-year Treasury is projected to increase to 2.61% in the second half of 2015, and to 3.19% in 2016. However, “the near-term outlook of higher interest rates is not necessarily going to translate into higher cap rates if the rates come from stronger economic growth, as expected, as opposed to an unexpected shock to the economic system,” CBRE writes.

• CRBE doesn’t expect any cap rate movement in the second half of 2015 for office assets in the majority of markets, and only modest declines in those asset classes that do change. Jacksonville and Cincinnati are expected to experience the largest cap rate declines in Class A acquisitions.

• Transaction activity in the U.S. industrial sector during the first half of 2015 rose 70% to $37 billion. CBRE expects the full-year gain over 2014 to be 40% or greater. Cap rates in this sector are expected to fall modestly in more than one-third of the markets surveyed. Larger declines of 25 basis points or more are expected in Class B and C stabilized properties in Philadelphia and St. Louis. On the other hand, 58% of the market surveyed should experience no change to stabilized industrial cap rates.

• Retail investment in the first half of 2015 rose 12% to $45.6 billion. The “mall and other” category in this sector grew by 14%. CBRE expects investment to accelerate modestly through the remainder of the year. As far as cap rates are concerned, Class B experienced the largest average decline of 24 basis points. And four markets—San Jose, San Francisco, Los Angeles, and Orange County, Calif.—all had Class A caps under 5%.

• In the first six months of 2015, sales of multifamily properties jumped 38% to 63.2 billion. One-third of that capital went to mid- and high-rise projects. For Class A infill assets, San Francisco had the lowest cap rate, at 3.75%. Of the 44 markets surveyed in this sector, 33 had cap rates of 5% or less. CRBE is predicting no cap rate change for acquisitions of stabilized infill multifamily assets in the second half of the year for more than 80% of the markets surveyed. But cap compression should occur in Nashville, Washington D.C., Baltimore, Indianapolis, and Detroit.

• Investment in U.S. hotels, at $26.9 billion, was 67% higher than in the first half of 2014. The vast majority of hotel investors are domestic, especially outside of major cities. CBRE suggests, though, that hotel pricing, as measured by cap rates, has peaked for high-end products in top-tier markets. “But it’s too early to definitively make that call,” it writes. CRBE expects cap rates for acquisitions of stabilized hotel properties to remain “broadly stable” in the second half of 2015, with 62% of markets tracked experiencing no change. Any noticeable compression is likely to occur in Tier I metros like Las Vegas and Orlando, and Tier III markets such as Tampa, Jacksonville, Austin, and Pittsburgh.

Related Stories

| Jun 2, 2014

Parking structures group launches LEED-type program for parking garages

The Green Parking Council, an affiliate of the International Parking Institute, has launched the Green Garage Certification program, the parking industry equivalent of LEED certification.

| May 29, 2014

7 cost-effective ways to make U.S. infrastructure more resilient

Moving critical elements to higher ground and designing for longer lifespans are just some of the ways cities and governments can make infrastructure more resilient to natural disasters and climate change, writes Richard Cavallaro, President of Skanska USA Civil.

| May 28, 2014

KPF's dual towers in Turkey will incorporate motifs, symbols of Ottoman Empire

The two-building headquarters for Turkey’s largest and oldest financial institution, Ziraat Bank, is inspired by the country’s cultural heritage.

| May 27, 2014

One World Trade Center cuts rents due to sluggish activity

Sluggish economy and lackluster leasing force developer The Durst Organization and the Port Authority of New York and New Jersey to reduce asking rents by nearly 10% to $69/sf.

| May 23, 2014

Big design, small package: AIA Chicago names 2014 Small Project Awards winners

Winning projects include an events center for Mies van der Rohe's landmark Farnsworth House and a new boathouse along the Chicago river.

| May 23, 2014

Top interior design trends: Gensler, HOK, FXFOWLE, Mancini Duffy weigh in

Tech-friendly furniture, “live walls,” sit-stand desks, and circadian lighting are among the emerging trends identified by leading interior designers.

| May 22, 2014

Big Data meets data centers – What the coming DCIM boom means to owners and Building Teams

The demand for sophisticated facility monitoring solutions has spurred a new market segment—data center infrastructure management (DCIM)—that is likely to impact the way data center projects are planned, designed, built, and operated.

| May 22, 2014

No time for a trip to Dubai? Team BlackSheep's drone flyover gives a bird's eye view [video]

Team BlackSheep—devotees of filmmaking with drones—has posted a fun video that takes viewers high over the city for spectacular vistas of a modern architectural showcase.

| May 21, 2014

Check out Pandora's posh NYC offices [slideshow]

The new East Coast office for the Internet radio provider is housed on two interconnected floors of the classic 125 Park Avenue building, and features multiple spaces for music performances, large gatherings, and “all hands” meetings.

| May 20, 2014

Kinetic Architecture: New book explores innovations in active façades

The book, co-authored by Arup's Russell Fortmeyer, illustrates the various ways architects, consultants, and engineers approach energy and comfort by manipulating air, water, and light through the layers of passive and active building envelope systems.