Societies continue to move toward megacity cultures, lifestyles, and economies that are becoming more vital, in some cases, than the countries that spawn them.

One result of this trend has been a growing tendency among owners, developers, and their Building Teams to package smaller and multiple commercial projects into large, single megaprojects whose construction costs exceed $1 billion, in spite of such projects’ historically erratic success rates and shortcomings.

“Speed to market has become critical for owners. In addition, construction companies are getting larger, making it more feasible for them to handle bigger projects,” explains Ron Magnus, a founding Principal with the market research firm FMI, which has just come out with a new study titled “Megaprojects: Changing the Conversation.”

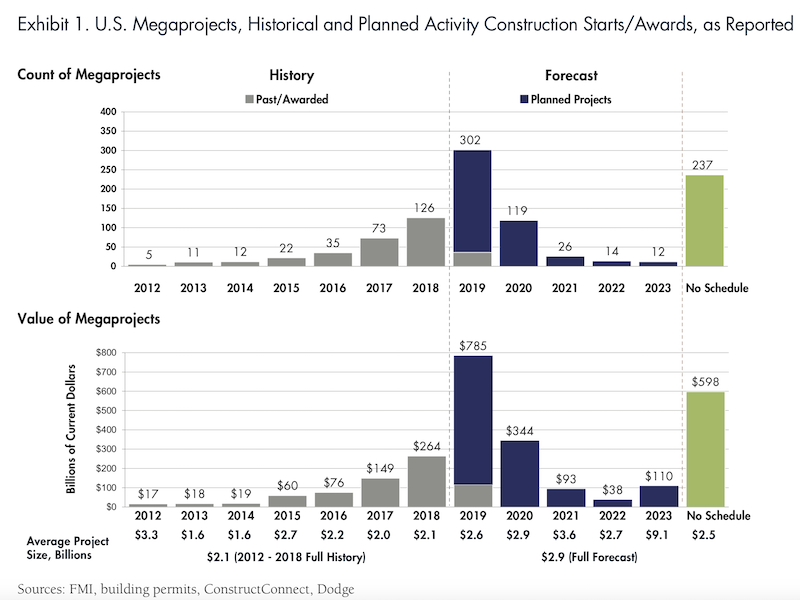

FMI’s report, authored by its content director Sabine Hoover, indicates that at least 320 megaprojects have been awarded in the U.S. alone since 2012—at an aggregate investment valued at over $700 billion.

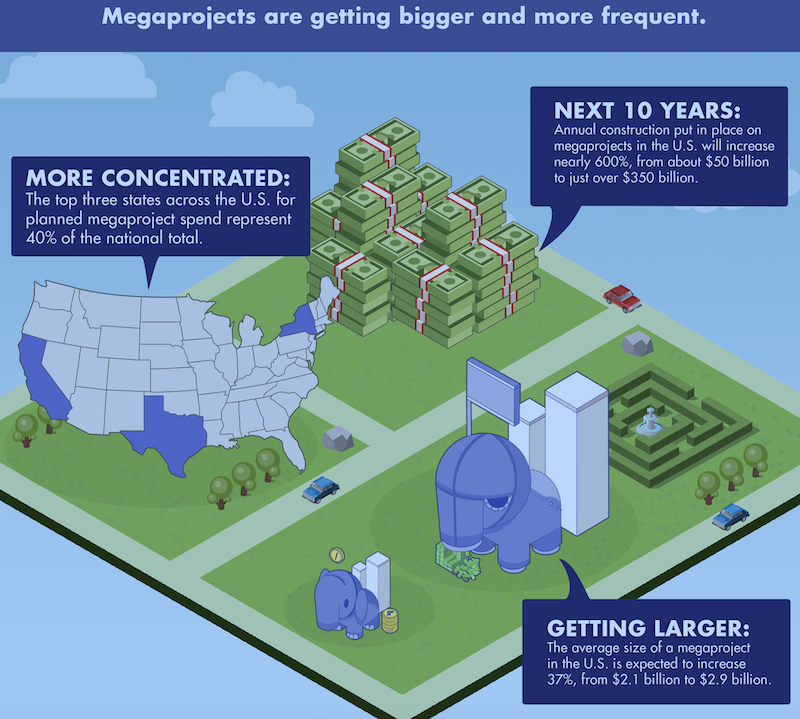

Additionally, more than 670 megaprojects are being planned, a future investment opportunity likely to reach $2 trillion. Most of these planned megaprojects are expected to be built in the South and West, with three states accounting for 40% of the total starts value (New York, 15%; California, 15%; and Texas, 10%).

FMI predicts that megaprojects could account for 20% or more of construction spending within the next five years. Chart: FMI

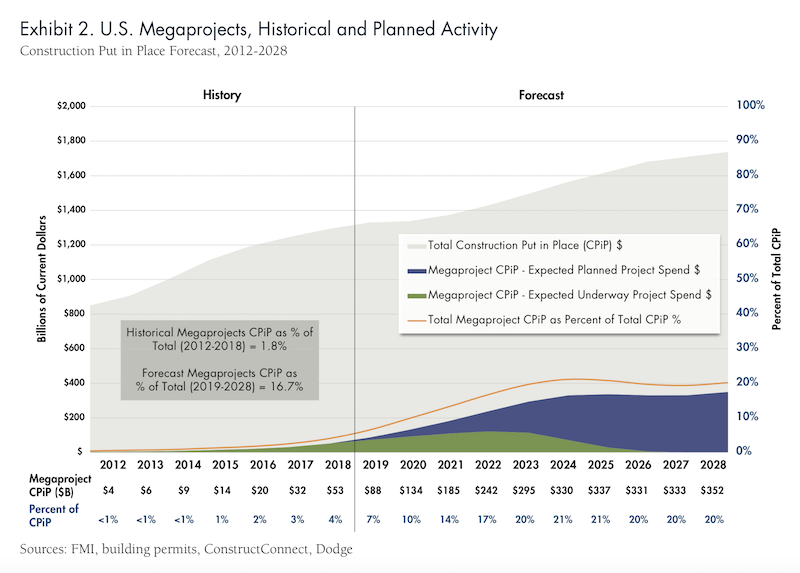

Megaprojects have been expanding in number and value. Between 2013 and 2018, the annual value of U.S. megaproject starts increased from 3% to approximately 33% of all U.S. construction project starts. FMI predicts that, over the next decade, annual construction put in place on megaprojects will explode by nearly 600% to $350 billion.

Measured another way, megaproject construction put in place accounted for only 1.8% of total CPiP between 2012 and 2018. FMI estimates that within the next decade—and possibly within the next five or six years—annual megaproject spending could equal around 20% of total construction spending.

While FMI acknowledges that industrial and infrastructure starts have accounted for the bulk of megaproject starts (61% in 2018), it also sees more evidence of this trend in nonresidential building.

The value of megaproject starts could rise at an especially brisk clip over the next two years. Chart: FMI

The big question, though, is whether the industry is ready to meet this demand. Part of FMI’s research for this report included input from a roundtable of 22 stakeholders—AEC firms, owners, academics—that have engaged megaprojects in the past. From that discussion FMI gleaned five key success factors:

•Trust. Stakeholders on successful megaprojects invest a lot of time upfront in building trust through off-site meetings, getting to know each other on a personal basis. “Trust is the cornerstone, the basic building block,” says Jim Whitaker, FAIA, FDBIA, Principal and Senior Vice President with HKS Inc.

•Culture of Cohesion and Collaboration. DPR Construction on one megaproject spent two weeks with the owner and architect charting the work and setting up its organizational structure. By doing so, the team reduced that project’s budget by $200 million without yielding functionality, square footage, or quality.

Keith Molenaar, associate dean for research at the University of Colorado Boulder, in collaboration with the Pankow Foundation, has studied more than 200 different building projects and found that early collaboration was key to success. The delivery method chosen, on the other hand, had far less impact.

•Transparent and authentic leadership. Effective megaproject leaders, says FMI, are experts in developing a team environment that fosters emotional engagement, shared purpose and accountability.

•Nimble and autonomous teams. Successful megaproject teams are getting away from centralized management and are setting up smaller, more nimble project teams that can move quickly. “Like the platoon model for marines, these teams enjoy a certain degree of autonomy and are empowered to make decisions without approval from the top, and at each decision point,” says FMI.

•Educated and experienced owners. The report quotes Darin Daskarolis, senior director of Global Construction-Data Centers at Facebook, who notes that since commercial construction is largely a relationship-based business, “we knew we had to form strong bonds with our contractors to develop a common and realistic view of the challenges ahead. This common view informed sensible budgets and guided strategic staffing decisions.

The global strategist Parag Khanna sees a world that is becoming more connected by buildings and structures. So where global defense budgets and military spending total about $2 trillion per year, infrastructure spending is expected to increase from $3 trillion today to $9 trillion annually by 2030.

For the U.S., FMI forecasts that half of all megaproject spending over the next three to five years could occur in just 20 metros, and just five of these markets—New York, Los Angeles, Dallas, Houston, and Washington D.C.—will account for one-fifth of total construction in the country. But FMI also ends its report with a cautionary warning for the construction industry. “We have no choice but to completely change our mindsets. Should megaprojects continue to fail just as their spending is expected to reach new heights, the impacts could be devastating to the framework of the E&C industry.”

Related Stories

Codes and Standards | Oct 26, 2022

‘Landmark study’ offers key recommendations for design-build delivery

The ACEC Research Institute and the University of Colorado Boulder released what the White House called a “landmark study” on the design-build delivery method.

Building Team | Oct 26, 2022

The U.S. hotel construction pipeline shows positive growth year-over-year at Q3 2022 close

According to the third quarter Construction Pipeline Trend Report for the United States from Lodging Econometrics (LE), the U.S. construction pipeline stands at 5,317 projects/629,489 rooms, up 10% by projects and 6% rooms Year-Over-Year (YOY).

Designers | Oct 19, 2022

Architecture Billings Index moderates but remains healthy

For the twentieth consecutive month architecture firms reported increasing demand for design services in September, according to a new report today from The American Institute of Architects (AIA).

Market Data | Oct 17, 2022

Calling all AEC professionals! BD+C editors need your expertise for our 2023 market forecast survey

The BD+C editorial team needs your help with an important research project. We are conducting research to understand the current state of the U.S. design and construction industry.

Market Data | Oct 14, 2022

ABC’s Construction Backlog Indicator Jumps in September; Contractor Confidence Remains Steady

Associated Builders and Contractors reports today that its Construction Backlog Indicator increased to 9.0 months in September, according to an ABC member survey conducted Sept. 20 to Oct. 5.

Market Data | Oct 12, 2022

ABC: Construction Input Prices Inched Down in September; Up 41% Since February 2020

Construction input prices dipped 0.1% in September compared to the previous month, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics’ Producer Price Index data released today.

Laboratories | Oct 5, 2022

Bigger is better for a maturing life sciences sector

CRB's latest report predicts more diversification and vertical integration in research and production.

Market Data | Aug 25, 2022

‘Disruptions’ will moderate construction spending through next year

JLL’s latest outlook predicts continued pricing volatility due to shortages in materials and labor

Market Data | Aug 2, 2022

Nonresidential construction spending falls 0.5% in June, says ABC

National nonresidential construction spending was down by 0.5% in June, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau.

Market Data | Jul 28, 2022

The latest Beck Group report sees earlier project collaboration as one way out of the inflation/supply chain malaise

In the first six months of 2022, quarter-to-quarter inflation for construction materials showed signs of easing, but only slightly.