U.S. retail and food services sales in July, at $696.4 billion, were up 3.2% over the same month a year ago, according to Census Bureau estimates. Luxury retail, in particular, has been ascending, the beneficary of persistent and post-COVID pent-up demand and robust retail expansion, according to a new Luxury Report 2023 released by Jones Lang Lasalle (JLL) this week.

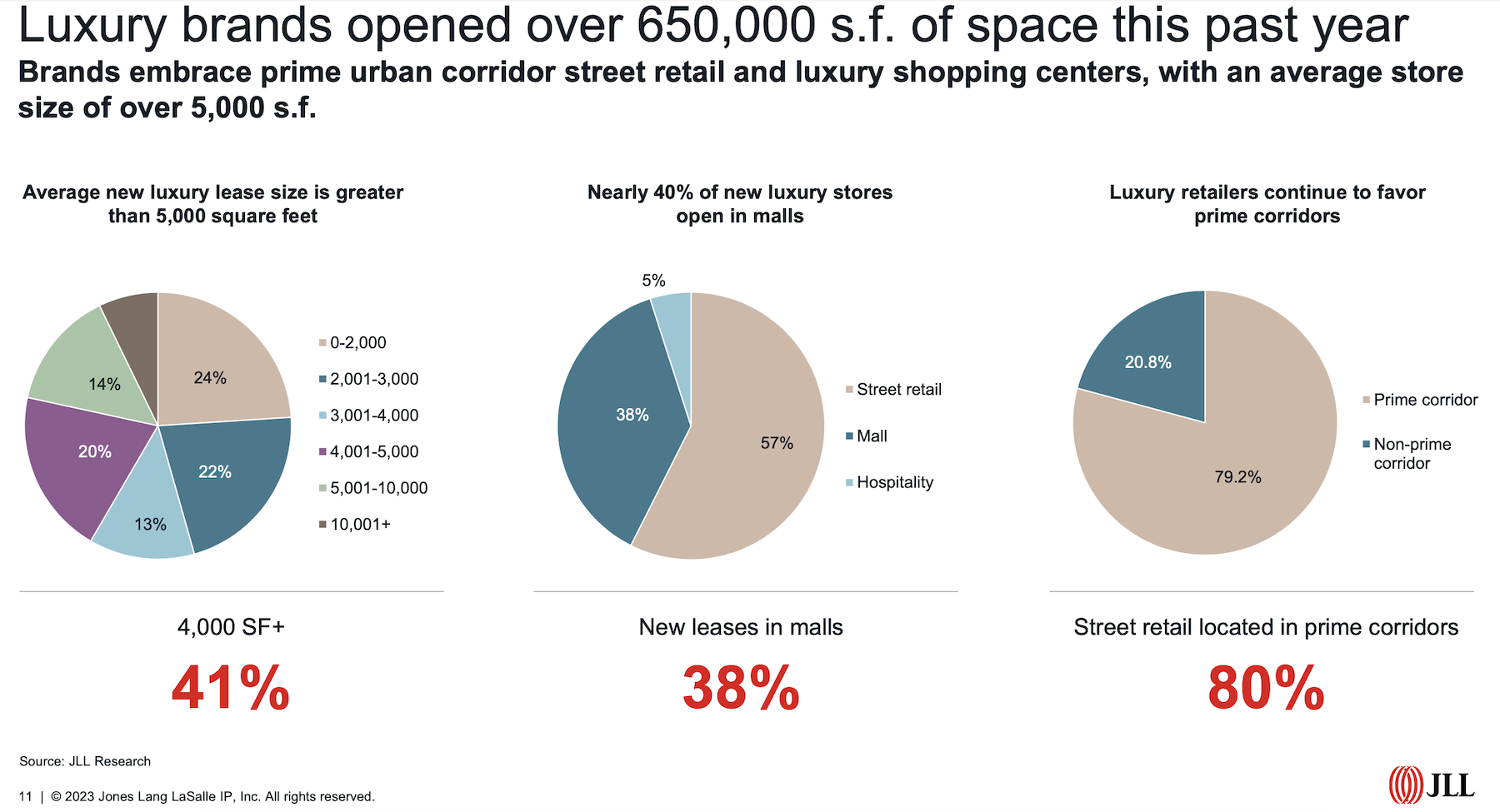

The United States accounted for the largest share of the global luxury market, 34% of overall sales, and JLL foresees ongoing growth to $83.33 billion in 2028 compared to $69.51 billion in 2022. Last year alone, luxury retailers added more than 650,000 sf of new selling spaces and stores with enhanced ecommerce capabilities, and JLL anticipates further expansion in prime retail corridors, suburban malls, and shopping centers.

LVMH, the global giant whose brands include Louis Vuitton and Tiffany, increased its net store count last year by 108 to 5,664 units worldwide. Kering Group, which controls brands that include Gucci and Bottega Veneta, added 100 stores, bringing its total to 1,659.

The average new luxury lease size is now greater than 5,000 sf.

Luxury retail getting more comfortable in the Sunbelt

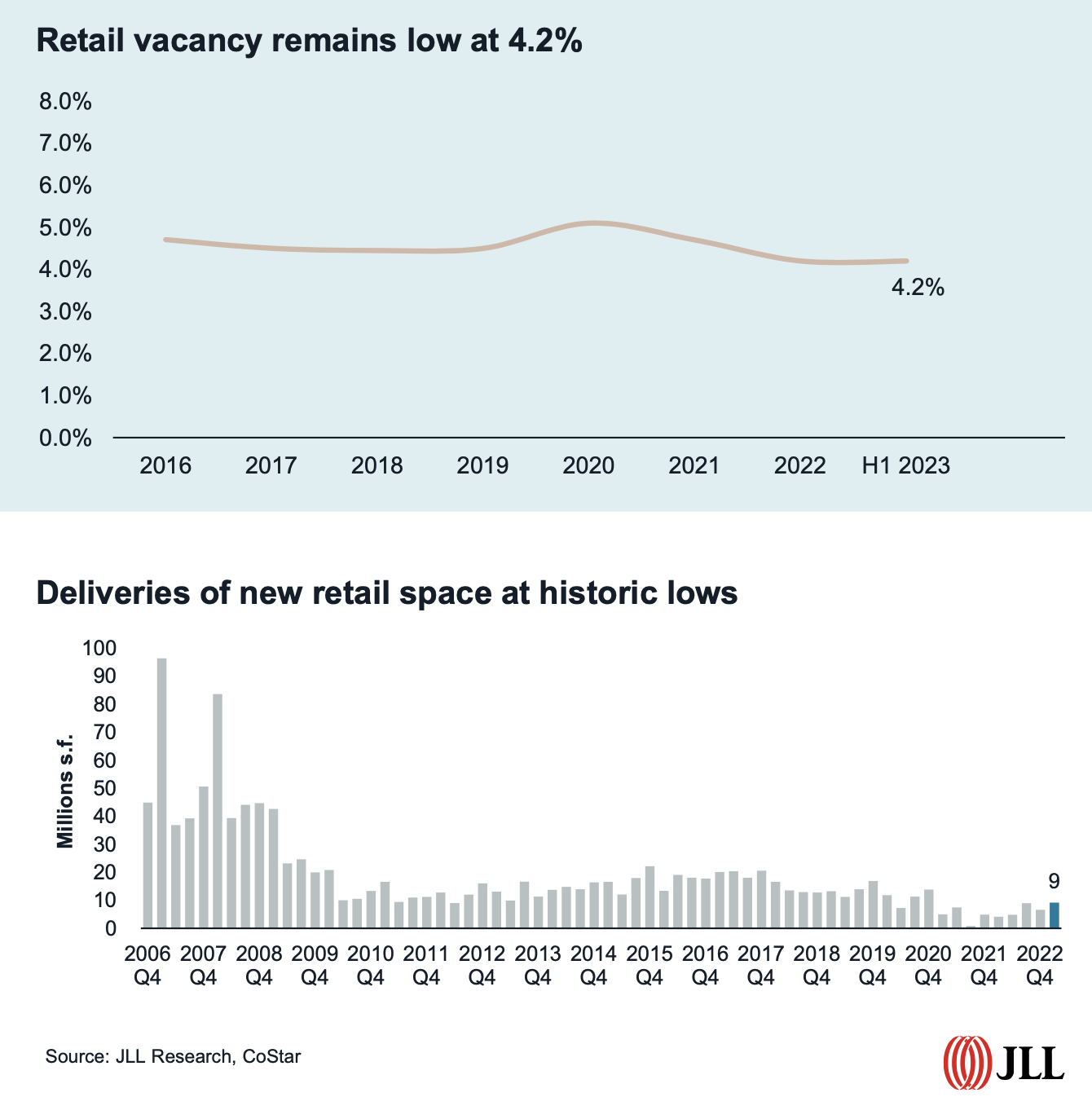

JLL suggests that the stars are aligned for bricks and mortar luxury retail. The retail sector as a whole continues to report solid fundamentals and low vacancy rates. Ecommerce, as a percentage of total retail sales, appears to have stalled at around 15%. And more than three-quarters of frequent luxury shoppers polled in a recent survey said they plan to visit a luxury store as often as or more frequently than they did last year.

JLL is finding that while New York and California account for over half of all new luxury store openings in the U.S., the Sunbelt is seeing significant expansion in places like Atlanta, Miami, and Las Vegas. Surprisingly as well has been the willingness of luxury brands to open new stores in malls, which accounted for 38% of the space added last year.

A growing number of mall operators now devote entire wings to luxury brands. In Toronto, for example, The Oxford Properties-owned Yorkdale Shopping Centre is repurposing 100,000 sf of space to increase the mall’s luxury composition to 20% in 2025, from 13% today.

What’s also indisputable has been the preference of luxury retailers toward street retail located in prime corridors, which account for more than 45% of all new luxury leasing activity in the U.S. Prime corridors include New York City’s Times Square, which saw a 29.1% increase in corridor foot traffic between July 2022 and 2023. Boston’s Newberry Street corridor saw an 18% year-over-year increase in foot traffic. The Beverly Hills Triangle accounted for 41% of all luxury store openings in Los Angeles last year, including Chanel’s largest flagship store in the U.S., a 30,000-sf lease.

Quoting CoStar data, JLL notes that cities where rents are rising fastest, like Las Vegas, have also been magnets for luxury dealers.

Secondhand products offer sales alternatives

Last year 12% of new luxury leases were for luxury boutiques, a growing category within this sector, says JLL. Brands in this category include Kith, Elyse Walker, and The Webster.

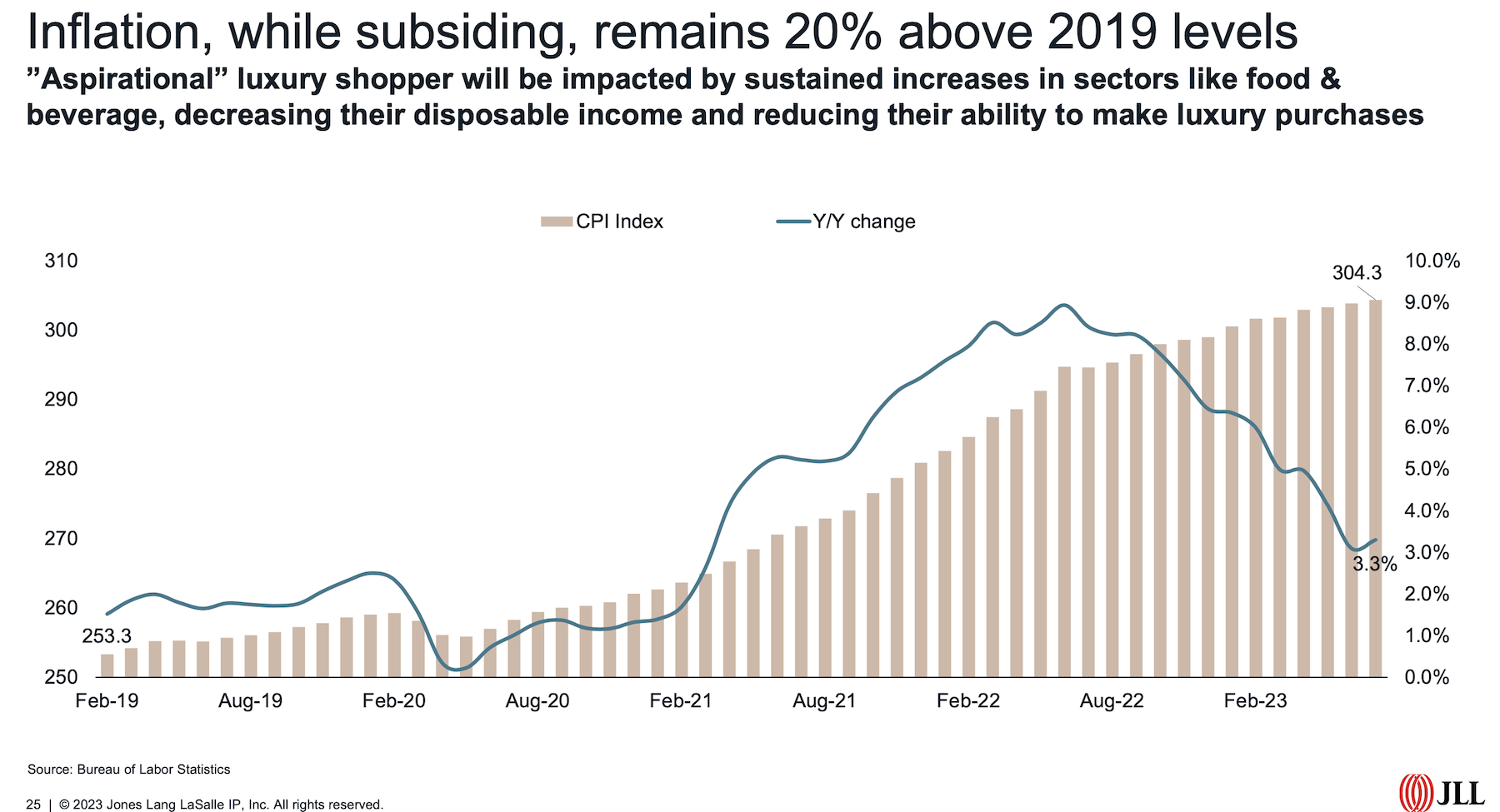

But there are some warning signs that could slow the luxury juggernaut. For one thing, there’s a lack of available retail space in an industry sector with historically low new deliveries. For another, so-called aspirational shoppers are still struggling with inflation at every retail level, not the least being luxury.

JLL reports that the market for secondhand luxury products grew by 28% in 2022. (Earlier this year, eBay launched “Certified by Brand,” which offers new, certified pre-owned, and limited-edition luxury products.) With more consumers concerned about environmental issues, brands that want to remain relevant must demonstrate a willingness to invest in the circular economy.

Related Stories

Giants 400 | Sep 12, 2023

Top 80 Retail Sector Contractors and Construction Management Firms for 2023

Whiting-Turner, ARCO Construction, Swinerton, and PCL top BD+C's ranking of the nation's largest retail building contractors and construction management (CM) firms for 2023, as reported in the 2023 Giants 400 Report. Note: This ranking factors revenue for all retail buildings work, including big box stores, cineplexes, entertainment centers, malls, restaurants, strip centers, and theme parks.

Firms for 2023")

Giants 400 | Sep 11, 2023

Top 140 Retail Sector Architecture and Architecture Engineering (AE) Firms for 2023

Gensler, Arcadis, Core States Group, WD Partners, and NORR top BD+C's ranking of the nation's largest retail sector architecture and architecture engineering (AE) firms for 2023, as reported in the 2023 Giants 400 Report. Note: This ranking factors revenue for all retail buildings work, including big box stores, cineplexes, entertainment centers, malls, restaurants, strip centers, and theme parks.

Adaptive Reuse | Aug 31, 2023

Small town takes over big box

GBBN associate Claire Shafer, AIA, breaks down the firm's recreational adaptive reuse project for a small Indiana town.

Giants 400 | Aug 22, 2023

Top 115 Architecture Engineering Firms for 2023

Stantec, HDR, Page, HOK, and Arcadis North America top the rankings of the nation's largest architecture engineering (AE) firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Giants 400 | Aug 22, 2023

2023 Giants 400 Report: Ranking the nation's largest architecture, engineering, and construction firms

A record 552 AEC firms submitted data for BD+C's 2023 Giants 400 Report. The final report includes 137 rankings across 25 building sectors and specialty categories.

Giants 400 | Aug 22, 2023

Top 175 Architecture Firms for 2023

Gensler, HKS, Perkins&Will, Corgan, and Perkins Eastman top the rankings of the nation's largest architecture firms for nonresidential building and multifamily housing work, as reported in Building Design+Construction's 2023 Giants 400 Report.

Shopping Centers | Aug 22, 2023

The mall of the future

There are three critical aspects of mall design that, through evolution, have proven to be instrumental in the staying power of a retail destination: parking, planning, and customer experience. This are crucial to the mall of the future.

Adaptive Reuse | Aug 17, 2023

How to design for adaptive reuse: Don’t reinvent the wheel

Gresham Smith demonstrates the opportunities of adaptive reuse, specifically reusing empty big-box retail and malls, many of which sit unused or underutilized across the country.

Sponsored | | Aug 15, 2023

The Data Benefits of Retail Keyless Entry

SALTO’s wireless access control system provides valuable data analytics for retail establishments

Office Buildings | Aug 10, 2023

Bjarke Ingels Group and Skanska to deliver 1550 on the Green, one of the most sustainable buildings in Texas

In downtown Houston, Skanska USA’s 1550 on the Green, a 28-story, 375,000-sf office tower, aims to be one of Texas’ most sustainable buildings. The $225 million project has deployed various sustainable building materials, such as less carbon-intensive cement, to target 60% reduced embodied carbon.