Add to the growing list of forecasts about the fate of retailing in America a new report by the global consulting firm A.T. Kearney that suggests the survival of shopping centers and malls will be predicated on their “morphing” into Consumer Engagement Centers (CES) that are less about buying and selling products and more about creating experiences for consumers.

“The U.S. retail sector is moving from a ‘push’ model to a ‘pull’ model where consumers are demanding more curated experiences,” explains Michael Brown, a Partner with A.T. Kearney's retail group, and co-author of “The Future of Shopping Centers.”

The report stems from a larger study his firm conducted to examine and predict prospective consumer behaviors over the next 10-15 years, says Brown. The focus of the latest report is on Millennials, who will reach their peak spending years within the next decade.

The authors note that the U.S., at 23.5 sf of retail space per person, is already seriously overstored, compared to countries like Canada (16.8 sf/person), Australia (11.2 sf), the United Kingdom (4.6 sf), and Japan (4.4 sf). The U.S. also lags Europe when it comes to locating retail in proximity to transportation hubs, and building stores that are part of mixed-use developments.

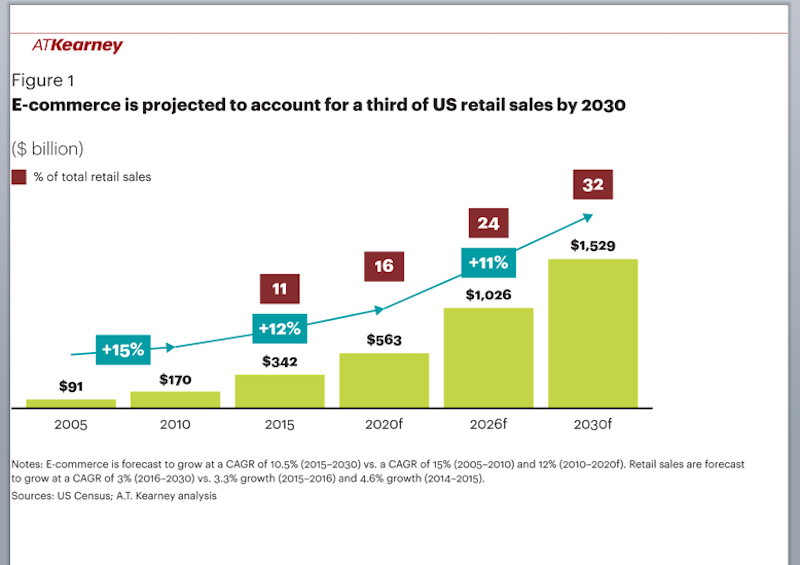

Looming in the background of A.T. Kearney's forecasts is the expanding encroachment of ecommerce. The report estimates that online purchases could account for 32% of total retail sales in the U.S. by 2030, or the equivalent of $1.53 trillion that year. That would be nearly triple the percentage in 2015, but Brown defends his firm's aggressive projections by noting that ecommerce has barely penetrated the grocery sector yet, but is likely to make a bigger splash there over the next several years, especially in light of Amazon’s $13.4 billion purchase of Whole Foods last year.

In addition, the report expects that, by 2030, at least two-fifths of all consumers will be digital natives who won’t draw distinctions between digital and physical retailing. Consequently, it is critical for retailers to master and embrace digital retailing not only to communicate with shoppers and transact business, but also to identify new customers, track purchases, and analyze patterns.

The report talks about how technology is creating “personalized digital ecologies” for consumers, which CES operators need to tap into along with autonomous, on-demand mobility technologies (from driverless cars to robots) that could play a much bigger role in future shopping experiences.

Online purchases could account for nearly one-third of all U.S. retail sales by 2030. Retailers need to embrace digital commerce to attract consumers who are less disposed to distinguish between on- and offline shopping experiences. Image: A.T. Kearney

Logistics will determine winners from losers

When it comes to product assortments, retailers now find themselves scrambling to respond to consumer fragmentation, which Brown explains is leading toward “micro segmentation” that has the potential to cut into big-brand hegemony. Consequently, retailers need to build a logistical infrastructure driven by data analytics that allows them to offer multiple brands they can switch in and out of relatively quickly as consumer buying trends change.

The report believes consumers are going to want a lot more say in the goods and services that retailers bring to market. Their veto power starts with their smartphones, which give them the alacrity to select, or block, any input they choose. Advances in smartphone technology—along with advances in 3D printing, machine-to-machine interfaces, and artificial intelligence—will not only give consumers greater expectations about the control they wield over what goods and services retailers make available to them, but also how those products are ultimately delivered.

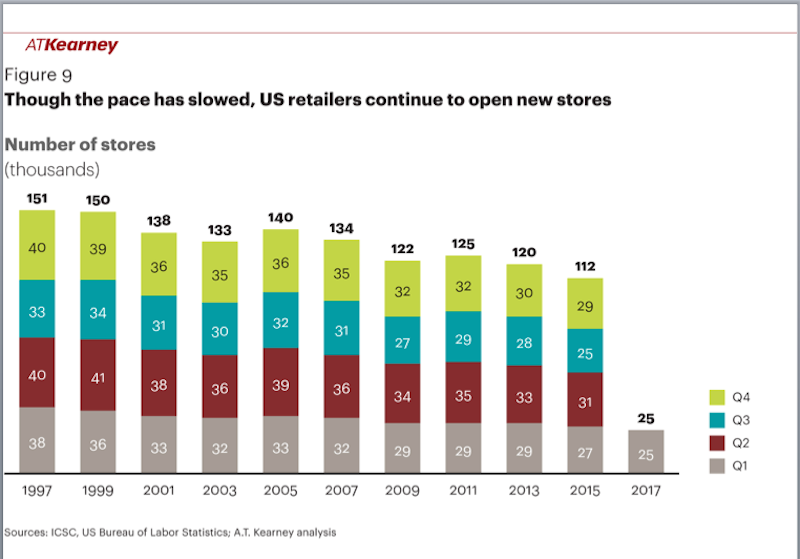

Physical stores aren’t going away; in fact, dealers are opening more stores in the U.S. And the picture about retailing’s future gets muddled when online retailers like Amazon and Boll & Branch are opening brick-and-mortar stores.

Even though the U.S. in overstored, dealers continue to open new outlets, although a growing number are using stores more as showrooms and distribution hubs for pickup by consumers who made their purchases online. Image: A.T. Kearney

But physical space, says Brown, is more likely to be used in the future to display merchandise and build experiences with consumers than to conduct actual buying and selling of products. He points specifically to the sporting goods retailer Foot Locker, which is reducing its store count but enlarging its remaining stores to enhance shoppers’ experience; and the home furnishings retailer Restoration Hardware, which has been opening “mansion” stores, 50,000- to 60,000-sf showrooms that support this dealer’s online selling strategy.

“Walmart and Amazon are successful because of their logistics,” says Brown, “and the speed and agility of a dealer’s infrastructure will be what’s important” going forward.

A.T. Kearney’s report divides successful future shopping centers into four distinct types:

•Destination centers that are regional malls with flagships, tenants that cater to specialized shopper groups, and possibly nontraditional anchors like theme parks. These destination centers could serve as digital distribution hubs, and even offer customers weekend experiences by tying into restaurants, hotels, and local entertainment;

•“Retaildential” centers, mixed-use facilities that are built to incorporate housing and are conveniently located near mass transit options;

•Value centers “that are anchored by an idea, not a retail nameplate,” the report states. Brown explains that value centers might cater to a specific ethnic group of customers, or to comsumers with like interests such as sports, fashion, or dining. These centers could include spaces for concerts, competitions, exhibits, and community events; and

•Innovation centers, that might be part-store, part research facility. They could include test stores and alternating-themed retail environments for the purpose of analyzing shoppers’ needs and behaviors over time.

Related Stories

Retail Centers | Apr 2, 2019

Brick-and-mortar retail is not dead—here’s proof

We continually hear that “retail is dying,” but there are many foundational retail types essential to consumers—here’s a look at 3 of them.

Retail Centers | Mar 19, 2019

Porsche’s next-gen showroom prototype opens in Palm Springs, Ca.

The dealership is the first to showcase Porsche’s new design philosophy, ‘Destination Porsche.’

Retail Centers | Dec 3, 2018

Biotrack your shop

Sabrina Hilfer, a specialty retail designer, talks about the integration of biometrics in the retailscape.

Retail Centers | Nov 8, 2018

The Container Store moves into the next generation courtesy FRCH Design Worldwide

The next-gen prototype is located in Dallas, Texas.

Retail Centers | Oct 22, 2018

Stuck in the middle: What can save the average American mall?

Erich Dohrer doesn’t want to talk about the “dead mall” or the great mall success story—he wants to talk about design solutions for the ones that are just getting by.

Retail Centers | Oct 9, 2018

Kengo Kuma designs Taipei Starbucks from 29 shipping containers

The store will be part of a new shopping mall.

Retail Centers | Sep 27, 2018

Turkish bazaar takes the shape of the surrounding mountains

The project is designed by PDG Architects and ANTEPE.

Retail Centers | Sep 26, 2018

The future of travel retail

Kevin Horn and Shirley Cheng explore how a new generation of travelers is disrupting airport retail.

Retail Centers | Sep 20, 2018

BIG designs ‘restaurant village’ just outside of Copenhagen

The restaurant comprises 11 spaces, each with their own unique function.

Retail Centers | Sep 17, 2018

Iteration vs disruption: Designing for a great customer experience

One way to solve for the future is to disrupt the expected.