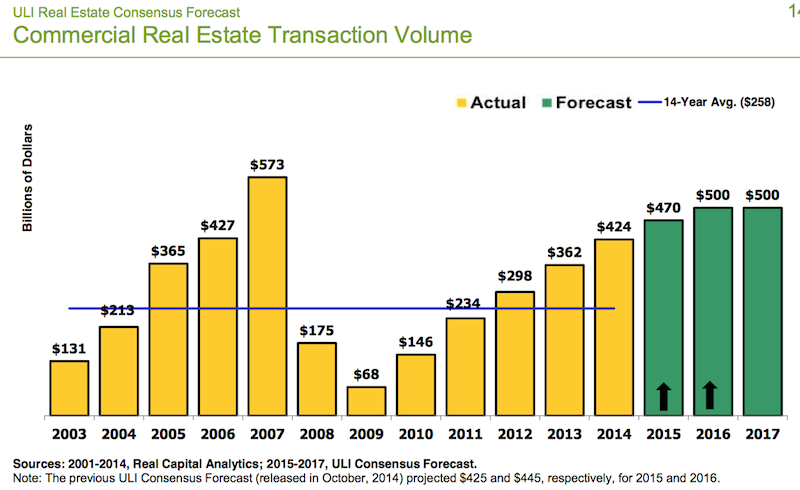

Driven by sparser availability of warehouses, offices, and retail, the real estate industry is positioned for solid growth this year and next, before tapering off at a still-respectable $500 billion in annual transactions in 2017.

Those predictions highlight Urban Land Institute’s (ULI) latest three-year Real Estate Consensus Forecast, based on the median of forecasts from 46 economists and analysts at 33 leading real estate organizations, who were surveyed from February 27 through March 23.

The expert consensus projects an 18% increase, to $470 billion, in commercial real estate transactions for 2015, followed by a 6.4%, to $500 billion, in 2016.

ULI’s forecast is more optimistic for the years 2015 and 2016 than previous forecasts for all indicators except single-family home starts.

The experts’ optimism stems, in part, from their predictions for healthy GDP growth, which they expect to rise by 3% this year and next, and by 2.8% in 2017. If realized, those would be the highest annual growth rates in nine years.

In addition, the U.S. economy has been experiencing its highest rate of job growth in 15 years. “For real estate, it’s really about jobs,” says William Maher, a director with LaSalle Investment Management, who analyzed the results of the survey for ULI.

The Consensus Forecast provides oultooks for specific construction segments:

• Institutional real estate assets are expected to provide total returns across all sectors of 11% in 2015, moderating to 10% in 2016 and 9% in 2017. By property type, returns should be strongest for industrial and office, followed by retail and apartments, in all three years.

• Vacancy rates are expected to decrease modestly for office and retail over all three forecast years. Industrial availability rates and hotel occupancy rate are forecasted to improve modestly in 2015 and 2016 and level off in 2017. Apartment vacancy rates are expected to begin rising slightly to 4.7% in 2015, 5% in 2016, and 5.3% in 2017. The 2017 forecast is just below the 20-year average vacancy rate.

• CRBE estimated that the availability rate for the industrial/warehouse sector declined to 10.3% at the end of 2014, coming in just below the 20-year average for the first time since 2007. ULI Consensus Forecast predicts availability rates will continue to decline in 2015 and 2016, with year-end vacancy rates at 9.8% and 9.6%, respectively, and remain steady in 2017 at 9.6%. Consequently, warehouse rental rate growth should continue, by 4% in 2015, 3.8% in 2016, and 3.1% in 2017, all above the 20-year average growth rate.

• The same pattern can be found in office vacancy rates, which declined for the fourth straight year, to 13.9% in 2014. That pattern is expected to continue through 2017, sparking further appreciation in office rental rates, which according the Consensus Forecast will increase by 4% in 2015 and 4.1% in 2016. Rental rate growth is expected to moderate slightly in 2017 to 3.5%.

• The Consensus foresees improvements in retail availability. And with rents increasing in 2014 for the first time in six years, the Consensus Forecast expects rental rates to sustain this growth, increasing by 2% in 2015, 3% in 2016, and 2.9% 2017.

ULI will release its next Consensus Forecast in October.

Related Stories

Retail Centers | Nov 20, 2017

28,000-sf brewery and restaurant coming to Houston’s Arts District

Method Architecture designed the three-story building.

Shopping Centers | Nov 15, 2017

900 North Michigan Shops renovation includes 190-foot-long digital art installation on the ceiling

The installation is visible from all floors and built in 10 different sections.

Retail Centers | Nov 13, 2017

American Girl Place New York opens new 37,000-sf New York Store designed by FRCH Design Worldwide

The store is located at 75 Rockefeller Plaza.

Retail Centers | Oct 25, 2017

‘Under’ will be Europe’s first underwater restaurant

The Snøhetta-designed restaurant will also function as a research center for marine life.

Retail Centers | Sep 26, 2017

DATÜM: Reinventing the department store

Department stores are going through a period of transformation in the face of a rapidly changing retail market. What’s behind the change and where is it leading us?

Mixed-Use | Sep 22, 2017

Defending against the online dragon

Some entertainment districts are going light on retail, partly because “the bulk of the leasing demand is for dining and entertainment,” say Barry Hand, a Principal with design mega-firm Gensler in Dallas.

Mixed-Use | Sep 18, 2017

Urban heartbeat: Entertainment districts are rejuvenating cities and spurring economic growth

Entertainment districts are being planned or are popping up all over the country.

Sponsored | Products and Materials | Sep 15, 2017

Creating a movement: How Mamava, Konrad Prefab and ALPOLIC partnered to change the culture of breastfeeding

Since its conception in 2006, the Mamava lactation pod has undergone several changes in design.

Mixed-Use | Sep 14, 2017

Capital One eschews the traditional bank with the Capital One Café

The new branch in downtown Santa Monica offers 8,400 sf of space designed by Gwynne Pugh Urban Studio.

Giants 400 | Sep 13, 2017

Top 75 retail construction firms

The Whiting-Turner Contracting Co., PCL Construction Enterprises, and Shawmut Design and Construction top BD+C’s ranking of the nation’s largest retail sector contractor and construction management firms, as reported in the 2017 Giants 300 Report.