In the third quarter of 2018, the U.S. office market again showed steady improvement, according to Transwestern’s national outlook for the sector. Absorption reached 22.7 million square feet, vacancy remained stable at 10.1%, and asking rents increased by 4.0%, annually.

Ryan Tharp, Research Director in Dallas, said the strong economy has contributed to the office market’s momentum, despite softer income growth in a very tight labor market.

“Real gross domestic product increased at an annualized 3.5%, according to first estimates, and personal consumption contributed 2.7% to that rate,” Tharp said. “Because inflation has remained in line with the Federal Reserve’s target of 2.0%, consumer and business confidence should keep the office market healthy well into 2019.”

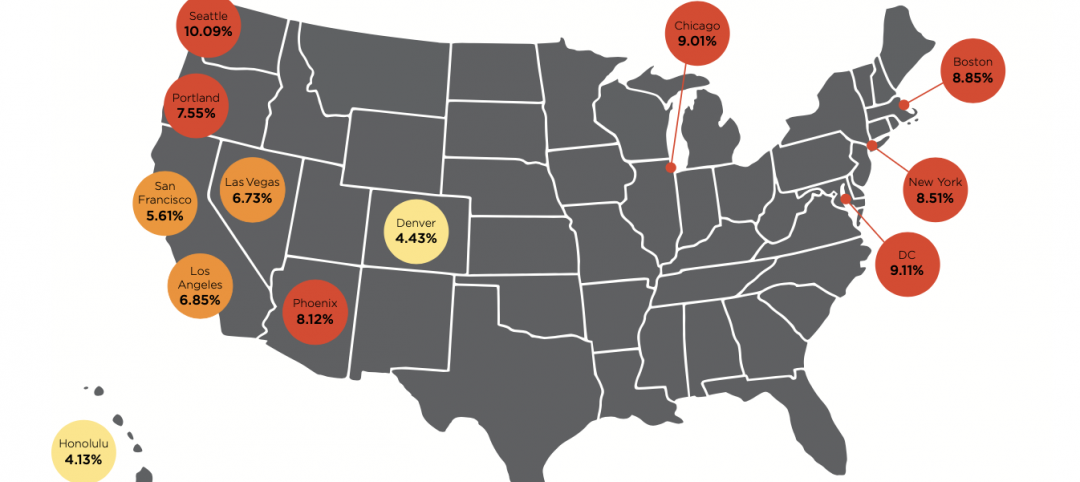

A positive sign is that year-to-date net absorption in the office market was 17.1% higher at the end of the third quarter than it was for the same period last year. Dallas-Fort Worth, San Francisco and Denver led in absorption by a significant margin for the prior 12 months, with a combined 13.3 million square feet.

Meanwhile, demand and supply are headed for equilibrium as new construction activity peaked in early 2017. In the third quarter, only 146.3 million square feet was under construction nationally.

“It’s encouraging to see that office demand is broad-based across multiple sectors, with the technology and coworking sectors driving demand as we move later in the cycle,” said Michael Soto, Research Manager in Los Angeles. “If demand continues unabated, rental rate growth should moderate.”

Year-over-year, Minneapolis, San Antonio, and Charlotte, North Carolina, have experienced the most dramatic rent growth, all coming in at 10% or greater. The strong performance of secondary markets demonstrates that the office sector is not being propped up by a few formidable markets.

Download the national office market report at: http://twurls.com/3q18-us-

Related Stories

Market Data | Jan 31, 2022

Canada's hotel construction pipeline ends 2021 with 262 projects and 35,325 rooms

At the close of 2021, projects under construction stand at 62 projects/8,100 rooms.

Market Data | Jan 27, 2022

Record high counts for franchise companies in the early planning stage at the end of Q4'21

Through year-end 2021, Marriott, Hilton, and IHG branded hotels represented 585 new hotel openings with 73,415 rooms.

Market Data | Jan 27, 2022

Dallas leads as the top market by project count in the U.S. hotel construction pipeline at year-end 2021

The market with the greatest number of projects already in the ground, at the end of the fourth quarter, is New York with 90 projects/14,513 rooms.

Market Data | Jan 26, 2022

2022 construction forecast: Healthcare, retail, industrial sectors to lead ‘healthy rebound’ for nonresidential construction

A panel of construction industry economists forecasts 5.4 percent growth for the nonresidential building sector in 2022, and a 6.1 percent bump in 2023.

Market Data | Jan 24, 2022

U.S. hotel construction pipeline stands at 4,814 projects/581,953 rooms at year-end 2021

Projects scheduled to start construction in the next 12 months stand at 1,821 projects/210,890 rooms at the end of the fourth quarter.

Market Data | Jan 19, 2022

Architecture firms end 2021 on a strong note

December’s Architectural Billings Index (ABI) score of 52.0 was an increase from 51.0 in November.

Market Data | Jan 13, 2022

Materials prices soar 20% in 2021 despite moderating in December

Most contractors in association survey list costs as top concern in 2022.

Market Data | Jan 12, 2022

Construction firms forsee growing demand for most types of projects

Seventy-four percent of firms plan to hire in 2022 despite supply-chain and labor challenges.

Market Data | Jan 7, 2022

Construction adds 22,000 jobs in December

Jobless rate falls to 5% as ongoing nonresidential recovery offsets rare dip in residential total.

Market Data | Jan 6, 2022

Inflation tempers optimism about construction in North America

Rider Levett Bucknall’s latest report cites labor shortages and supply chain snags among causes for cost increases.